High and persistent services inflation in the US has prevented overall inflation from returning to the Federal Reserve’s 2% objective. In response, the Fed has postponed interest rate cuts. To assess the prospects for services inflation, in this Macro Flash Note EFG Chief Economist Stefan Gerlach looks at the behaviour of consumption spending on services.

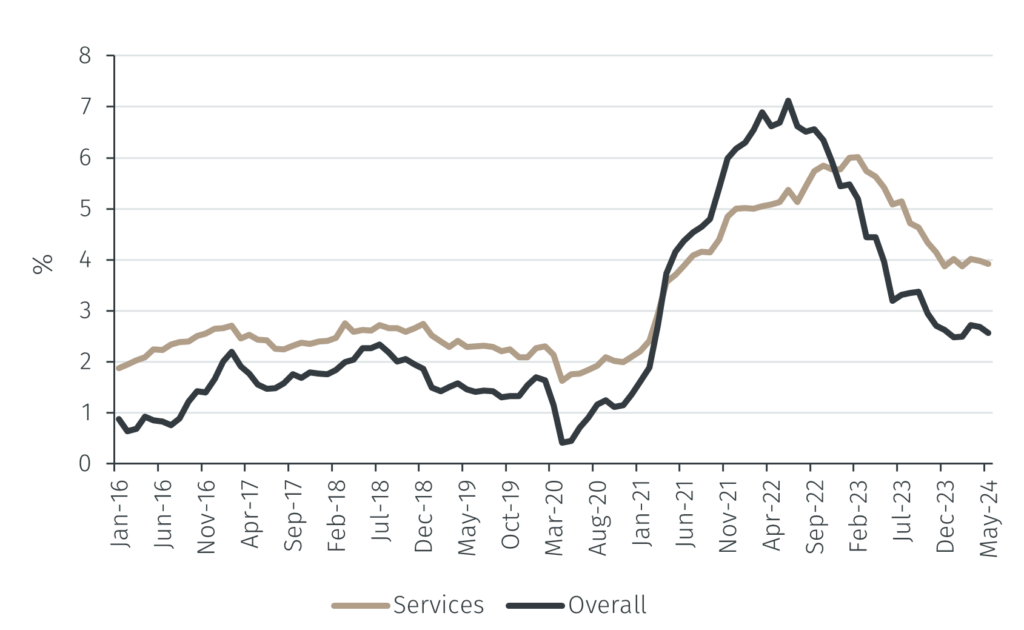

US services inflation as measured by the personal consumption expenditure (PCE) index has remained robust, peaking at 6.0% year-on-year in January – February 2023 and declining only to 3.9% in May 2024. Since services are a large part of household consumption, it has prevented overall inflation from returning to the Fed’s 2% inflation objective (Figure 1). In turn, this has led the Federal Open Market Committee to postpone cutting interest rates.

Chart 1. US PCE inflation (YoY)

Why has services inflation stayed so high? To address this question, it is useful to look at the behaviour of consumer spending on services.

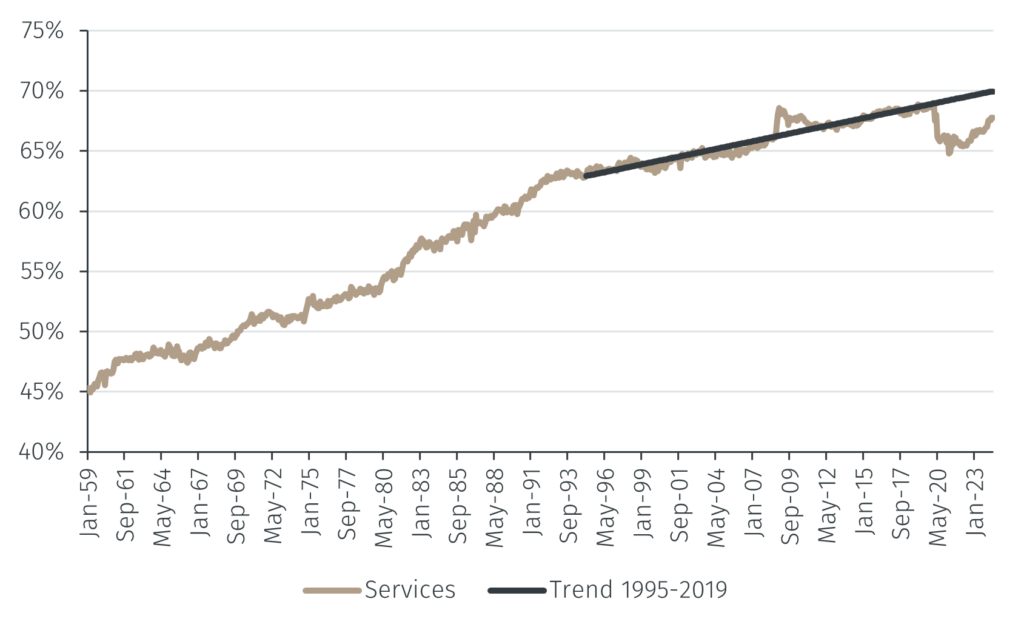

The figure below shows the proportion of consumer spending associated with services. It has been gradually increasing over time, peaking at 69.0% in January 2020 as the Covid pandemic started.

With households worried about contracting Covid and with restaurants, bars and similar institutions subject to lockdowns of varying degrees of severity, consumer spending on services fell sharply, reaching 64.8% of the total in March 2021. It has since started to recover but stood at 67.7% in May 2024.

While it is difficult to determine exactly what the “normal” level of consumption spending on services should be, the figure shows a simple linear trend, estimated over the period 1995-2019. This serves a means of ascertaining whether today’s spending on services is high or low relative to that trend. The rough estimate it provides suggests a normal level of 69.9%. If so, consumption spending on services as a fraction of overall consumer spending was a little more than 2% lower than normal. That implies that consumer spending on services has not yet recovered fully after the pandemic and that services inflation may remain high for some time to come. If so, the Fed may delay interest rate cuts for longer than is currently expected.

Chart 2. Consumer spending on services (as a fraction of overall consumer spending)