Financial markets have been on a roll for close to a year now, pumped up by monetary and fiscal policy on steroids. This has led some observers to question whether such unstinting fiscal spending and supposedly unconditional monetary policy support can really enable specific economies – like the US – to escape the iron law of the business cycle.

But as the cycle progresses and the exceptional measures adopted have put the economy back on a more promising trajectory, bringing growth back on track will cease to be the primary concern. At that point, central bankers will leave centre-stage and begin focusing more on price and financial stability than on GDP growth per se. Meanwhile, a number of fiscal support programmes – whether implemented or announced – will get toned down as the consensus on where to take political and economic policy weakens in the face of an economy that seems to be powering ahead under its own steam. In short: the law of the business cycle will take back the reins it previously lost to emergency crisis-fighting measures.

But all that raises any number of questions, particularly in light of the massive support measures that have characterised this most unusual period. For example, what will happen once fiscal and monetary stimulus is removed? How will financial markets react once conditions recover a semblance of normality? Will they go into free-fall? Succumb to the law of gravity? Or will they revert to what appears to be their long-term trend?

As we’ve pointed out several times over the past few months, the United States has once again emerged as an archetype for both the crisis and post-crisis periods.

Monetary Policy Approaching an Inflection Point

The Federal Reserve (Fed) is sticking with its baseline scenario – that the recent rise in inflation is temporary – while acknowledging that higher prices might prove more persistent than initially forecast after all. Its policymakers have thus adapted their messaging and taken a tougher stance. They have hinted that they may scale back their asset purchases in the months to come – possibly as early as this autumn if the economic indicators are still pointing in the right direction.

This change of gears will likely be extremely gradual, and the financial-market response demonstrates that the prospect of a return to more conventional monetary policy comes somewhat as a relief. Shorter-term yields – which are most sensitive to expected shifts in monetary policy – have risen. At the same time, longer-term yields – which tend rather to reflect long-range economic growth forecasts – have stood pat, or even fallen below where they were before the Fed changed its tune. This also explains why risk assets have performed so well.

Fed Chairman Jerome Powell has stressed that his job also consists of making sure he doesn’t get caught off guard by inflation. So the prospect of a US economy deviating from the path of a classical business cycle has grown somewhat dimmer.

Financial markets do not seem to expect an error in monetary policy – either through overheating or abrupt tightening. Yet a number of problems could well surface in the process.

To start with, now that inflation expectations have adjusted, attention has been shifting to the state of the job market. This increasing dependence on economic indicators can be a source of volatility, because those indicators are themselves volatile due to frequent revisions and seasonal adjustments, which have become particularly erratic in the atypical business cycle we are experiencing. There is a peril that the Fed will be forced to hike in response to remarkably robust employment figures2 – whereas the financial system can’t afford higher financing costs, given that excessive leverage has made the system extremely sensitive to the level of interest rates. And that highlights the paradoxical nature of the world we live in: a run-up in inflation (fuelled by rising wages and/or property prices) could ultimately turn into a deflationary shock when the speculative bubbles created by exceedingly supportive policies finally pop3.

This means that Mr Powell will have to engage in a difficult monetary-policy balancing act, and the risk of slipping up will be that much greater in such a fast-growing economy.

The Business Cycle is Progressing, so the Strength of GDP Growth Must be Carefully Monitored

In addition, though the move to tighter monetary policy (and therefore tougher financing conditions) may seem remote at this stage, it will eventually result in less buoyant GDP growth. That, indeed, would be the purpose of such a change. And it pays to recall that every action produces an opposite reaction.

Though often ahead of the crowd, the United States is in this case part of a broader trend. As we pointed out last month, other central banks in the developed world have also started preparing financial markets for a similar policy shift. The same goes for a number of so-called emerging economies where the changeover has already begun and/or where investors are already pricing in tighter monetary policy for the months to come.

Central banks appear so far to be adroitly negotiating this turn; their move towards more hawkish policies has not weighed on financial markets in the process. But while abundant liquidity is beneficial to cyclical assets and carry strategies, its subsequent withdrawal means less supportive conditions for financial markets. It’s therefore advisable to start bracing for a decrease in available liquidity – however gradual – and an environment of less lavish monetary policy.

When Fiscal Stimulus Winds Down

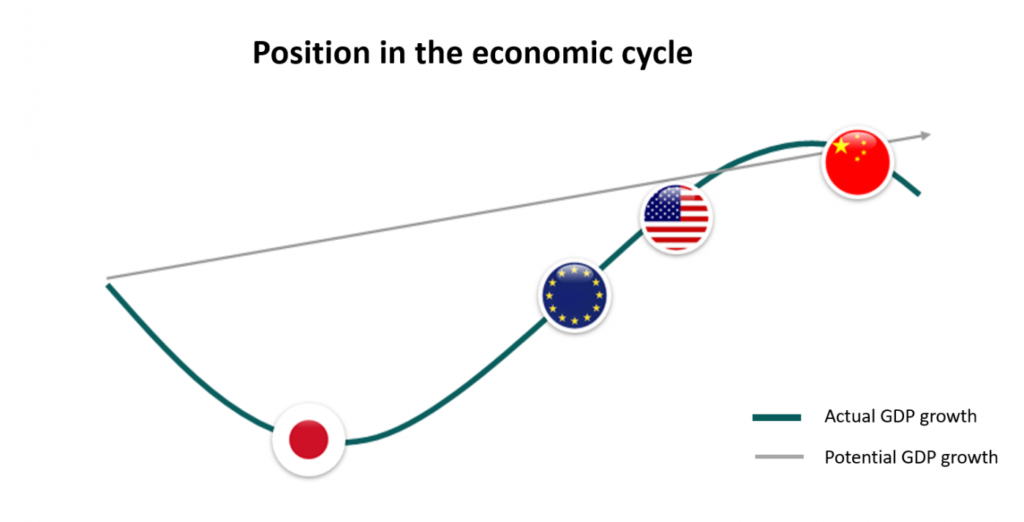

The business cycle is similarly shaped by governments’ economic policies, and is unlikely this time to go abruptly into reverse. For the coming quarters, the US and European economies are on course to post double-digit growth on an annualised basis – driven by rebounds in consumer spending, world trade and tourism. But a subsequent slowdown can be expected. Because the Chinese economy is further along in the business cycle, it is already operating at a more moderate pace, and without government intervention, output will likely fall short of China’s potential growth rate by the end of this year. That shift will spill over to the European economy, which is highly sensitive to Chinese GDP growth.

While we don’t expect fiscal spending to contract markedly in the second half of 2021, the process of phasing out the emergency measures that have dominated these past 18 months is nonetheless now on the horizon. Those measures have helped save countless jobs and prevent a solvency crisis, but they have also led to a drop in the number of bankruptcies relative to a “normal” year – a most remarkable achievement indeed6. We can accordingly expect that when these lifelines get taken away, we will see a sharp rebound in business failures. Here again, the iron law of the business cycle is likely to come back in full force, militating in favour of extremely careful corporate bond-picking.

Meanwhile, the Biden administration’s federal spending ambitions will most likely get dialled down, particularly as the Democratic Party’s razor-thin majority in Congress will make negotiations highly challenging. So there is a genuine risk that the stimulus package will prove to be less potent than initially anticipated – and that the current phase of fiscal expansion will give way to fiscal contraction next year.

Adjusting Portfolios to the Prospect of Less Monetary and Fiscal Support

The business cycle is moving along. Predicting when growth will peak is no easy job, but judging by past experience, the withdrawal of liquidity by central banks is typically an early sign of the cycle rolling over. For the time being, it looks like the monetary policy turn is being skilfully negotiated. Financial markets are now anticipating a rise in key rates from November 2022 onwards, which will represent a greater challenge to hopes of sustainably stronger growth in the long term, and therefore to long-term rates too. The coming months could therefore see less volatility in the bond markets. We have tactically neutralised our short positions and we expect this flattening of the yield curve to continue due to the ambivalence of the Fed’s reaction function.

This phase of the economic cycle, along with such an environment, tends to be particularly favourable to stocks whose earnings growth trajectories are more autonomous, meaning less dependent on the economic cycle. They are the backbone of our investments.