US inflation

Inflation is popping up everywhere. Last Tuesday (13th July), the US printed an upside surprise for consumer price index (CPI) inflation for June 2021, coming in at a whopping 5.4%1, versus an expectation of 4.9%2. The following day (14th July), producer price inflation data for June came in at 7.3%3, versus an expectation of 6.7%4. Inflation, may not be as transitory as the market had expected. Core inflation, i.e. excluding food and energy prices, on both the consumer and producer measures also beat expectations. So there appears to be more than just the usual suspects of volatile energy and food price increases driving this trend. Most line items saw month-on-month increases. Some items provided ‘sticker-shock’: used car prices saw a 10.5% m-o-m (45.2% y-o-y) increase. Higher levels of inflation in the US will be tolerated relative to past regimes, as the Federal Reserve (Fed) last year adjusted its target to look at average inflation, not just point-in-time inflation. In short, it means the central bank will allow inflation to run hot to compensate for periods in which inflation was low.

Euro area inflation

Across the ocean, while most of the continent was awestruck by a beautiful football tournament, the monetary goalposts also shifted: the European Central Bank (ECB) revised its inflation target5. The ECB will now look at the 2% inflation benchmark in a symmetrical fashion rather than treat it as an upper limit. While the phraseology is subtle, in practice this could be meaningful, and brings the central bank in line with the Fed i.e. periods of below 2% inflation need to be compensated by periods of above 2% inflation.

Higher for longer

We expect inflation to remain higher for longer. While upside inflation prints may be giving fuel to the monetary hawks, rising Covid cases may deter the central bank from pressing the breaks prematurely. Even talking about pressing the breaks may become taboo in this heightened period of investor sensitivity to the Fed’s forward guidance. Federal Reserve Chairman Jerome Powell, in a testimony to the Senate Banking Committee said on Thursday 15th July, that while he is uncomfortable with inflation much higher than target, it would be a mistake to react too soon, citing pandemic-related bottlenecks as a cause for the inflation. He believes those bottle necks should pass. That underplays the demand driven increases we suspect are contributing to inflation, which are likely to be less transitory.

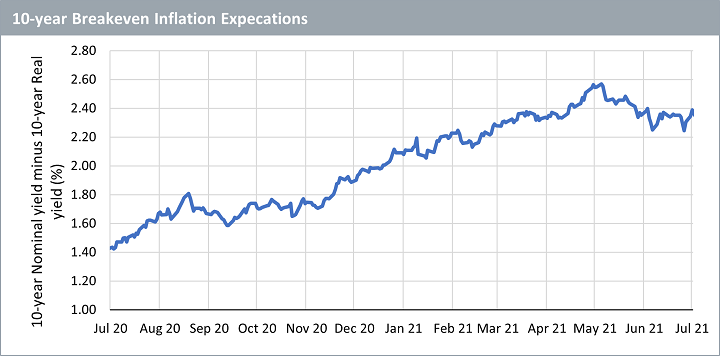

Expectations rise again

10-year breakevens (a proxy for inflation expectations) are rising once again, after looking like they had peaked in May 2021. Other measure of inflation expectations could regain upside pressure.

Source: WisdomTree, Bloomberg. 13/07/2020 to 13/07/2021

Historical performance is not an indication of future performance and any investments may go down in value.

Hedge with commodities

We believe broad commodities and gold are some of the best assets to hedge against inflation: “Positioning for inflation: commodities and gold can be essential hedging instruments”. The data printed last week emboldens our case for having these assets in a portfolio. As the elevated inflation numbers may not be transitory, this may not just be tactical but a strategic play.

Sources

1 https://www.bls.gov/news.release/cpi.nr0.htm

2 Bloomberg survey

3 https://www.bls.gov/ppi/

4 Bloomberg survey

5 https://www.ecb.europa.eu/press/pr/date/2021/html/ecb.pr210708~dc78cc4b0d.en.html