Jeremy Gleeson, Portfolio Manager and head of AXA IM’s Technology investment team explains why investors should not let short-term volatility nerves curtail their potential gains from long-term, fundamentally sound megatrend growth themes.

It’s been a complex year for equity markets, particularly within strategies focused on the traditionally ‘growthier’ technology companies. The resolve and nerve of equity investors has been subject to one barrage after another of critical hits over the period – rate rises, geopolitical tensions, the threat of rampant inflation, supply chain seizures and shortages and, of course, that little matter of a multi-year global pandemic. It’s somewhat understandable that drawing such a bad hand all at once, combined with some high-profile individual stock disappointments, has led investors to something of a flight to safety and a market rotation in favour of value-orientated stocks. It’s also not hard to envisage why investors have taken one eye off the long-term fundamentals of growth companies, when constant market upheaval, changing government policies and external events have encouraged a shift to reactionary short-termism. However, whilst volatility could well continue for some time, investors should also note that is opening up some interesting opportunities for long-term investors.

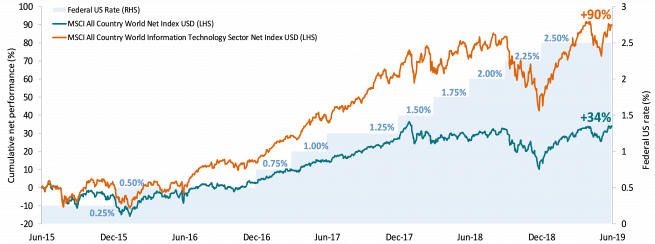

Consider the performance of the MSCI ACWI index relative to the technology sector. There is clear historical evidence that equities within the technology sector historically outperform the broader equity index. This is not a COVID-19 hangover; as per the chart above, this effect has been developing, even during the last upward interest rate cycle. The pandemic has, however, accelerated a trend that was already in place and is now unlikely to recede in a meaningful way outside of short-term market disruption. The question is whether investors are willing to consider the potential long-term cost of moving to assets perceived as less risky and the associated costs of short-term trading movements, or if they can hold their nerve when the going gets relatively tough. This is a perpetual challenge for equity investors and one that never gets easier to navigate.

Despite all the doom and gloom, there’s already considerable evidence to suggest that our investment theses remain strong. Of those companies that we invest in within the Digital Economy strategy that have reported first quarter results for 2022, 72% have delivered better than expected revenues and provided better than expected earnings, suggesting that these businesses continue to grow faster than what was expected of them.

Do FAANGS have teeth?

It’s easy to measure the trials and tribulations of the technology sector through the prism of the usual Facebook, Amazon, Apple, Netflix and Alphabet (FAANG) suspects, and monitor these as a bellwether for the sector in general. While these are often important positions within the Digital Economy strategy to varying extents, this approach risks highlighting stock-specific idiosyncrasies and ignoring the diverse nature and rich source of growth opportunities found across the technology sector and market cap spectrum. As we discuss below, behind these A-list names exists a worthy rollcall of less headline-grabbing manufacture, infrastructure, software producers and more. These industries are critical for the digital operation of an abundant and growing range of sectors. Let’s consider one small, anecdotal example to understand just how fundamental the shift and acceleration in synergistic, cross-industry technological capabilities has become.

I want it all, and I want it now

Picture the scene: a student in the 1990s needs an obscure, yet vital book to complete their course. They go to their local library, fill out a paper application form, and request the book be located. A manual paper card is filled out by the librarian and filed for searching. The student pays a fee in cash and waits several weeks, until the book is finally sourced by the library’s limited national network. Our student then returns to the physical premise once more, to finally obtain the book and squeeze the assignment in just in time.

In 2022, thanks to sophisticated e-commerce capabilities, our student can be online within the touch of a mobile screen and locate the same book from any number of online outlets, large and small. They can also search private sellers and auction sites around the globe within seconds. The book is found within minutes and purchased with one click, facilitated by payment providers which are continually investing in improvements and innovations and becoming accessible to more and more global customers. Financial details are encrypted and protected from theft by capabilities provided to the e-commerce site and the payment provider by one or more cybersecurity firms. The book is packaged and sent out by the vendor’s automated procurement and dispatch facility and is received by our student the next day without ever leaving their house. It’s inconceivable that the trajectory of increasingly demanding consumer expectations is going to go in any other direction than forwards and faster; consumers have become accustomed to everyday conveniences and are not going to accept anything less. This is where the sub-themes of the Digital Economy strategy come into play.

Discovery, decisions, defence and data

In our example above, we considered how the growth of the digital economy is driven by several key, overlapping ingredients. We’ve defined these as:

- Discovery – how consumers access products and how businesses attract new customers

- Decisions – e-commerce companies, web portals and mobile apps which provide consumers with convenient and reliable product choices.

- Delivery – companies which help facilitate and secure payments and logistics to keep pace with consumers’ increasing expectations of rapid dispatch and same-day delivery. This is a diverse area that spans companies in the payments space, cyber security, logistics and real estate.

- Data & Enablers – IT Services companies that provide technologies or services that help their customers adopt a digital ethos

The need for companies around the world to modernise and digitalise their businesses continues as we have been seeing good results from companies involved in many different aspects of this from consulting businesses such as Accenture and Endava to providers of software services such as ServiceNow and Zendesk.

Supply chain issues affecting the technology sector are far from resolved and point to a future where the pain suffered by vendors of physical technology equipment over the past year will give way to the delayed gratification of much more favourable future quarters, where large backlogs of orders will be filled. As anyone who’s tried to buy a MacBook Pro M1 Max over the past year will attest, consumers (and particularly those at the specialised and higher spec end of the market) are prepared to wait and not compromise with alternative, more readily available products. This is in part due to brand loyalty to Apple, and to the ubiquity of its suite of products in certain creative and design industries with a high saturation of Mac-specific software. Increasingly demanding video capabilities in 4K and 8K definition are only going to require more powerful chips and capabilities to fulfil the growing and insatiable need for high-quality online content generation.

Similarly, the lifting of travel restrictions related to COVID-19 are helping open aspects of the economy that have been largely closed for the best part of two years. We think this will help payment companies who will benefit from the increase in cross border transactions because of more overseas travel. One such beneficiary of this trend is FIS, who will benefit due to a resurgence in card-based transactions at hotels, restaurants, and other venues due to lockdown restrictions easing.

And now, a message from our sponsors

Similarly, where there’s an audience, there’s an advertising opportunity – and that means revenue. Within the strategy’s interactive media and services allocation, the past year has already been relatively kind to companies such as Alphabet (the holding company behind brands such as Google and YouTube), and Meta Platforms, the social media firm whose assets also include Facebook, Instagram and WhatsApp. These companies have already benefitted from increased spending on online advertising and are well placed to continue to mine returns from this escalating trend. While consumers faced with fears over the rising cost of living and inflation may seek to cut household bills by reducing ad-free premium streaming services, this could be offset by the increased revenue from advertisement saturation and increased click-through rates. It also links into to the revival of the travel company which traditionally uses a high level of advertising. Again, this highlights how the Digital Economy strategy achieves diversification via very different sub-themes, but also benefits from a synergistic overlap effect which can benefit the whole portfolio.

The economy is evolving, and a key driver of this is disruptive and innovative technology

The compelling case for the Digital Economy strategy is part of AXA IM’s view that clear megatrends exist across certain economic, corporate, social or technological themes. These themes all have two fundamental drivers in common – demographic shifts, and, most pertinent here, technological changes and accelerating capabilities.

It’s important to take a step back and recognise that despite all the external market stressors playing on the minds of investors, company fundamentals have been reasonably robust and results from companies within the Digital Economy sector have for the most part been good. One prominent theme in the strategy is cybersecurity, which continues to benefit from a strong need for companies and governments to help protect themselves and their employees and customers from multiple threats. Another theme is the need for companies around the world to modernise and digitalise their businesses continues, as we have been seeing good results from companies involved in many different aspects of this from consulting businesses such as Endava and providers of software services such as ServiceNow and Salesforce. The opportunity for payment companies to thrive post-lockdown mentioned earlier is multi-faceted, and benefits from a rise in cross-border payments as well as increased domestic transactions.

Unfortunately, during periods of market volatility, any positive trends can often be overlooked, so we continue to focus on what we always do in terms of identifying attractive long-term investment opportunities. The message for long-term investors is clear – stay connected; hold fast during short-term market volatility, and don’t get left behind.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.