Markets this week have been gripped by apprehension over the potential fallout in the banking system from the abrupt end in 2022 to the low interest rate regime. After 40 years of falls in inflation and interest rates, the Covid pandemic set off a sea change in macroeconomic fundamentals, triggering an unprecedented tightening of monetary policy by the US Federal Reserve and European Central Bank. The Fed and ECB now face the challenge of pursuing their mandates to ensure price stability without undermining financial stability.

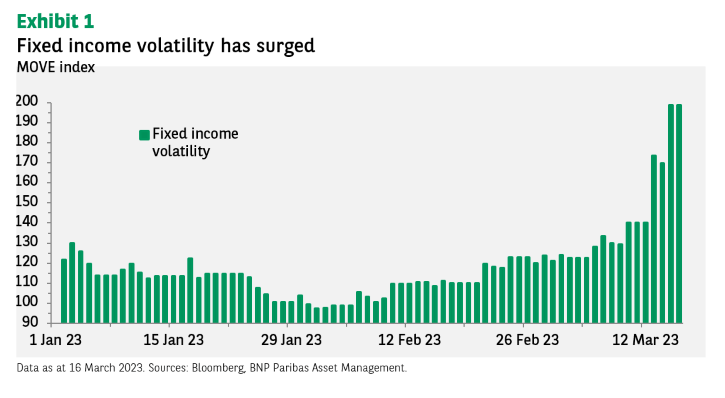

Volatility in financial markets has spiked (see Exhibit 1 below) in the wake of the sudden collapse of Silicon Valley Bank (SVB) and Signature Bank (SBNY), two mid-sized US commercial banks. Their demise was brought about by a confidence crisis and a subsequent run on deposits.

SVB was vulnerable because it had invested in long-maturity US Treasuries at a time when interest rates were much lower. It had not properly hedged the interest-rate risk and hence was obliged to sell these at loss to meet customer demands for their funds. News of the losses set alarm bells ringing among investors, worried that other financial institutions might be vulnerable in light of the paradigm change in the interest rate regime.

Fed takes steps to restore confidence

The failure of SVB was followed by that of Signature Bank, triggered again by a confidence crisis and a run on deposits. Like SVB, Signature Bank’s business model was unusual: it focused on large deposits from its digital assets business.

To restore confidence in the US banking system, regulators announced on 12 March that all deposits at SVB and Signature Bank would be guaranteed by the US authorities.

The Fed said it would make additional funding available to banks to ensure they have ‘the ability to meet the needs of all depositors’ through a new Bank Term Funding Program (BTFP). This will offer credits at par for up to one year to banks pledging US Treasury securities, mortgage-backed securities and other high-quality collateral. Pressure through mark-to-market valuations is thus alleviated for up to one year.

US banks support regional lender

On 16 March, a group of 11 US banks announced they would deposit USD 30 billion at San Francisco-based First Republic Bank in a joint effort to bolster its finances and limit fallout among US regional banks.

Four of the biggest banks in the US — JPMorgan Chase, Bank of America, Citigroup and Wells Fargo — contributed USD 5 billion each. Goldman Sachs and Morgan Stanley will contribute USD 2.5 billion each and BNY Mellon, PNC Bank, State Street, Truist Financial and US Bancorp will each add USD 1 billion.

The deposits are uninsured, the banks said — effectively making them an expression of confidence in First Republic’s future. In announcing the deposits, the banks said recent events did nothing to undermine the banking system, but that they were deploying their financial strength ‘where it is needed the most’.

US Treasury Secretary Janet Yellen and Fed chair Jerome Powell are believed to have orchestrated the deal. They declared the show of support for First Republic to be ‘most welcome’. First Republic’s share price ended 16 March up by almost 10%, erasing earlier losses, while the S&P 500 index rallied 1.8% on the day, marking its best day since January.

Contagion to Europe

Events in the US set in motion an uninhibited search for weak links in the banking system. Spillover to Europe occurred on 15 March, regardless of a different fundamental and regulatory environment.

A slump in its share price of around 30% on 15 March led Credit Suisse (CS) to appeal to the Swiss central bank for support. This was forthcoming when the Swiss National Bank (SNB) and the Swiss Financial Market Supervisory Authority FINMA issued a statement asserting that the problems of certain US banks did not pose a direct risk of contagion for the Swiss financial markets.

If necessary, the SNB said, it was readiness to provide CS with liquidity. CS rapidly took up this offer, announcing that it was taking decisive action to pre-emptively strengthen its liquidity by intending to exercise its option to borrow from the SNB up to CHF 50 billion under a Covered Loan Facility as well as a short-term liquidity facility, fully collateralised by high-quality assets.

CS also announced it would buy back CHF 3 billion (USD 3.2bn) in senior debt securities.

Markets reacted positively to these developments on 16 March with the EuroSTOXX 600 bank index, which includes the region’s major banks, up slightly.

How do the Fed and ECB proceed?

Following SVB’s collapse and the closing of Signature Bank, we expect the Fed to seek to separate monetary policy from short-term market strains and distress. For this reason, we still expect the Federal Open Markets Committee (FOMC) to proceed with a 25 basis point rise of the federal funds rate on 22 March.

Funding pressures will accelerate a tightening in bank lending standards that has been underway for a year, reflected in:

- A decline in corporate bond issuance, particularly pronounced in leveraged finance

- A tightening in bank lending standards as reflected in the Fed’s own senior loan officers survey, dominated by regional banks.

The Fed will likely want to avoid surprising markets with the March rate decision.

The Fed Primary Dealer Survey (deadline now extended by one day) will give officials some clarity on what market participants expect. It seems probable that they will digest the survey results, determine how the markets are functioning and devise a strategy. This could, for example, involve Chair Powell appearing in the media over the weekend or perhaps writing a newspaper op-ed.

Major repricing across markets

The events in the US injected significant volatility into asset markets. At one point, the yield of the 2-year Treasury note had fallen by almost 120bp relative to its level a week earlier.

Turmoil at US regional banks elevated uncertainty over the Fed’s near and medium-term rate path, with a wide distribution of possible outcomes. Expectations for end-2023 policy rates have fluctuated wildly intraday and traded through a nearly 200bp range in less than a week.

Although daily moves of 50bp or more are unlikely to continue, we expect volatility to probably remain high. Markets must balance the rate rising cycle continuing against a likely tightening credit impulse and the potential for earlier rate cuts than expected from the Fed.

The US Treasury yield curve will likely reduce its inversion as a lower terminal rate may lead to increased inflation risk and term premiums. Conversely, a rapidly weakening US economy could lead to resurgent steepening driven by a rally in long-dated debt.

Since a precipitous fall at Monday’s opening, the S&P 1500 regional bank index has not as yet mounted a sustained rally, but it has also failed to break the low set on Monday.

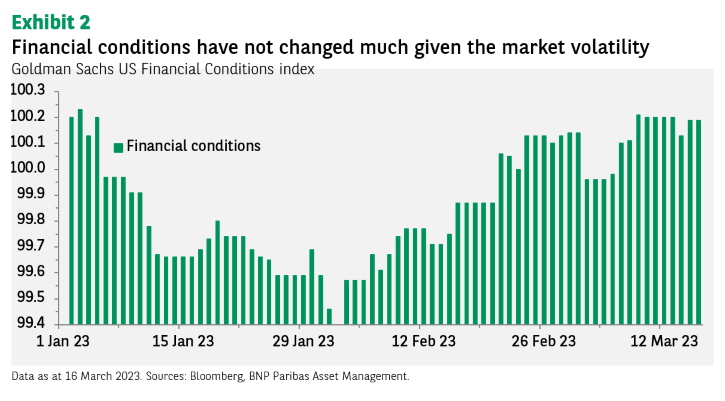

Measures of banking strength do not show reason for concern among market participants. The ‘TED Spread’ does not indicate a breakdown in confidence at present. It measures the gap between the rate at which banks lend to each other, typically represented by the difference between Libor (the London Interbank Offer Rate) and the equivalent Treasury bill yield. The higher the spread, the greater the level of wariness between banks.

ECB stays the course

As widely anticipated, the Governing Council raised the three key ECB interest rates by 50bp on 16 March. This was the third consecutive 50bp increase, after two 75bp steps, taking the deposit rate to 3%. It is now 350bp above the level at which it started this cycle of monetary tightening in mid-2022.

The latest policy measure underlines the ECB’s determination to ensure the timely return of inflation to its 2% medium-term target.

While acknowledging that the current high level of uncertainty reinforced the importance of a data-dependent approach to policy rate decisions, the ECB reiterated in its statement that monetary policy will be determined by its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission.

New ECB macroeconomic projections

The new forecasts were finalised in early March before the recent financial market tensions. The ECB noted that these tensions implied additional uncertainty around the baseline assessments of inflation and growth.

Prior to the latest developments, the ECB’s baseline path for headline inflation had already been revised down, mainly owing to a smaller contribution from energy prices than previously expected.

ECB staff now see headline inflation averaging 5.3% in 2023, 2.9% in 2024 and 2.1% in 2025. At the same time, the ECB sees underlying price pressures remaining strong. Inflation excluding energy and food continued to increase in February and ECB staff expect it to average 4.6% in 2023, (higher than foreseen in the December projections).

Subsequently, core inflation projected to come down to 2.5% in 2024 and 2.2% in 2025 as the price pressures from past supply shocks and the reopening of the economy fade and as tighter monetary policy increasingly damps demand.

Investment strategy

Our multi-asset team initiated an underweight in European sovereign bond duration when 10-year German Bunds broke though the lower bound of their recent range.

This was an entirely valuation-driven move, seeking to exploit what it sees as excessive swings in bond markets – for example, a 50-55bp drop in 10-year Bund and French government bond (OAT) yields.

This week having delivered ample evidence of the capacity of sentiment-driven markets to drive events, we cannot exclude further volatility. Central banks have, however, demonstrated their readiness to maintain financial stability. We expect them not to neglect this aspect of their mandates in their pursuit of price stability.

Disclaimer

![]()