Boston – Last year’s hammering of the traditional stock/bond portfolio was less severe for accounts with allocations to senior loans, thanks to the outperformance of loans that was nothing short of dramatic. Immunity from higher interest rates — in fact, participation in them — was key, as was the buoying effect from the robust buying of institutional investors.

That performance follows from the hybrid structure of loans, an asset class with characteristics of bonds (a face amount, a maturity, a coupon) and equities (a price that can bump with headlines). At the same time, loans are unique: Unlike bonds, which sport “fixed” coupons, loan interest payments actually float. Unlike stocks, which are perpetual, loan prices are anchored by short lives and a par value.

From case study to shining bright

Last year was a sheer case study on the merits of the asset class. Loans shook off the rising rates that roiled bond markets in the first half of 2022, while showcasing little beta1 with equities amid the runaway volatility that characterized the second half.

Now in 2023, the loan asset class continues to shine bright. On a trailing 12 months basis, loans have still far outpaced the returns of not only stocks and bonds, but even many alternative asset classes.

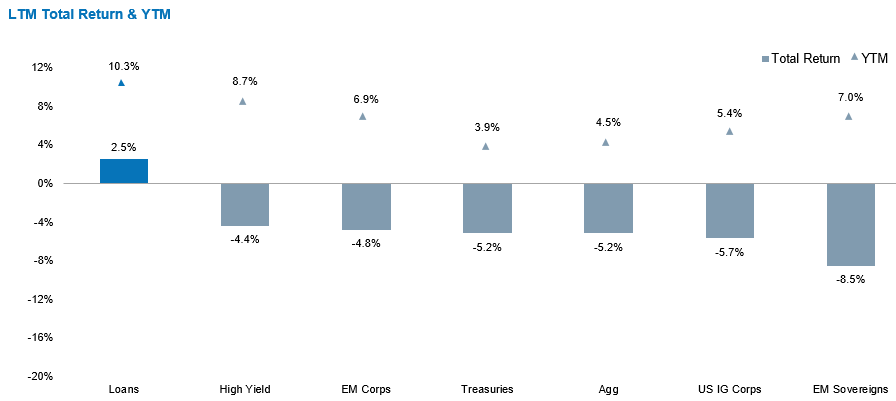

Loans continue to shine amid rising rates

To be sure, the loan market has already returned approximately 3.2% for the first quarter. Conditions in the asset class remain firm, with little supply to weigh on things (mostly higher-rated refinancings and add-ons to existing loan facilities) and plenty of institutional buying (mainly in relation to CLOs) to offset retail fund redemptions.

But what now? Here are our answers to the questions we hear from investors:

"Have we missed it?"

To those asking about timing, we see ample potential opportunity for investors today. Valuations are cheap compared to the loan market’s own history as well as to the rest of the fixed income world. And, most importantly, the absolute yield of loans exceeds that of every other major U.S. fixed income class.

At the opening of the second quarter, as of April 3, the yield to maturity for the Morningstar LSTA Leveraged Loan Index stands at 10.3%, with the dollar price of the index at 93.4. Starting yield has been the number one driver of forward total return, so we wouldn’t be surprised if loans continued to outpace looking ahead.

"What if the Federal Reserve cuts rates?"

As for the Fed, Chair Jerome Powell has openly stated that there are no plans for rates cuts in the near term ahead. In fact, policy rates are expected to remain high through the balance of the year, if not longer. If and when the Fed does cut rates, we believe loan yields will simply reflect that. For example, all else equal, a loan fund yielding 9% today would yield 8% after a series of four quarter-point cuts. That would still be a substantial yield advantage.

"What about recession risks?"

On recession risks, this topic enters the fray in any credit product with the potential for default. In our view, the key is deciphering the rubric of actual versus implied levels, and on that basis, we don’t see forward defaults approaching what would be needed to erase seven points of capital, which is the approximate inverse of the dollar price in today’s market.

To be sure, that sort of impairment would require a cumulative default rate of more than 20%, using the typical 70% recovery experience of the asset class. For context, COVID-era defaults peaked at 4%. Though fundamentals opened this inflationary period on solid footing, we think defaults may rise a bit into 2024 — tighter credit conditions could do that — but our own perspective is that this is already “priced in,” and a good amount more. Does anyone expect an environment ahead that would be five times as disruptive as COVID?

We believe firmly in the strategic case for this unique asset class. Loans are simply different, and in the current environment, we think that for suitable investors, the case for a tactical overweight can rest on high income, cheap valuations and a structural profile suggested by history to be able to blend well with other portfolio fare.

Bottom line: If you ask us, we would say that loans are shining bright. They delivered last year. They delivered in the first quarter. They appear well poised to deliver looking ahead.

1 Beta is a measure of the relative volatility of a security or portfolio to the market’s upward or downward movements.

The index performance is provided for illustrative purposes only and is not meant to depict the performance of a specific investment. Past performance is no guarantee of future results.

Morningstar LSTA US Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market.

Risk Considerations: Loans are traded in a private, unregulated inter-dealer or inter-bank resale market and are generally subject to contractual restrictions that must be satisfied before a loan can be bought or sold. These restrictions may impede the strategy’s ability to buy or sell loans (thus affecting their liquidity) and may negatively impact the transaction price. It may take longer than seven days for transactions in loans to settle. Due to the possibility of an extended loan settlement process, the strategy may hold cash, sell investments or temporarily borrow from banks or other lenders to meet short-term liquidity needs. Loans may be structured such that they are not securities under securities law, and in the event of fraud or misrepresentation by a borrower, lenders may not have the protection of the anti-fraud provisions of the federal securities laws. Loans are also subject to risks associated with other types of income like high-yield bonds. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical, currency exchange rates or other conditions.