– Since the introduction of the US IRA the European Union has been concerned about an exodus of both manufacturing and product development investment towards the US and realised it must act to support its green industries

– The common goal of both plans is to increase the domestic manufacturing capacities of clean technologies and reduce the over reliance on China

– What are the investment implications as the two go head-to-head, and what will China do in response?

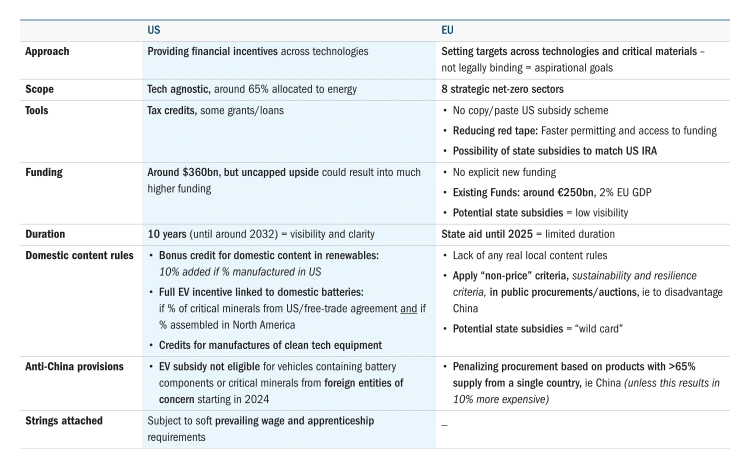

The US Inflation Reduction Act (IRA) passed in summer 2022 is the most ambitious clean energy plan introduced in the US. The IRA provides long-term visibility, highly executable features, and massive subsidies across all clean technologies1.

But as much as the IRA is a climate bill it is an industrial policy. It provides fiscal support to the whole clean energy value chain – from materials to manufacturing and deployment – with the aim to develop domestic supply chains and reduce the reliance on China. As such, domestic content rules linked to tax credits are a key feature of the Act.

The clear and actionable framework of IRA credits substantially shifted the playing field towards the US in terms of attracting investments in clean energy and redirecting capital away from the European Union (EU).

Since the introduction of the IRA, the EU raised its concerns about two basic risks: an exodus of both manufacturing investment and of project development investment. The risks became quite tangible as numerous EU companies started to announce plans to expand into the US at the expense of Europe – such as Volkswagen’s decision to prioritise a battery plant in the US instead of eastern Europe2.

Thus, in Q1 of this year the EU announced its response to the IRA, the Green Deal Industrial Plan3. The Plan is not revolutionary but evolutionary, and represents an acceleration of policies in order to adapt to a post-IRA and more competitive international clean tech environment.

The Plan consist of two Acts: the Net Zero Industry Act and the Critical Materials Act, which basically set the target to scale up domestic manufacturing capacities of eight strategic net zero technologies so at least 40% of their demand is supplied from within the EU by 2030 and 40% of the minerals needed are processed in the bloc.

The targets are significant but not binding and are proposed to be achieved by reducing red tape: facilitating existing financing and shortening permitting process. Although the Plan does not include a mass EU-wide subsidy scheme that mirrors the IRA, it does propose the temporary relaxation of state aid rules for countries to provide tax support to potentially “match” IRA benefits.

This provides a strong signal of the EU’s determination to compete for green industries, even if it remains unclear how countries will deliver it (Figure 1). We therefore believe that the simplicity and clarity of the IRA will likely remain the key factor in investment decision-making in a US versus EU scenario and result in a smaller scale of support in the EU.

Figure 1: two competing approaches

What is the key problem both the US IRA and EU Green Deal Industrial Plan are trying to solve?

Despite the different approach and tools of both policies, there is one common goal behind them: to increase the domestic manufacturing capacities of clean technologies and reduce the over reliance of China.

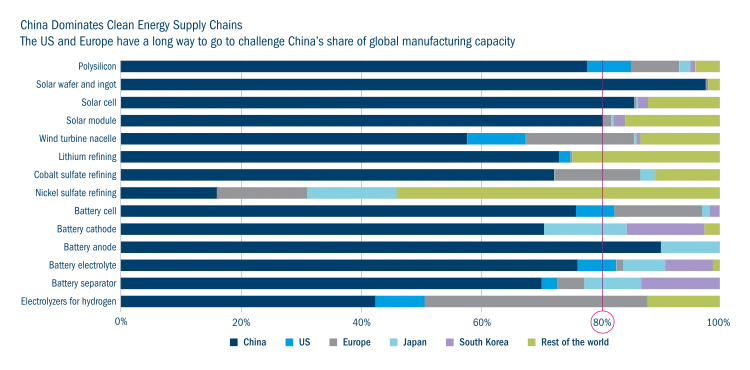

The energy transition represents a supply-chain challenge. Very little manufacturing is located in either US or Europe with China dominating the manufacturing of key sectors of the energy transition: solar, wind and battery with more than 80% of global capacity (Figure 2). As such the US and EU’s aim to support domestic supply chains by establishing local manufacturing will be difficult and expensive.

Figure 1: China dominance

Direct implications

The combination of the IRA and the Green Deal should bring tailwinds for companies in the clean energy value chain, particularly to those with global exposure to both regions. The uncapped nature of the IRA tax credits means the amount of capital that could be mobilised could significantly exceed the estimated $370 billion initially set out in the plan4, with both Goldman Sachs and Credit Suisse estimating around $1.5 trillion in investments over the coming decade5.

Meanwhile, despite the fact the EU Green Deal does not contemplate new funding, the EU says it has around €250 billion of REPowerEU funding to spend6 – but this is small in comparison to the estimated $1 trillion annual investment needed in the EU7. However, faster access to funding coupled with looser rules for country state aid could be instrumental to unlocking private capital.

Success in the EU also relies on individual member states implementing the Green Deal Industrial Plan, which makes it hard to assess the impact. A larger and faster policy response could boost investor interest and provide more support to EU companies. Within the EU those companies with German exposure could potentially benefit most, given Germany’s fiscal flexibility to provide subsidies and drive to compete for capital allocation.

Among the sectors that should benefit from both US and EU IRA/Green Deal dynamics are:

- Renewables generators Clear winners are those companies for which wind and solar is already competitive, even without subsidies, and are present in regions that will see mobilised capital and strong growth in renewables such as Iberia, Germany and the US. Hence, the US and EU IRA/Green Deal represent incremental tailwinds.

- Integrated players Industrial gas companies that will benefit from the potential wider adoption of hydrogen (blue and green).

- Hydrogen pure players/electrolyser manufacturers Especially firms with a strong global presence already generating large part of their revenues from the US.

- Renewables manufacturers These will benefit particularly given the focus and support on domestic supply chains. Thus wind turbine manufacturers, solar panel producers and battery manufacturers will see strong tailwinds.

- Mining/metals recycling Miners and processors with exposure to critical materials that are expanding in the EU region should benefit from simplified permitting and state funding.

- Companies exposed to the renewables value chain An acceleration of renewables will drive higher demand from those companies in the value chain that produce a differentiated product relevant for their generation. The materiality and timing of the impact on earnings will vary by company, but those in electrical equipment, mining equipment and energy efficiency will be positively impacted.

Broader implications and the future

The dynamics of the IRA and Green Deal clearly push for onshoring and more diversified supply chains. A more fragmented global marketplace – including within the EU – will result in new considerations for both investors and corporates.

The focus to avoid excess reliance on China while remaining competitive will be challenging. The reshoring of critical inputs has the potential to limit some industries’ capability to upscale, and the challenges in sourcing raw materials and scaling up production facilities may have unintended consequences. For example, in order to build diversified and localised supply chains sourcing needs will become a strategic priority for companies: long-term partnerships, targeted acquisitions and vertical integration can be critical levers for securing raw materials. We could increasingly see initiatives by original equipment manufacturers (OEMs) to secure access to raw materials, and renewables developers partnering with suppliers to build additional manufacturing capacity or investing directly in vertical integration. This could include the insourcing of critical components, the expansion of manufacturing facilities or the creation of new facilities.

Intensifying competition in the upstream battery or renewables supply chains could be detrimental for companies in these industries, and there is also the potential for higher price volatility of key clean energy components and raw materials. In turn there is a risk of a more inflationary energy transition: producing many of the components and sourcing many of the materials critical for clean technologies locally could be costly and inefficient, and hence more expensive than currently importing them from China.

In terms of solar specifically there is a risk of oversupply. It is not just the US and EU looking to boost domestic production; India is also providing subsidies8 and China itself has plans to expand manufacturing through the entire supply chain much more quickly than other countries. The IEA expects this in particular to cause a major glut by 2027, with solar supply significantly exceeding expected global demand. The result would be plant utilisation levels of as low as 25%-30% in China for all manufacturing segments – about half of today’s level9. This glut could also create fierce price competition and cause investors to cancel many announced manufacturing expansion projects both within and outside of China.

Other unintended consequences could see: local content requirements and limited availability of materials promoting an acceleration in circular-economy/recycling to reduce resource consumption – for example a higher emphasis on battery and minerals recycling; and the growth of new technologies/a spur in innovation – for example, the EU does not produce any lithium, so battery manufacturers will be incentivised to keep innovating sodium-ion batteries that are made without lithium.

What will all this mean geopolitically? The elephant in the room is China’s response. Given both the US IRA and the EU’s Green Deal Industrial Plan could disadvantage Chinese players in the clean tech sector, in favour of the US and the EU themselves, it is not inconceivable for China to retaliate. So there is a risk of rising global trade tensions. However, the flip side to this is a rise in “friend-shoring”, whereby the US expands its trade agreements elsewhere, offering tailwinds to firms in Japan, Korea, Chile, Australia – and perhaps the EU – among others. We will watch the developments with great interest.

1 Read more: Columbia Threadneedle Investments, US Inflation Reduction Act: a strong force to accelerate energy transition technologies, 16 November 2022

2 FT.com, VW puts European battery plant on hold as it seeks €10bn from US, 8 March 2023

3 All Green Deal figures from https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal/green-deal-industrial-plan_en

4 https://www.cbo.gov/publication/58366

5 Credit Suisse, US Inflation Reduction Act, September 2022 and Goldman Sachs, Inflation Reduction Act, January 2023

6 https://ec.europa.eu/commission/presscorner/detail/en/ip_23_510

7 IEA, World Energy Investment 2022

8 https://www.iisd.org/publications/mapping-india-energy-policy-2022

9 https://www.iea.org/reports/renewables-2022

Risk Disclaimer

Views and opinions have been arrived at by Columbia Threadneedle Investments and should not be considered to be a recommendation or solicitation to buy or sell any companies that may be mentioned.

The information, opinions, estimates or forecasts contained in this document were obtained from sources reasonably believed to be reliable and are subject to change at any time.

Engagement efforts outlined in this Viewpoint reflect the assets of a group of legal entities whose parent company is Columbia Threadneedle Investments UK International Limited and that formerly traded as BMO Global Asset Management EMEA. These entities are now part of Columbia Threadneedle Investments which is the asset management business of Ameriprise Financial, Inc. Engagement and voting services are also executed on behalf of reo® clients.