Strategic shifts towards decarbonisation and dual supply chains, inflation and rising cost of capital are starting to revert investors’ focus back towards corporate profits and cashflows. This move is supportive of value investing in Asia ex Japan. Cyclical, old economy and financial stocks are likely beneficiaries.

Value equities in Asia ex Japan have had a strong rebound since Nov 2020, outperforming the regional index by 15%.1 We believe this re-commencement of value’s outperformance has just begun in Asia, well supported by the economic cycle, implied market expectations, and investor positioning.

As the pendulum starts its mean reversion journey from one end (optimism over growth stocks) to the other end (renewed focus on profits and cashflows), we see significant mispriced stock opportunities for bottom-up value investors in Asia.

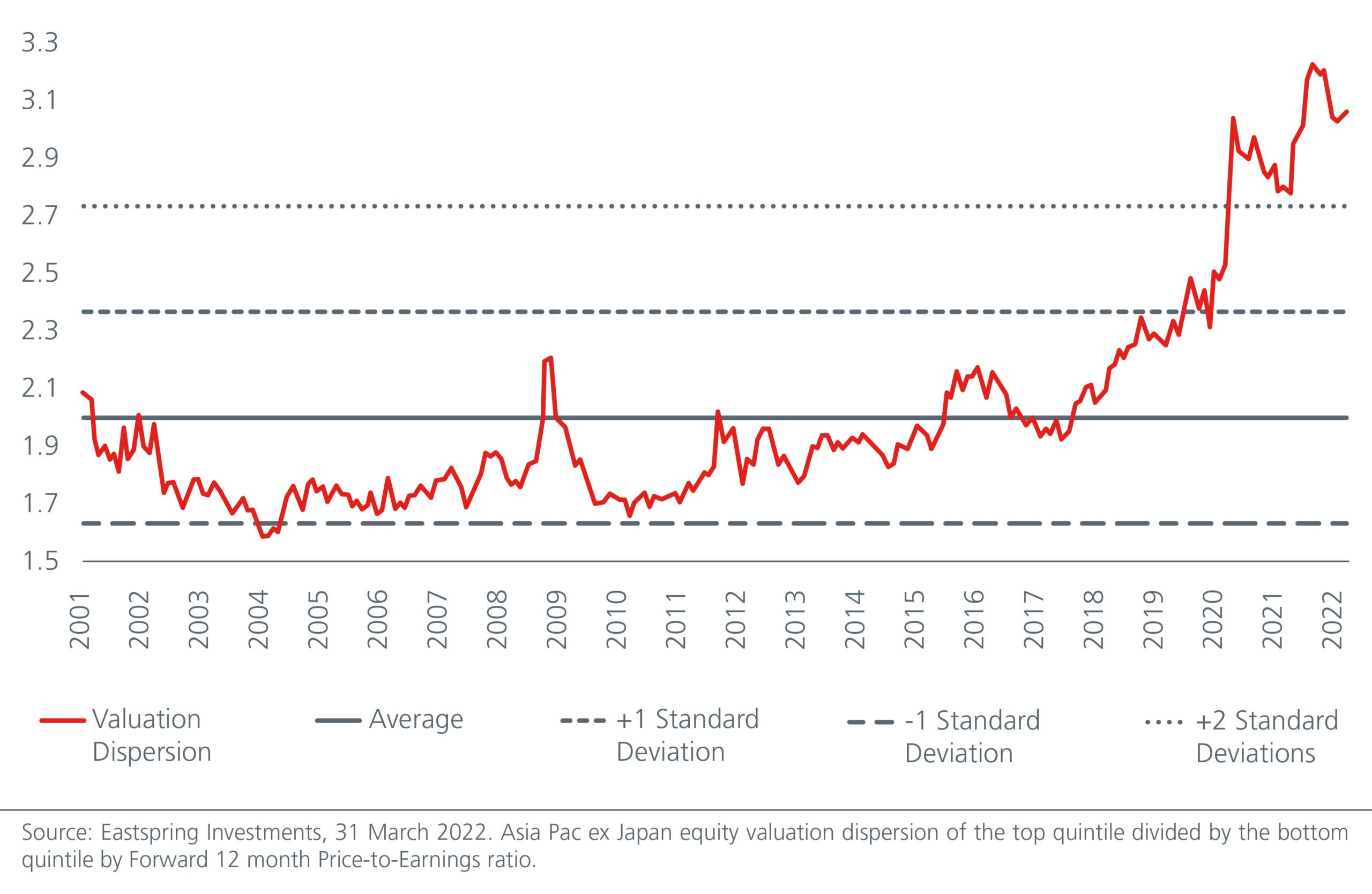

Fig 1: Valuation dispersion (and hence alpha opportunities) stays large despite the recent value outperformance versus growth

Economic shifts and investor positioning

Global decarbonisation, the focus on sustainable growth and the shift to dual supply chains are driving strategic shifts in Asian Corporates, leading to far different outcomes in their investing and operating behaviours than the prior decade of asset light growth.

The change in expectations around inflation and interest rates is refocusing the market’s attention towards profitability and free cashflows, unlike the TAM/GMV2-only focus of growth investors over the prior decade. Similar investing trends around the globe too bode favourably for their suppliers, who are mostly in Asia. We believe the resulting economic cycle in Asia is supportive of value investing. Beneficiaries are likely to be cyclical, old economy and financial stocks.

Mr. Market having enjoyed years of growth investing is not yet reflecting any of this potential regime shift. This is reflected in the extreme valuation dispersion between value and growth and quality stocks, and the continuing overweight positioning in growth sectors as reflected in sell-side surveys.3 See Fig. 2.

The sharp value underperformance over the prior decade led to several investors giving up on value investing philosophically. Career risk and the inertia to look beyond the next quarter also explains the slow shift out of the yesteryear’s winners. We believe this contrarian positioning offers us a unique advantage to exploit the opportunity using our differentiated investment process.

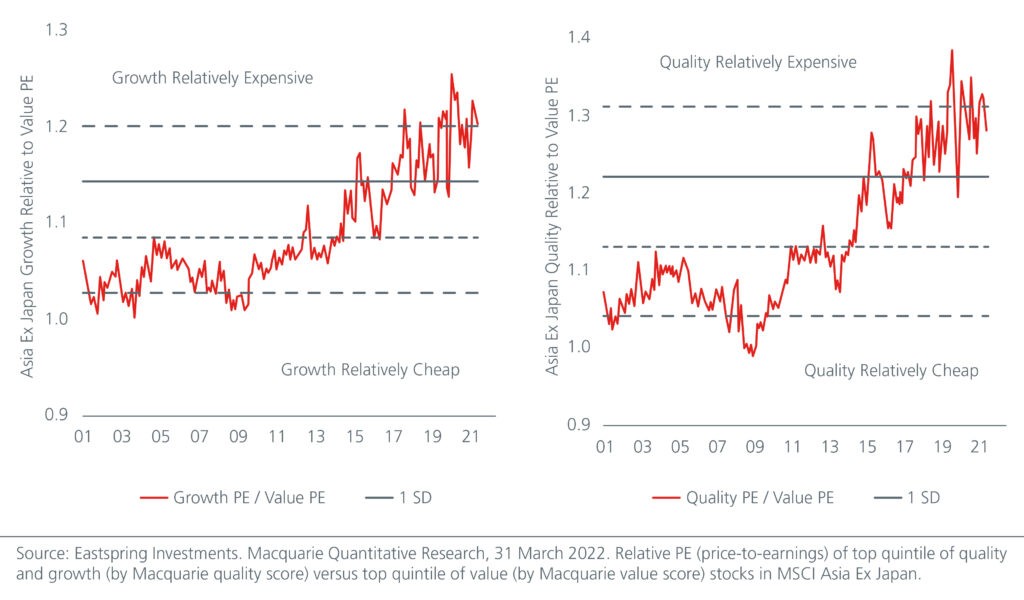

Fig 2: Asian Value names substantially undervalued compared with Quality and Growth stocks

De-rated Asian markets present attractive pickings

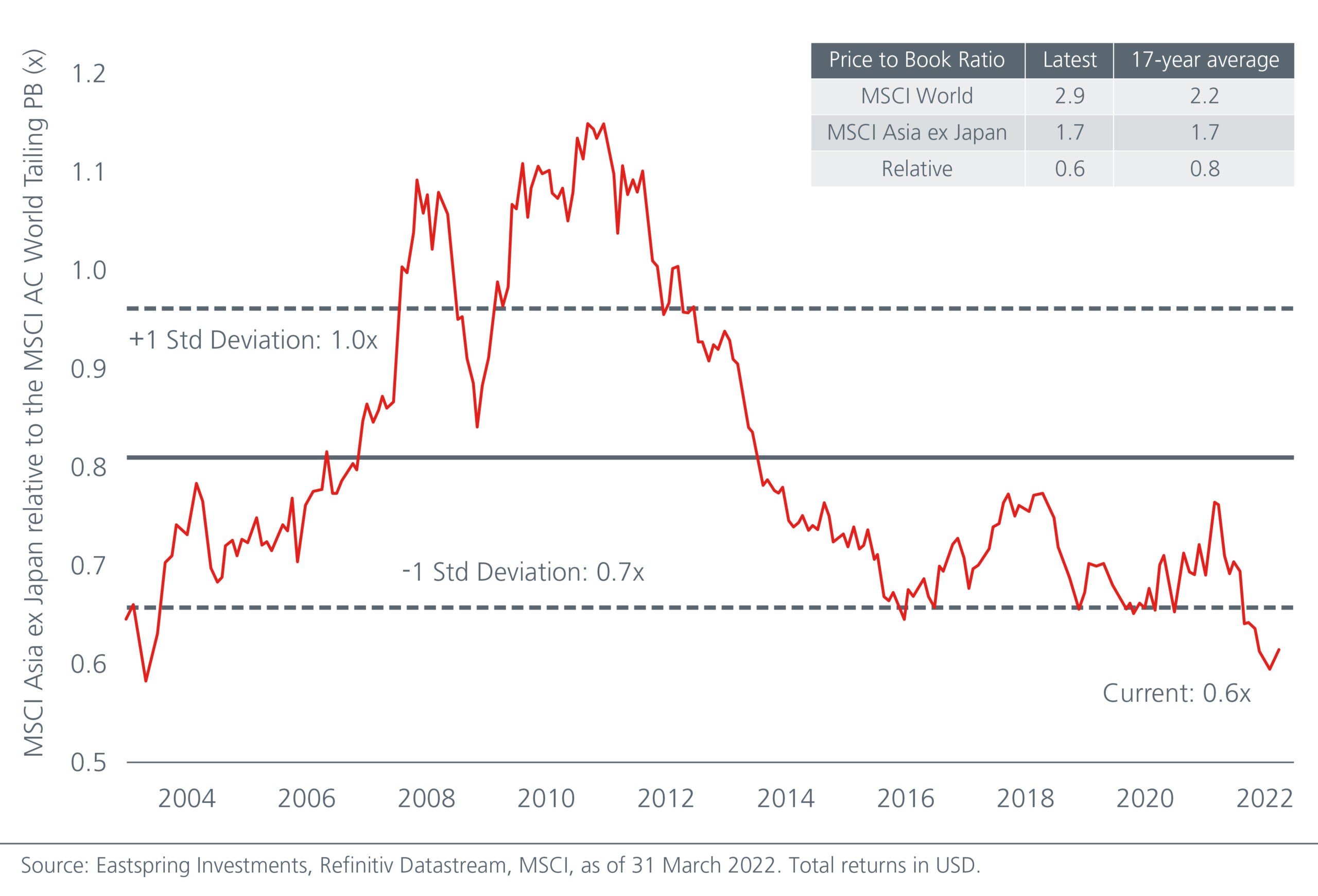

Asia ex Japan markets declined 21% over the last year4 driven by a slower re-opening than the rest of world and regulation in China. This has driven valuations to a price-to-book ratio of 1.7 versus 2.9 for MSCI World, the widest since the tech bubble selloffs in the late 1990s. See Fig. 3.

This discount is out of range compared to the shorter post-2014 history, a period of significant outperformance in growth stocks. As several of the macro and style trends of the post 2014 cycle reverse, it presents opportunities for Asian value names to reduce this discount.

Fig 3: Asia ex Japan equity markets are attractive versus the world

Significant value opportunities

We see significant value in banks in both developed and emerging Asia. The strategic shift among Corporates (as discussed earlier) combined with higher interest rates and higher inflation provide banks with a good opportunity to grow their earnings after years of low margins (in developed economies) and poor asset quality (in emerging economies). ASEAN banks further benefit from asset quality normalisation coming out of the delayed reopening in their economies over 2021. Market implied returns and investor underweight positioning suggest we are getting paid to take on this normalisation, without running into investor crowding.

We continue to like several restructuring opportunities in Asia where management teams are driving large-scale change in a firm’s culture, operations, and balance sheet to revert returns to their historical mean. We believe our understanding of this internal change and an edge in understanding normalised returns beyond the next few quarters allow us to take outsized positions in these companies, without worrying about short-term macro volatility.

We are also seeing mispricing opportunities in large public-sector companies in China. Many companies have de-rated over the last 2 years due to the US sanctions, the property downcycle and the trade war concerns despite no negative impact to their medium term cashflows and improved visibility in their ESG journey. As we look beyond the recent COVID-induced lockdowns, we are also attracted to the services sector i.e., travel, leisure, and advertising. These businesses have robust moats and positive cashflows and are outside the limelight of their crowded bigger peers.

Why we are invested in Value

At Eastspring, our value philosophy is premised on the observation that human emotions and behavioural biases distort investment decision making. This leads investors to focus on the recent past, extrapolate into the near future, and thus overpay for the promise of growth and perception of quality.

Our disciplined value approach relies on a proprietary screening of outlier de-rated stocks within our Asian investment universe, a focus on medium-term sustainable returns, and an experienced team of investors debating the best investment opportunities from this basket of mispriced stocks. Our investment edge is in understanding the range of medium-term outcomes in this opportunity set, versus what is implied in the current market expectations.

We believe the starting point for Asia ex Japan’s valuations, the re-commencement of value’s outperformance, and the distinct regime shift in the economic cycle and corporate strategies bode well for Asian equities. The investment style allocations over the last five to seven years and investor crowding in ‘me-too’ strategies should get re-evaluated at this point.

This is the seventh of a series of eight articles which examines the different investment strategies investors can adopt to tap on the opportunities that are emerging in Asia.

Footnotes:

Sources:

1 Refinitiv Eikon Datastream, MSCI Asia ex Japan Index versus MSCI Asia ex Japan Value Index, total return indices, USD to 29 April 2022.

2 Total Addressable Market/Gross Merchandise Value

3 Bank of America’s Fund Manager Survey, April 2022.

4 Refinitiv Eikon Datastream, MSCI Asia ex Japan Index USD total return index as of 29 April 2022.

Disclaimer:

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore and Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws.

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (531241-U).

This document is produced by Eastspring Investments (Singapore) Limited and issued in Thailand by TMB Asset Management Co., Ltd. Investment contains certain risks; investors are advised to carefully study the related information before investing. The past performance of any the fund is not indicative of future performance.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only) by Eastspring Investments (Luxembourg) S.A. – UK Branch, 10 Lower Thames Street, London EC3R 6AF.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author on this page, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this posting is at the sole discretion of the reader. Please consult your own professional adviser before investing.

Investment involves risk. Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments (excluding JV companies) companies are ultimately wholly-owned/indirect subsidiaries/associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company, a subsidiary of M&G plc (a company incorporated in the United Kingdom).