Boston – The sell-off in emerging markets debt (EMD) continued through the second quarter along with the majority of global capital markets. Stocks and bonds generally moved in tandem, as markets continued to price in the potential for the end of the “easy money” era of the past decade.

Inflation remained a key issue in just about every country, and central banks have largely been forced to react with increasingly hawkish policy stances. Higher food and energy prices, a second-order effect of the devastating war in Ukraine, continued to divert more consumption toward necessities and away from global discretionary spending and investment.

While we observed some easing of China’s zero-COVID policy, it continues to create challenges for global supply chains and remains a drag on the world’s second-largest economy. This combination has led investors to more seriously consider the likelihood of recession in the near term — a slowdown in which EMD markets will likely not be spared.

Outflows year to date are at all-time highs for both local- and hard-currency funds, which is reflective of the problems in the market and macro environment.

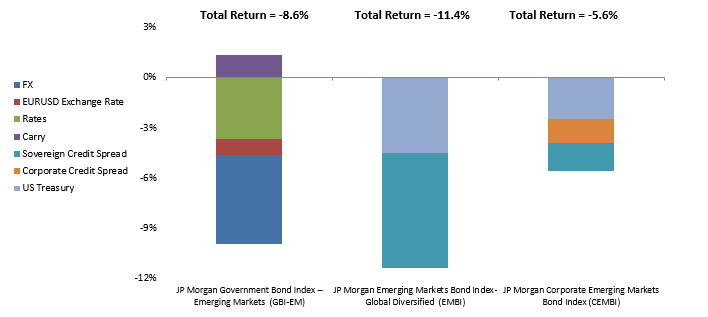

- Corporate EM debt, while losing 5.6%, was the best-performing EMD sector. Its relative outperformance reflected its country makeup — being more heavily tilted toward Latin America — as well as its higher-quality profile and the underlying relative strength of the issuers.

- EM local-currency debt lost 8.6%, weighed on by the broad rally in the U.S. dollar, while local interest rates generally also moved higher, in keeping with the global trend.

- Dollar-denominated, hard-currency debt was the worst-performing segment, with a loss of 11.4%. Spreads broadly continued to widen, and more countries saw their bond prices move toward distressed levels. Rising U.S. Treasury yields also hurt the sector, given the relatively long U.S. duration profile of most issues.

War and rising rates continue their double whammy for EMD

Looking ahead

Through the remainder of 2022, we are optimistic on EMD, as valuations appear to be well compensating investors for the risk.

- The macroeconomic environment is challenging for all areas of capital markets, but it appears EM investors have already priced this in better than most.

- Inflationary pressures, and corresponding central bank reactions, remain the most important factor for the asset class. Commodity prices are likely to be the largest driver here and something we are watching closely.

- No end appears in sight for the devastation in Ukraine, or the impact on food and energy prices.

- China appears to be easing policy on the margin and moving slightly off its strict, zero-COVID policy. Reformers may make gains during the Party Congress in a few months, but President Xi’s power remains unquestioned.

- While COVID continues to wreak havoc on lives and livelihoods, many countries have learned to live with the virus, and it appears to no longer be the most important factor in most countries.

Bottom line: We expect markets to continue emphasizing differences among countries and credits. That creates investment opportunities for those with research capabilities and due diligence that are up to the task. That is why we focus on country-level macroeconomic and political research, and stand-alone analysis of specific risk factors such as currency, credit spreads and interest rates — an approach we have followed for more than two decades.

Investing entails risks and there can be no assurance that any strategy will achieve profits or avoid incurring losses. It is not possible to directly invest in an index. Past performance does not predict future results.

The value of investments may increase or decrease in response to economic and financial events (whether real, expected or perceived) in the U.S. and global markets. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical, currency exchange rates or other conditions. Investments in debt instruments may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline.