Global stock markets made cautious progress this week following recent heavy losses

Optimism about the potential for artificial intelligence (AI) to boost growth among global technology firms managed to offset the latest round of worries about future interest rate rises. Weak economic data on both sides of the Atlantic, meanwhile, gave investors further cause for concern given last week’s dire statistics from China.

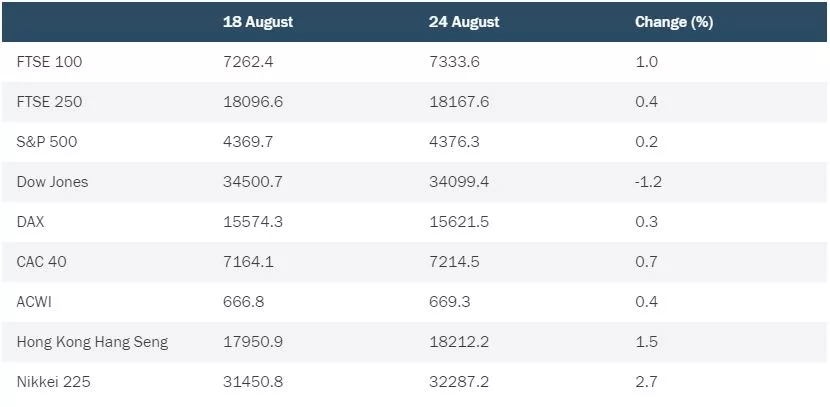

United States

On Wall Street, the Dow Jones Industrial Average ended trading on Thursday 1.2% down for the week so far, with the S&P 500 edging 0.2% ahead. Investors welcomed another upbeat earnings statement from one of America’s most important semiconductor companies, which expects to benefit to an even greater degree from the use of AI by its customers. With the technology still at a relatively early stage, markets are hopeful AI can have a transformative effect like that of the internet. There was more mixed economic data in the US, with early indicators suggesting the country’s economy had stagnated in August while durable goods orders fell sharply. The labour market continues to show resilience, however, increasing the likelihood of further interest rate rises.

UK

In the UK, the FTSE 100 closed on Thursday 1% up for the week so far, with the weakening pound helping to boost the value of various international companies listed in London. Sterling’s fall was caused partly by hopes that interest rates in Britain may peak lower than previously expected. Data showing a drop in retail sales and business activity in general has put more pressure on the Bank of England to slow the pace of rate rises. Latest figures that highlighted an improvement in government finances were welcomed, but Chancellor Jeremy Hunt played down the possibility of implementing tax cuts before next year’s general election.

Europe

In Frankfurt, the DAX index ended Thursday’s session up 0.3% for the week, while France’s CAC 40 gained 0.7%. Prices for natural gas in the eurozone, which had spiked earlier in the week, fell back after an industrial dispute at a major Australian supplier was resolved. However, European economic performance continued to underwhelm, with Germany recording its fastest decline in business activity in three years and France also showing weakness.

Asia

In Asia, the Hang Seng index in Hong Kong rose 1.5% to bring its recent run of losses to a halt, at least temporarily. There were no further shocks from China’s beleaguered property sector, though investors were disappointed by a smaller-than-expected interest rate cut by the country’s central bank. Positive earnings figures posted by several major firms late in the week supported gains on the wider market. Japan’s Nikkei 225 index of leading shares, meanwhile, advanced 2.7% with the country’s biggest technology names displaying renewed strength on the back of positive news from the US semiconductor industry. In addition, the Bank of Japan’s decision to raise the cap once more on bond yields provided a boost for share prices in the financial sector.

Note: all market data contained within the article is sourced from Bloomberg unless stated otherwise, data as at 24 August 2023.