Experienced hikers know that descending can be more arduous than going up the hill. Fortunately, robust gear can help you overcome what obstacles there may be on your way. What equipment should you buy, and what should be left sitting on the shelf?

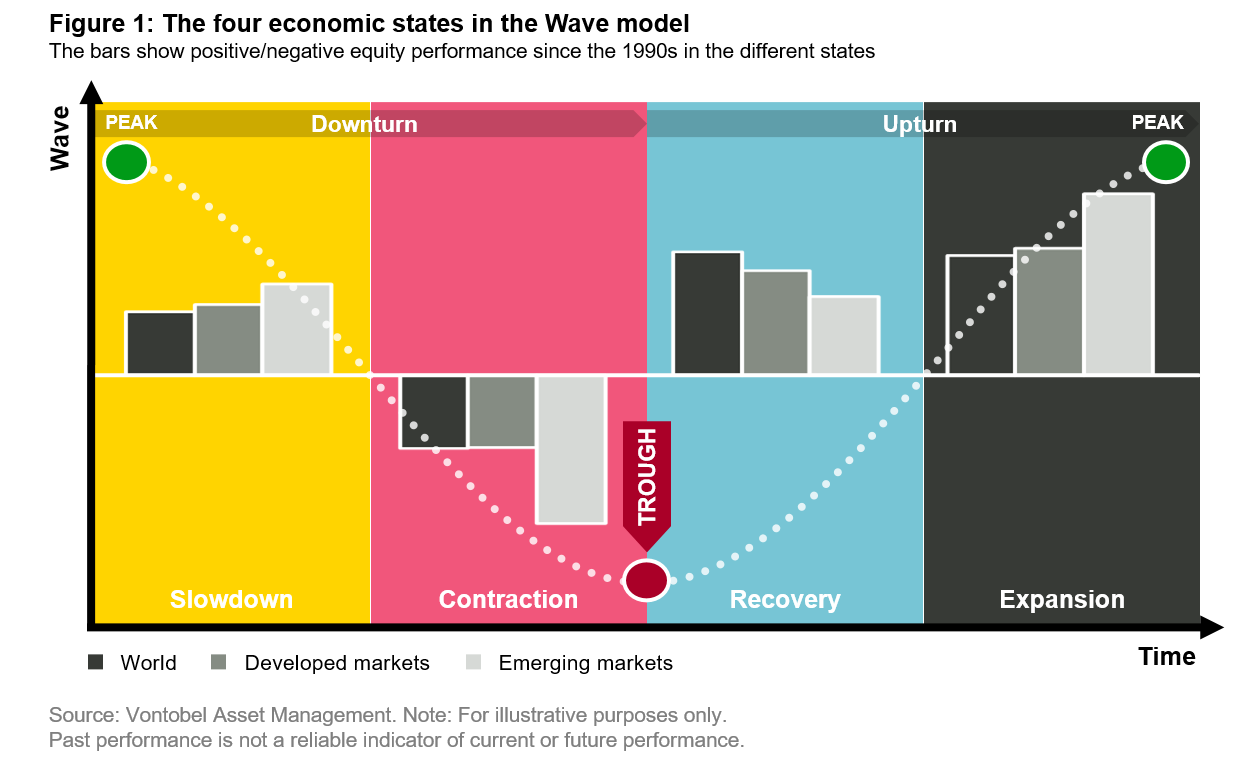

Before you consider the purchase of a special brand of trekking poles, hiking boots – or, for investors with a focus on emerging markets (EM), a specific security to make your journey more secure – let’s first take a look at the GPS tracker. There’s little doubt that we have indeed left “Peak Growth Mountain” behind, definitely in emerging economies but increasingly in developed markets as well. That’s what our business cycle model “Wave” (see figure 1) suggests, and this is crucial information for investors taking a top-down macroeconomic view.1 After finding your location on the map, you can start scanning the landscape for potential opportunities (or danger zones), using country, sector, and even theme-specific binoculars.

But first things first. Business cycles start with an economic recovery, typically followed by an increasingly unsustainable expansion triggering inflation and prompting central banks and governments to implement countercyclical “restrictive” policies, such as rate hikes. These policies stall the economic recovery, causing growth and inflation to peak. At that stage, the economy enters a slowdown followed by a contraction, which often coincides with a recession. This is usually the time when central banks and governments change tack, supporting the economy with “expansionary” policies such as tax cuts. What follows is another recovery, and the business cycle starts again.

So much for theory. In real life, things are more complicated, with business cycles often breaking this pattern, as they did during the pandemic crisis, for example. The stringent lockdown measures in early 2020 that threw the global economy headlong into the worst maelstrom since last century’s Great Depression were followed by an economic recovery that was similarly spectacular.

Where is the business cycle taking us?

The mid-point of an economic slowdown tends to be a supportive environment for cyclical asset classes.2 But could we already be getting close to the beginning of the next stage of the business cycle? To get a clearer view on this, and to identify the possible winners and losers, you as an investor will have to make assumptions about the future development. The key element here is to evaluate and anticipate the steps of governments and central banks that make or break an economy. Our business cycle model has worked well so far this year, pointing at an expansion-to-slowdown transition before it materialized. Currently, the Wave model shows a 67 percent probability that the global economy will continue to slow in the short term.

Eyes on EM hard-currency debt

This suggests a cyclicals-focused but well calibrated equity strategy. Let’s not forget that the longer we are in a slowdown, the bigger the risk of slipping into contraction territory, which is why defensive dividend-paying stocks, typically found in markets such as Switzerland, are becoming increasingly attractive. Due to their defensive nature, they are likely to outperform in a shift to a more adverse contraction scenario, but could participate in an equity market rally if the growth environment improves again. The continued edge of dividend yields (dividend payment relative to a company’s share price) over bond yields is another argument for dividend strategies.

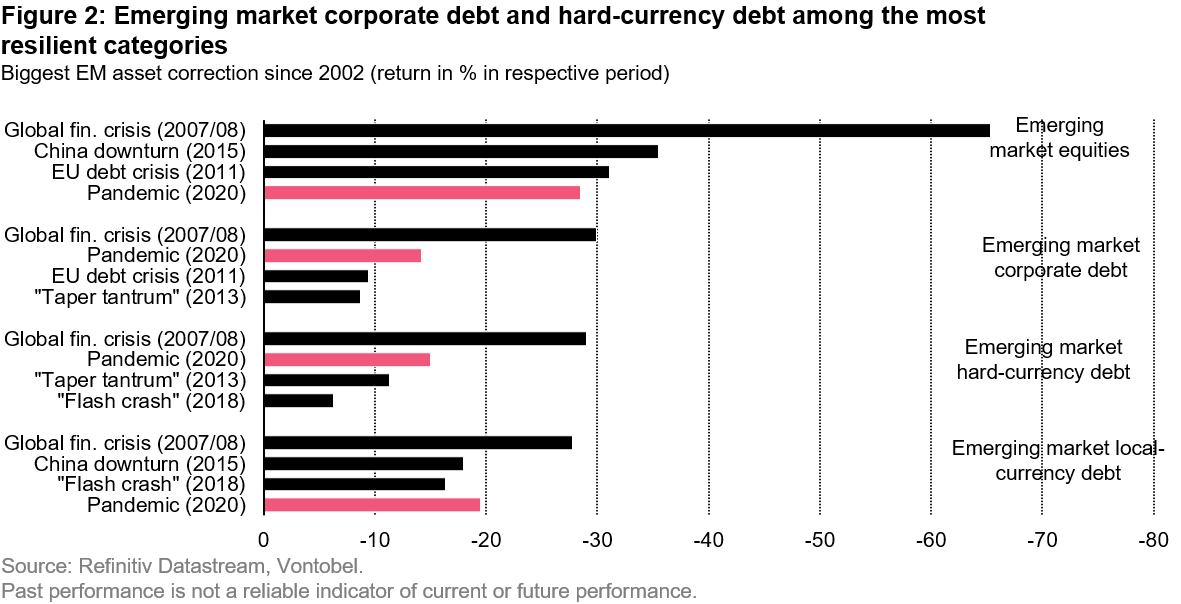

Generally, the attraction of defensive assets is particularly evident in emerging markets, where the risk of entering the contraction phase is significantly higher than in developed economies. This leaves us with a preference for hard-currency debt within the region. According to our analysis, emerging market hard-currency debt has generated slightly positive returns even during periods of economic contraction. Moreover, draw-downs – the biggest observed loss measured in terms of peak-to-trough difference – have been lower than in other asset classes (see figure 2).

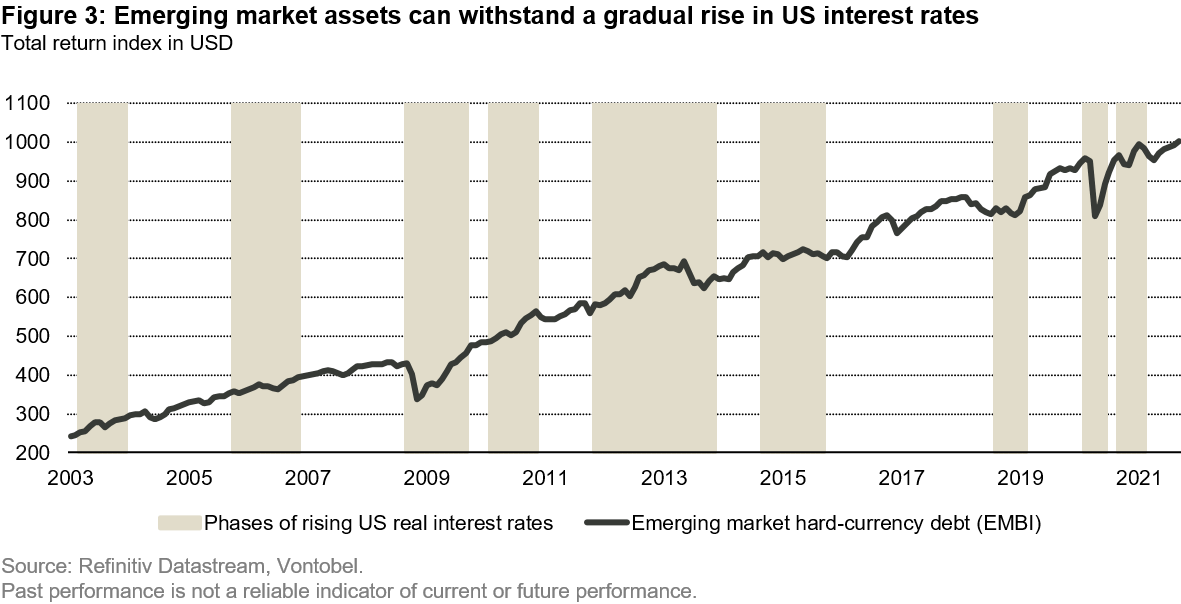

Our view on prices – we are probably past the “Peak Inflation Mountain” as well, also supports the rationale for engaging in this fixed income segment. With upward price pressure easing, central banks will be in no hurry to tighten monetary policy much more from here. In such a scenario, EM bonds denominated in hard currencies have room to gain in value, lowering the yield difference to US government bonds. The risks for emerging market bonds include a possible tightening of monetary policy in the West: Should the US Federal Reserve hike interest rates and the US dollar rise significantly as a consequence, dollar funding would become more expensive, leaving emerging markets in the lurch. However, we don’t expect any such move by the world’s most powerful central bank before the end of 2022. Therefore, any USD strength may only materialize in the second half of 2022. Moreover, phases of moderate USD appreciation and a slow rise in US Treasury yields need not be negative for emerging market assets, which have proven their resilience in times of gradually increasing US rates (see figure 3).

Are emerging market equities a buy already?

Whilst emerging market assets tend to perform well in an economic slowdown, EM shares have underperformed so far this year. Between February and late August 2021, emerging market equities suffered two major downturns of more than 10 percent each, both times weighed down by index heavyweight China. At the same time, eastern European and Latin American shares performed well in the first half of 2021. Those markets are likely to remain supported in the near term because these economies are still on the upward growth path, unlike their Asian counterparts.

There are two main reasons for the overall sluggishness of EM equity markets. China’s economy started slowing down in February, around the time its equity market began to underperform. On top of that came the regulatory crackdown against Chinese technology companies and real estate developers that triggered the second leg of the slump between June and August. After a decade of regulatory laissez-faire, the initiative by Chinese watchdogs can be interpreted as an understandable move to catch up with western regulatory standards. Even so, it was an eye-opener to many global investors who have never contemplated the possibility of such a massive regulatory push against China’s national tech champions.

Therefore, the recent sell-off needs to be seen in the context of market participants trying to price in regulatory risks. Are we there yet? Concerns may linger, not the least because Chinese authorities may find it useful to tighten regulatory screws further, for example through the personal information protection law (PIPL), which takes effect in November 2021. What investors will want to see is more transparency in the regulatory process. Once this happens, the recent correction in emerging market equities will probably be seen as an attractive buying opportunity. Moreover, China will have to find ways of supporting the economy in light of recent underwhelming data. Chinese authorities have recently approved additional stimulus measures, a move that may usher in a stabilization of the local equity market.

Some hedging against inflation makes sense

Even though our business cycle model is not designed to predict cyclical inflation trends, it enables us to draw conclusions regarding price levels. The data series we use don’t suggest permanent inflation pressure, even indicating somewhat lower inflation rates going forward. However, as labor markets continue to tighten, the risk of accelerating wage growth rises. Moreover, we see the emergence of a possible inflation driver tied to the corporate world’s adaptation to sustainability requirements. To incentivize companies to go “green”, governments tend to increase the costs of fossil energy sources, which is likely to increase prices for products and services. Therefore, adding commodities to a portfolio as an inflation buffer makes sense, in our opinion.

Be prepared as you’re heading for the base camp

Things seemed easy enough on the way to “Peak Mountain”, but now, we have a new situation. Many mountaineering expeditions fail on the way down from the summit because of poor preparation or bad judgment. Smart investors with the necessary risk-mitigating equipment should arrive safely at base camp, ready to take on the next challenge.

1. Also see our recent article “ How to check if peak talk has substance to it ”.

2. https://am.vontobel.com/insights/how-to-check-if-peak-talk-has-substance-to-it