In this paper, we examine the intensifying interest of investors and regulators in the environmental, social, and governance (ESG) policies of asset managers. We show an example of the factors incorporated into a common ESG metric for real assets, the Global Real Estate Sustainability Benchmark (GRESB), and describe academic research into the impact of the “green” component of ESG on property performance. That research identifies rent and value premia associated with “green certifications” and “green branding.” However, the benefits are shown to diminish over time as green properties become more common reflecting both regulation and investor appetite. Understanding these effects is becoming increasingly important as asset managers cope with the “race to zero” to achieve net zero carbon emissions by 2050.

It’s not hard to understand why commercial real estate investors are increasingly interested in ESG metrics, especially the environmental component. A well-quoted figure estimates that the “built environment” contributes 39% of global carbon emissions.1 Reflecting the importance of property to global warming, a “net zero” carbon goal as a follow-up to the 2015 Paris Accord has been adopted by 137 countries out of the 191 that signed the Paris agreement as of 2021 with more to follow.2 Controlling commercial property’s carbon footprint is crucial to achieving that goal.

While a disproportionate amount of attention toward the environmental aspect is accruing—perhaps reflecting extreme climate events—social and governance concerns are also noteworthy. In the social component, property is also prominent, particularly regarding availability of affordable housing. In the US, 46% of households are experiencing rent stress defined as devoting 30% or more of household income to housing. At the same time, homeownership is out of reach for many with the median home price more than four times median household income, the highest ratio since 2006.3 The governance component is likewise important to property investors, especially related to the appetite for transparency, reporting and benchmarking to satisfy the demands of their own constituents.

Investor interest in ESG is growing

As indicated by the expanse of GRESB participants, interest in ESG among investors has been growing.

Private Equity Real Estate’s (PERE’s) 2019 ESG Investor Survey of 60 institutional investors in private equity real estate funds reported that 35% were currently requiring ESG initiatives from their advisors, 13% were planning such requirements for the following 3-5 years, and 27% were considering such requirements. Moreover, more than 80% of respondents reported that ESG policies were established to meet investor demands.4

Along with growing investor interest in ESG, regulators are also sharpening their focus. In March 2021, new European Union (EU) rules affecting ESG disclosures of asset managers that sell products in the EU took effect. The new rules are aimed at making disclosures regarding the ESG characteristics of funds and investments more robust and consistent. Under the new rules, fund managers are required to describe how ESG considerations are integrated into their investment processes or not integrated, whether or not a specific fund is marketed as ESG focused. At the end of the year, a “taxonomy regulation” will apply a classification tool that offers standardized definitions of activities that can be called “green.”5

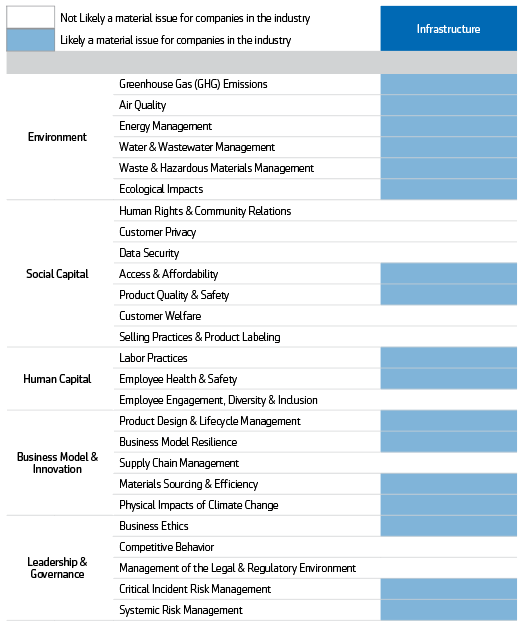

What are ESG considerations for property?

The most comprehensive metrics for assessing and benchmarking ESG results have been developed by GRESB. GRESB was founded in 2009 with the goal of providing standardized and validated data on the performance of real assets including real estate and infrastructure. In 2021, more than 1,520 REITs and other real estate owners completed GRESB assessments for 117,000 properties in 64 countries totaling $5.7 trillion in value. Elements of GRESB scores are shown in Exhibit 1.

Exhibit 1: GRESB score elements

Investment property performance benefits

The intensifying interest of investors in ESG and the broadening requirements of regulators are fostering interest in the impact of ESG policies on investment performance. A growing body of research is focusing on this concern and uncovering positive impact despite fears that ESG efforts might impair performance. Several notable studies are highlighted in the paragraphs that follow.

With regard to GRESB ratings, a 2015 study calculated that global REITs enjoyed significantly better return on assets (ROA)and return on equity (ROE) associated with better GRESB scores. For example, a 1% higher GRESB score was associated with a 1.26% higher ROA while a 1% higher GRESB score was associated with a 3.29% higher ROE. In addition, a 6.93% higher Sharpe ratio for REIT stock return was also associated with a 1% higher GRESB score.6 This study is unique in that it uses GRESB scores to focus on entity level performance rather than property level performance. It is important to note however, that the study covers a short time period, 2010-2014, reflecting the relatively recent 2009 inception of GRESB reporting. Moreover, the results do not prove causation but only identify association. Are better performing REITs perhaps more likely to be GRESB participants? Are they perhaps more financially able to commit resources for collecting required GRESB data? Are they perhaps more attune to the interest of their stockholders in ESG? Or might better performing REITs be actually reaping benefits associated with their ESG policies? Further research may answer these questions.

The bulk of research on ESG impact on commercial real estate performance has focused on “green certifications”. In the US, these are primarily Energy Star and LEED; both were developed in the 1990’s to reward properties with energy saving sustainability characteristics. According to CBRE, 42.2% of the total office space in the top 30 US office markets held one of the green certifications in 2019. At the same time, more than 250,000 apartments totaling 3.3% of investment grade units within the top 30 markets were also green certified in 2019.7

Recent research examined 71 peer-reviewed academic papers dealing with green certification. Most were published between 2012 and 2016 and the vast majority focused on US office properties with LEED and/or Energy Star certifications. The research shows generally positive results for fundamental property performance associated with green certifications. Specifically, rent premiums were on average 6.3% higher, occupancy was 6.0% higher, and sales prices were 14.8% higher. Yields were on average were 0.46% tighter. The studies controlled for property age, size, quality, locational attributes and type of rent contract using various protocols. It is crucial to account for these property characteristics to avoid the possibility that green certified buildings might be stronger performers because they are newer or better.

Several of the surveyed studies found that increasing supply of certified buildings in specific markets was associated with a decline in rent premiums over time. This finding is extremely important because it suggests that the value of green certifications may reflect their novelty and/or relative scarcity. Expanding on this point, the authors further note that: “As sustainability becomes mainstream, it is not just a question of how much more valuable sustainable buildings are compared to regular buildings. Regular buildings are those that suffer from faster obsolescence and tightening regulations, which further increases the polarization between sustainable and non-sustainable assets.”8

Green certification has also been beneficial for apartment properties separately. As part of their research, Shaun Bond and Avis Devine collected data on all LEED certified apartment properties with at least ten units totaling 97 properties with 26,744 units. They matched each LEED property with nearby comparable properties based on size, quality, amenities, and locational characteristics. As is typical for apartments, the majority of units were leased on net terms so that energy savings accrued largely to tenants. This contrasts with the gross leases typical for office properties under which landlords enjoy energy savings benefits. In their paper, Certification Matters: Is Green Talk Cheap Talk, Bond and Devine find that LEED properties have a rent premium of 9.1%.9

Source of premia: Reputation and energy savings

Research has also delved into the sources of better performance from certified properties. For example, in their paper, Green Certification and Building Performance, Avis Devine and Nils Kok identify higher levels of tenant satisfaction, increased probability of lease renewal, and lower rent concessions for certified buildings. These findings suggest that certified buildings are associated with a “green brand” that has value.10 Such branding value was also found in the Bond and Devine paper which found a 4.7% rent premium for properties that market themselves as “green” but without certification versus the 9.1% premium they found for LEED properties.9 While these studies do indeed show the value of green branding, it may well be related to scarcity. Once “green” becomes common through the combination of regulation and investor appetite, its value may diminish as described in the UK paper mentioned above.8

Beyond brand value, there is also evidence that rent and property value associated with certifications vary by the amount of energy savings again controlling for type of rent contract, etc. A study of 293 Energy Star office properties assessed in 2009 shows, “A $1 saving in energy costs of a building is, on average, associated with a 3.5% higher rent, and…4.9% premium in market valuation.”11

Another source of green benefits is associated with reduced cost of debt. In a study of US and UK REITs, researchers estimated a 10-basis point lower interest expense ratio for US REITs with green assets significantly above the average portfolio proportion.12

Getting to net zero carbon

The net zero carbon goal initiative, titled the “Race to Zero,” is indicative of the disproportionate focus on environmental issues. It is led by the Climate Ambition Alliance (CAA) and is an offshoot of the United Nations Framework Convention on Climate Change (UNFCC) which manages the Paris Agreement of 2015. The Race to Zero program, is recruiting governments at all levels, companies, organizations, and investors, as well as countries, to participate in reducing carbon emissions to achieve net zero by 2050. The target is intended to limit the risk of average global temperature rise above 1.5 degrees Celsius. Referring to the UNFCC analysis released in September, UN Secretary General Antonio Guterres said it shows “the world is on a catastrophic pathway” with a 2.7 Celsius rise estimated by the end of the century in the absence of serious action.13

For commercial properties, getting to net zero carbon requires innovative approaches to construction that address the carbon embodied in steel and concrete as well as energy saving operation through eliminating use of fossil fuels. Proven technology for doing so is available as demonstrated in the almost 700 properties have been verified as certified or emerging net zero buildings as of last year.14

But retrofitting of existing structures will also be required due to the slow pace of replacement of existing assets by new construction. Retrofitting can be financially advantageous when the investment produces step-ups in rent and property value. Retrofitting to “green” standards might also produce branding value. Availability of carbon offset credits can add further benefit. But many properties will be deemed to have poor prospects for retrofitting and to be unworthy of the cost of carbon offsets. This cohort will likely include properties that are locationally vulnerable to climate change and extreme weather events beyond what is insurable for reasonable cost. This cohort will lose market value, suffer accelerated obsolescence, and probably revert to non-institutional ownership.

Conclusion

Commercial real estate asset managers are witnessing intensifying interest in ESG policies from investors and regulators. Addressing this interest involves adopting standards such as GRESB, LEED and Energy Star, incorporating certified properties into commercial mortgage debt and property portfolios, and making ESG retrofits in existing property portfolios. Investment activities will also involve accessing the evolving price and availability of carbon credit offsets. When combined with tightening regulation, these efforts will influence the potential for a carbon neutral future as expressed in the “Race to Zero” initiative.

In this paper, we describe the investment performance benefits associated with green certifications as identified by researchers; we note that the benefits are dissipating over time as green properties become more and more common which might appear to be shrinking the incentive for retrofitting. While this diminution might make the “Race to Zero” more difficult, it could, on the other hand, be replaced by a new branding opportunity around efforts toward the net zero goal.

References

1World Green Building Council, Bringing Embodied Carbon Upfront, September 23, 2019.

2UNFCCC, Climate Ambition Alliance, September, 2021.

3Harvard Joint Center for Housing, State of the Nation’s Housing, 2021.

4PERE, 2019 ESG Investor Survey, July/August 2019.

5Proskauer, European ESG Disclosure Requirements for Asset Managers, September 23, 2020.

6F. Fuerst, The Financial Rewards of Sustainability, University of Cambridge, June 16, 2015.

7CBRE, Green Building Adoption Indexes, 2019.

8N. Leskien, et. al., “A Review of the Impact of Green Building Certification on the Cash Flows and Values of Commercial Properties”, Sustainability Journal, March 2020.

9S. Bond and A. Devine, “Certification Matters: Is Green Talk Cheap Talk”, The Journal of Real Estate Finance and Economics, V52, 2016.

10A. Devine and N.Kok, “Green Certification and Building Performance: Implications for Tangibles and Intangibles”, Journal of Portfolio Management, 2015.

11P. Eichholtz, et. al., “The Economics of Green Building”, The Review of Economics and Statistics, March, 2013.

12A. Devine, E Steiner and E. Yonder, “Decomposing the Value Effects of Sustainable Real Estate Investment: International Evidence”, European Real Estate Society, 2017.

13New York Times, “United Nations Warns of ‘Catastrophic Pathway’ with Current Climate Pledges”, September 17, 2021.

14New Building Institute, 2020 Getting to Zero Buildings List, September 2020.