COP26 was all about the international community helping design and deliver a more sustainable future for both people and the planet. But while the steps that developed countries are taking have come under a great deal of scrutiny, there has arguably been less attention on the advancement – and financing – of sustainability in emerging markets.

Of course, all eyes are on China, the world’s largest greenhouse gas emitter, responsible for around 30% of global CO₂ emissions. In September 2020 China’s President Xi Jinping pledged to become carbon neutral by 2060, meaning that the country’s carbon emissions would be balanced out by funding an equivalent amount of carbon reduction elsewhere. China also recently announced plans to cut its reliance on fossil fuels to below 20% by 2060, an ambitious statement given that last year coal made up nearly 60% of the country’s energy use1. In line with these targets, China is now the leading renewable energy technology producer and exporter, demonstrating its strong commitment towards sustainability2.

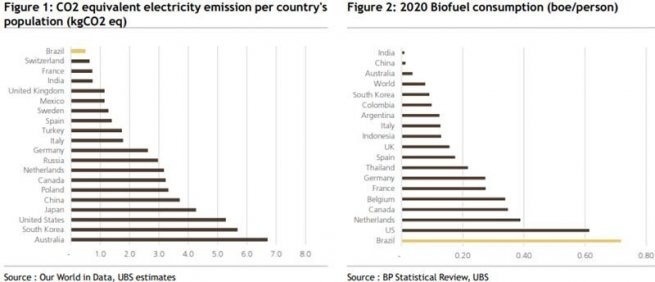

Outside of China, other emerging markets are making big strides in terms of environmental policies. For example, Brazil has been adding ethanol to its fuel to reduce reliance on gasoline for almost 50 years, and in 2020 the national average consumption of biofuel was 0.72 barrels of oil equivalent (boe) per person, considerably higher than the global average of 0.08 boe per person3. In addition, some 84% of Brazil’s electricity comes from renewable sources, one of the highest proportions globally4.

Meanwhile, Costa Rica has undergone a huge reforestation programme, increasing forest coverage to 60% of the country from 40% only 30 years ago5. With an abundance of solar and wind power to harness, Chile also has extensive capacity for renewable energy. In 2020 the country set a goal to become one of the world’s top producers and exporters of green hydrogen (hydrogen produced from renewable energy), a key initiative towards the goal of driving down global consumption of fossil fuels.

Other regions are less advanced in their sustainability policies, with Africa an example of where there is still much work to be done. However, this also means that there are huge opportunities for a positive environmental impact. The African Green Stimulus Programme, launched in 2021, is designed to support the continent’s recovery response to the devastating socio-economic and environmental impacts of the COVID-19 pandemic in a more green and sustainable manner. At the same time, given that a large percentage of Africa’s labour force is employed in agriculture, there is a significant need for support to improve agricultural productivity, which could in turn lead to greater food security. In addition, millions of people in the continent are still without clean drinking water, another key area that must be addressed.

Growth of green bonds

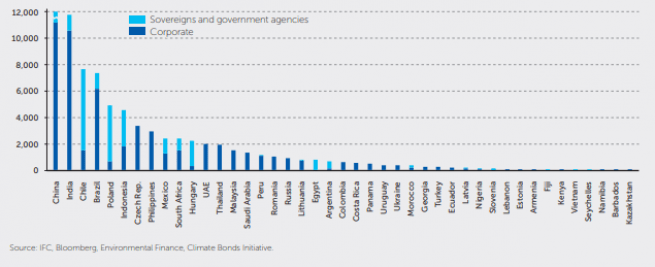

The development of the green bond market is a clear demonstration of the commitment emerging markets have towards climate change, as the debt is issued with the intention of using the proceeds to fund sustainable projects. In 2020, some $40bn of green bonds were issued across emerging markets – a 20% increase from the previous year. Since 2012, 43 emerging market countries have issued green bonds, amounting to $226bn of total issuance. Although the green bond market still only constitutes 5.5% of total emerging market credit, it is expanding rapidly, with $100bn of annual issuance expected by 20236. China continues to be the biggest issuer of green bonds in emerging markets, but India, Chile and Brazil have also been big drivers of this growing market in recent years.

Figure 3: Cumulative Emerging Market Green Bond Issuance, 2012-2020 (in US$ million)

Hurdles remain

However, there are still hurdles for emerging market countries to overcome in implementing sustainable policies. For instance, many developing countries currently lack the technology to adopt renewable energy and/or the wealth to develop it, while poorer nations have more basic needs to address. In addition, given the heterogeneity across emerging markets it is difficult to implement a one-size-fits-all model. For example, the terrain of Brazil makes the implementation of electric trains difficult, while the lack of infrastructure in Colombia means the adoption of sustainable technology is challenging.

On the one hand, emerging market countries are some of the biggest carbon emitters, reflecting their rapid recent economic growth, often combined with cheaper carbon-intensive energy sources. But on the other, carbon emissions per capita are significantly higher in developed markets, and the vast majority of the carbon budget has been used up historically by developed nations, in particular the European Union (EU) and the US7.

We believe the implementation of decarbonisation programmes should not come at the cost of future economic growth of emerging market countries and developed nations have a responsibility to help finance sustainability in emerging markets. For example, they can provide funding assistance and technology to allow quicker implementation of environmental policies, recognising that it will require a collaborative effort to fight climate change. The agreement at COP26 for the US, the EU and other developed countries to help fund South Africa’s transition away from coal is a positive step and one that could serve as a model for other countries – and other projects.

Our convictions

Environmental, social and governance (ESG) factors are a key consideration when directing capital towards emerging markets. Our emerging market debt strategies adhere to AXA IM sectoral exclusion policies, meaning they do not invest for example in controversial weapons, soft commodities or palm oil. We also apply the AXA IM ESG Standards policy, which also excludes certain areas like tobacco, as well as our ESG scoring methodology. We aim for our emerging markets debt strategies to hold an ESG score greater than that of their benchmark or universe, encouraging a tilt towards investments with a high-ESG quality.

Over the past 20 years, many emerging market countries have largely been thought of as commodity exporters, with economies built on their natural reservoirs of oil, gas and metals. As such, the energy sector has typically represented a significant allocation in emerging market debt strategies. However, we have been reducing our exposure to these assets in favour of more consumer-driven sectors which we believe offer greater sustainability. We have also been focusing on renewable energy opportunities across Latin America and Asia.

In addition, we have been seeking to reduce the carbon footprint of our emerging market debt strategies. We have reduced exposure to sectors with high carbon emissions such as steel and protein producers and utility companies. Across AXA IM, we have also strengthened our policy for the oil and gas sector, with new exclusions to mitigate the adverse impacts of the industry on the environment. Within emerging markets fixed income strategies, we have reduced exposure to oil producers, particularly those that are state-owned enterprises, which in addition to being carbon-intensive are also potentially less open to engagement.

We believe that sustainable development issues are a major concern for investors in emerging market debt. By combining ESG factors with traditional financial criteria we aim to not only build more stable investment strategies with potentially superior long-term returns., but also help emerging market countries play their part in financing a more sustainable future for the planet.