Inflation jumped to 9.2%1 in February (8.8% in January) – a surprise to most economists who were expecting it to start falling – showing that the beast hasn’t been tamed just yet. If inflation stays at this level then £100,000 of cash not generating any return will lose nearly a quarter of its value in just three years.

Hopefully that will not happen, but even though interest rates on savings are rising, the gap between what your bank or building society will pay you and inflation is still punitive for anyone sitting on a lot of cash.

Many investors are undecided about what action to take but know they have to do something. Equities are often said to offer long-term protection against inflation2, and one way they do that is through the dividend income they provide.

Some may worry that equity markets are fully valued after a decade of quantitative easing. They may be right, but if you are a long-term investor in a market going sideways, dividends can make a difference.

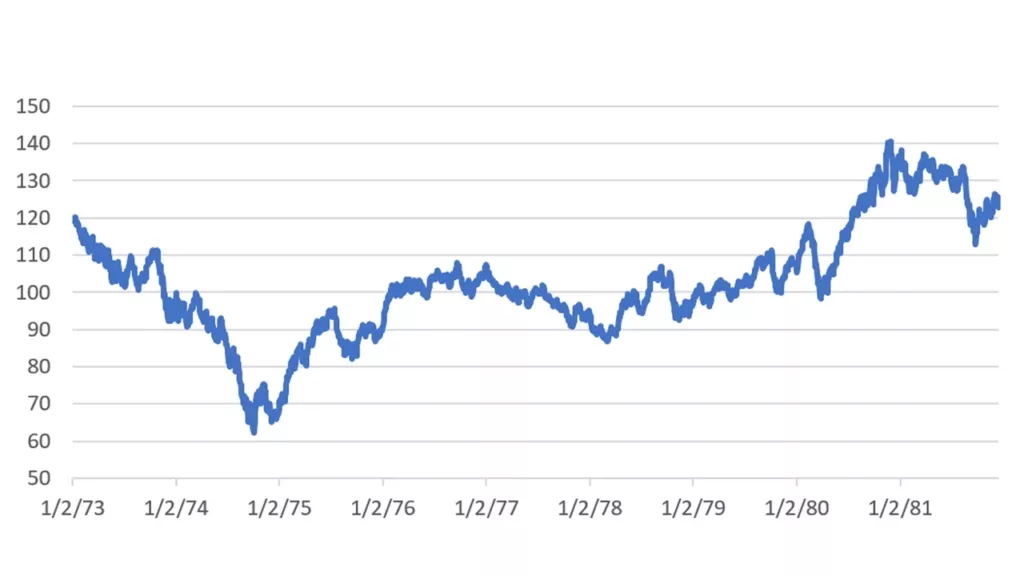

Take January 1973 to July 1980. The S&P 500 index staggered down from 120 in January 1973 to 62 in October 1974 before gradually clawing its way back up again in July 1980.

A market going nowhere?

What happens when you factor inflation into the numbers? The story is even bleaker. Adjust prices for double-digit inflation in the early part of this period3 and it was July 1987 before the S&P price recovered to the January 1973 level in real terms.

Yet the total return of the index with dividends reinvested over those 14 years was 381% – nearly 12% a year. Of course, to be fair, you need to factor inflation into those returns too. Adjusted for CPI, they look more modest – 4.18% a year in real terms – but still a lot better than the index charts alone might imply.

There have been other long periods spanning many years where markets have gone sideways – 1929 to 1956, for example, or 2000 to 2014. But, there have also been some spectacular climbs – between April 1982 and June 2000, for instance, the S&P 500 index rose nearly 650%.

There are important lessons in these numbers. You should not fear being in the markets if you are there for the long term. You do not know when they will turn – and when they do it can be sudden and sharp. Dividends count. They provide an important cushion in down markets and help you generate real returns in sideways markets. I believe they are likely to become a much bigger part of total shareholder returns in 2023 and the years ahead.

Historically, the UK was perhaps the best place in the world to find dividends. It still is a good source of income. But these days there are plenty of opportunities elsewhere for a global investor focused on decent dividends. That makes it easy to have a good diversified global portfolio with a strong focus on income.

To underline that point, as I write, the UK makes up just over 18% of our portfolio, Europe around 24%; North America 44% and we have around 15% in the Pacific Rim – ex Japan. Six of our biggest holdings are in the US, which most of us associate with low dividends.

Do not be lured onto the rocks by the siren call of a company with a very high dividend. It can be a sign of a company in trouble. Often the company has stretched financials which make paying the dividend an issue, or the business model is under long-term competitive threat. Good research is essential.

And do not be so focused on dividends that you miss out on fast growing companies that pay little or no dividend but are reinvesting profits wisely at high rates of return.

I like dividends, but only because of their contribution to the total return, and in generating a real return. Ultimately, my job is to grow and protect investors’ wealth. Dividends help do that.

Footnote

1 CPI inflation for 12 months to February 2023 – https://www.ons.gov.uk/economy/inflationandpriceindices

2 MSCI

4 Bloomberg

Investment risks

Unlike money deposited in a bank or building society account, an investment involves stock market risk. The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested.

When making an investment in an investment trust you are buying shares in a company that is listed on a stock exchange. The price of the shares will be determined by supply and demand. Consequently, the share price of an investment trust may be higher or lower than the underlying net asset value of the investments in its portfolio and there can be no certainty that there will be liquidity in the shares.

The use of borrowings may increase the volatility of the NAV and may reduce returns when asset values fall.

The Invesco Select Trust plc uses derivatives for efficient portfolio management which may result in increased volatility in the NAV. In addition, some companies are suspending, lowering or postponing their dividend payments, which may affect the income received by the product during this period and in the future.

The Invesco Select Trust plc – Global Equity Income Share Portfolio invests in emerging and developing markets, where difficulties in relation to market liquidity, dealing, settlement and custody problems could arise.

The Invesco Select Trust plc UK Equity Share Portfolio invests in smaller companies which may result in a higher level of risk than a product that invests in larger companies. Securities of smaller companies may be subject to abrupt price movements and may be less liquid, which may mean they are not easy to buy or sell.

Important information

This article is marketing material and is not intended as a recommendation to invest in any particular asset class, security or strategy. Regulatory requirements that require impartiality of investment/investment strategy recommendations are therefore not applicable nor are any prohibitions to trade before publication.

Where individuals or the business have expressed opinions, they are based on current market conditions, they may differ from those of other investment professionals and are subject to change without notice.

For more information on our products, please refer to the relevant Key Information Document (KID), Alternative Investment Fund Managers Directive document (AIFMD), and the latest Annual or Half-Yearly Financial Reports. This information is available using the contact details shown.

Further details of the Company’s Investment Policy and Risk and Investment Limits can be found in the Report of the Directors contained within the Company’s Annual Financial Report.

If investors are unsure if this product is suitable for them, they should seek advice from a financial adviser. For details of your nearest financial adviser, please contact IFA Promotion at www.unbiased.co.uk