Berlin’s 34‑point reform program could be a major success because it addresses a multitude of challenges. Patience might pay off for investors.

IN A NUTSHELL

- At the beginning of July the governing coalition surprised markets by announcing a comprehensive reform package.

- The package targets excessive bureaucracy, underinvestment and supply‑side constraints, and we consider the chances of implementation to be high.

- Combined with the government’s investment programs and the economic recovery that is already underway, it offers investors long‑term opportunities in both equities and infrastructure.

A surprisingly broad package of measures with long‑term potential for investors

The governing coalition presented an impressively broad reform package on July 2. Together with other measures that have already been approved or implemented, the package has the potential to deliver effects as lasting as those of “Agenda 2010,” Gerhard Schröder’s 2003 reform package. Against the backdrop of a strengthening economic environment, the timing of the package appears particularly favorable.

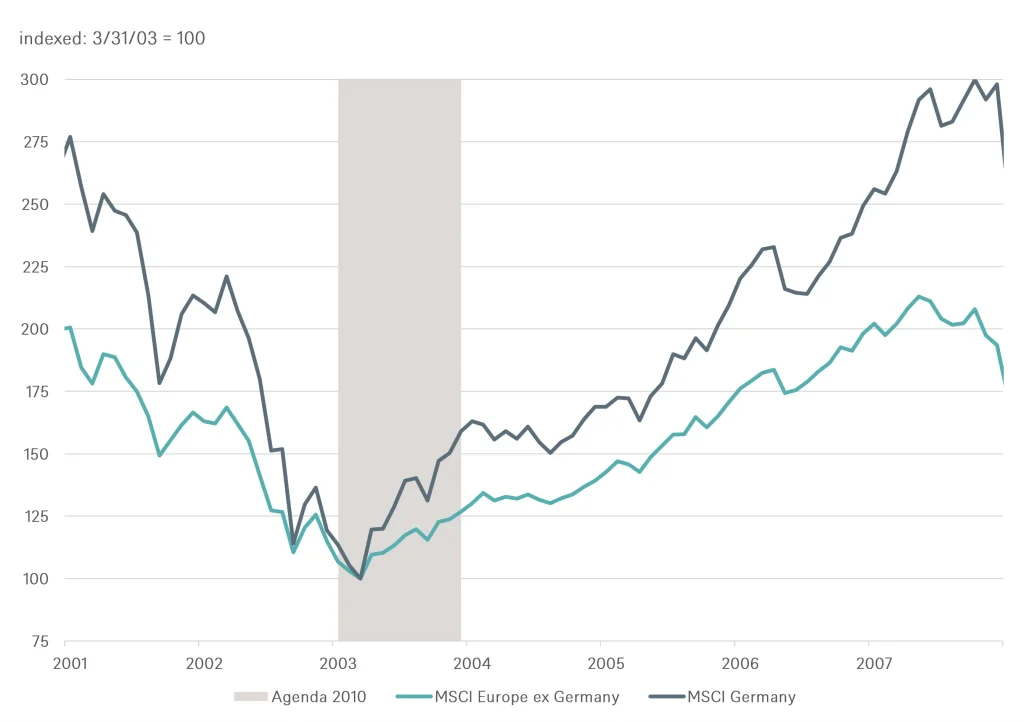

German equities have now outperformed their European peers for three consecutive days following the announcement of the Berlin coalition’s policy package on Thursday morning. We expect financial markets to continue rewarding progress as the reforms move through the legislative process. But reforms often take years to reveal their full impact on both the economy and financial markets. Figure 1 illustrates how German equities outperformed European stocks for years following the implementation of Agenda 2010, in particular in the first year after its adoption in 2003.

Fig. 1: Agenda 2010 was followed by years of outperformance in German equities

Of course, other factors, such as the cyclical nature of the German economy and the sharp increase in exports to China at the time also played an important role. In our view, however, the reforms enabled German companies to benefit more from the global upswing than they otherwise would have.

We expect a similar pattern this time. Despite widespread scepticism, the German economy was already on a promising path in 2025 but was held back by the Trump punitive tariffs and the consequences of this year’s Iran war. We now see the economy returning to an expansionary trajectory, as reflected, for example, in the strong industrial orders in May: up 1.9% month-on-month, and by 1.0% excluding large orders. The combination of structural reforms and an improving cyclical backdrop should provide a supportive environment for capital markets at a time when investors are increasingly looking for alternatives to the highly valued AI-related sectors concentrated in the U.S. and Asia.

1/ We actually like it: the package in context & detail

1.1 Various challenges – various solutions

Structural, historical and cyclical headwinds for Germany’s economy

Germany has long been burdened by three fundamentally different challenges that are often conflated in public debate. First, structural supply-side weaknesses, including a high tax and social contribution burden, excessive bureaucracy and rigid labor-market regulations. Second, after decades of underinvestment; in defense, energy infrastructure and housing construction, efforts are now being made to make up for prolonged periods of insufficient spending within a relatively short timeframe. Third, external cyclical headwinds, such as elevated energy prices resulting in part from two wars, weak demand for industrial goods amid the global manufacturing recession, U.S. tariffs and China’s transformation from customer to competitor. While structural weaknesses have often been blamed for all of Germany’s challenges, distinguishing between these different factors is important. And, in our view, the outlook is now improving on all three fronts.

Global economy back on a stable growth path

We believe the global industrial recession has passed its low point. There remains considerable pent-up demand for investment worldwide as several headwinds fade. U.S. tariffs are becoming less of a drag, and the economic consequences of the Iran war have proved far less severe than many feared. Oil prices have already fallen sharply from their recent highs. In Germany, industrial orders have increased strongly in recent months and we believe it is only a matter of time before this translates into higher industrial production.

Infrastructure: From neglect to a top priority

The governing parties had already addressed weak public investment in defense and infrastructure before taking office by easing Germany’s constitutional debt brake. As a result, German defense spending — most of which is no longer subject to the debt brake — is set to triple by 2028 compared with 2022. In addition, the federal government has launched the Infrastructure and Climate Neutrality Fund, a €500 billion investment program, equivalent to around 11% of gross domestic product (GDP), which will be rolled out over the next ten years.

At last, supply-side reforms

The newly adopted reform package — which we expect to be largely translated into legislation by year-end — is, in our view, as far-reaching and potentially growth-enhancing as the last major reform effort, the Agenda 2010 reforms introduced in 2003. Those reforms helped transform Germany from the “sick man of Europe” into Europe’s economic role model.

1.2 The Main Components of the new reform agenda

Streamlining Bureaucracy

- Abolition of all reporting and documentation requirements. Any requirements that remain must be justified and reapproved.

- Approval as the default: all applications will be considered approved if the relevant authority does not identify a need for further review within four months.

- If implemented as proposed, these two measures would represent a fundamental shift in Germany’s bureaucratic framework.

- A key test of the government’s determination to drive meaningful change is the planned repeal of the Supply Chain Act for around 95% of companies.

- The combination of deregulation and the digitalization of public administration is expected to go far enough to enable an 8% reduction in public-sector staffing.

- The Fourth Bureaucracy Reduction Act, which entered into force in October 2024, includes additional measures to accelerate planning and approval procedures, particularly for industrial facilities and infrastructure projects.

Labor-market reforms to increase flexibility and labor supply

- The recommendations of the Pension Commission are to be implemented in full. The statutory retirement age would be raised, although only from 2031 onward and by just six months spread over a decade. This is arguably too late and too gradual to offset the retirement of the baby-boomer generation, which is already underway. However, a range of measures is intended to postpone the effective retirement age, which could significantly expand labor supply. This is particularly relevant given the long-standing trend toward later retirement and steadily rising labor-force participation among older workers.

- The recommendations of the Welfare State Reform Commission are also set to be adopted. These would further strengthen work incentives for low-income earners, in addition to the already implemented replacement of the Bürgergeld scheme with a new system called basic income support.

- Expected measures to increase working-time flexibility have, however, been postponed until the autumn.

- The Skilled Immigration Act II, which entered into force earlier this year, is intended to further improve access to the German labor market. Additional measures include the introduction of the Opportunity Card 2.0, a digitalized points-based immigration system, and a faster recognition process for foreign professional qualifications through the centralization of responsible authorities.

Tax reform

- The proposals for personal income tax reform are relatively modest.

- We expect greater economic benefits from the already approved reduction of the corporate tax rate to 25%, although this will only take effect from 2028 and will be phased in gradually over a five-year period.

- Until then, companies can benefit from a 30% declining-balance special depreciation allowance for investments.

Ban on the nationalization of residential property

The measure is intended to prevent state-level nationalization of large private rental housing portfolios, thereby reducing a key political risk for real estate investors, although the legal path may prove complex given Germany’s division of powers between the federal and state governments.

Infrastructure measures

- Accelerated expansion of electricity distribution networks, with implementation times for new grid projects set to be cut in half.

- Faster rollout of the long-overdue digitalization of the electricity grid. By the end of 2030, 90% of metering points are supposed to be equipped with smart meters.

- Both measures are urgently needed to advance the energy transition.

Measures to strengthen capital markets

- As also recommended by the Pension Commission, both the first pillar (statutory public pension system) and the third pillar (private pension provision) of Germany’s pension system are expected to include elements of capital-funded retirement provision. If this succeeds in substantially increasing equity ownership in Germany, it could also be regarded as a supply-side reform, given the strong empirical evidence that deep capital markets support long-term economic growth.

- These measures would be complemented by the Startup Nation Act (adopted in February 2026), a package aimed at strengthening Germany as a venture-capital hub.

- Tax incentives for venture-capital investors are also planned.

1.3 A long road from proposal to legislation

For now, the proposed measures remain just that — proposals. They still need to be translated into legislation, coordinated across ministries, approved by the cabinet and passed by both the Bundestag and, in many cases, the Bundesrat, the upper house. That is a lengthy process involving many steps, all of which are expected to be completed by the end of the year. Most of the legislation is scheduled to enter into force on January 1, 2027. But a great deal could still go wrong along the way. Nevertheless, we see a number of reasons to believe that the proposed reforms have a strong chance of ultimately being implemented:

- The program is backed by the entire governing coalition, including the Christian Democratic Union (CDU), the Christian Social Union (CSU), and both wings of the Social Democratic Party (SPD).

- There is an overwhelming — if largely unspoken — consensus in Germany that change is needed. This view is shared by the partners in the governing coalition.

- That said, the reforms are likely to face opposition from a variety of interest groups. In principle, this should be seen as a positive sign, since the absence of protest would suggest that the measures lack significance. However, the proposed reforms are so numerous and affect such a broad range of stakeholders in different ways that, unlike during the adoption of Agenda 2010 in 2003, we believe it is quite possible that no single protest movement will emerge around which all opponents can rally.

If these measures are ultimately implemented, they will lay the foundation for a sustained improvement in Germany’s economic outlook. Though structural reforms do not, by themselves, generate an economic upswing, they create the conditions necessary for the economy to turn the next cyclical recovery into stronger and more durable growth.

2 / How could investors benefit?

2 / How could investors benefit?

2.1 German equities could regain momentum

Dax at record high, but still lagging other major indices this year

The presentation of the reform package on July 2 was followed that day by a new record high in the Dax. In a global context, this allowed German equities to recover at least some of the relative underperformance accumulated over the previous twelve months, particularly compared with the broader European market. This underperformance was largely driven by the above-average burden imposed on the German economy by the Trump tariffs and by the further increase in energy prices following the Iran war.

The strong performance of the major global technology stocks also played a role. But this segment is currently experiencing a period of heightened volatility. The AI boom initially claimed casualties among software companies and later among the hyperscalers that had been at the forefront of the AI theme. Semiconductor stocks, by contrast, delivered an exceptionally strong second quarter. In our view, however, valuations in the sector have now reached levels that leave it vulnerable even to relatively minor disappointments — such as less aggressive capital expenditure plans from the hyperscalers.

Against this backdrop, European and German equities could emerge as relative beneficiaries, as they are not among the pioneers in these highly valued segments. As Figure 2 shows, German and European equities continue to trade at a significant discount to U.S. equities, both by current and historical standards, although this discount has narrowed somewhat as a result of the recent sector rotation. In addition, Europe stands to benefit disproportionately from the reopening of the Strait of Hormuz, just as it had previously suffered disproportionately from constraints in energy supply. As such, the positive effects of renewed energy market normalization could prove particularly supportive for the European economy.

We do not believe that the reform package will ignite foreign investors’ interest in the German equity market as quickly as last year’s announcement of substantially higher defense and infrastructure spending. Rather, we expect it to be a classic “show-me” story — one in which investor confidence builds only as the reforms become visible.

In our view, the sectors most likely to benefit from the reform package are those with a strong domestic focus, including construction, real estate, retail, banking and business services. Within the equity market, small- and mid-cap stocks in particular stand to gain from the proposed reforms.

2.2 Fixed income and currencies

Modest impact expected on German Bunds and the euro

We expect the reform package to have only a limited impact on German government bonds over the medium term. Bond markets have already been pricing in a higher debt burden for the German state, while continuing to view Germany as one of the most creditworthy sovereign issuers in Europe. In our view, the reform package is unlikely to alter that assessment materially.

We also believe that the foreign-exchange market may react only gradually and with some hesitation. First, international investors are likely to remain sceptical about the pace at which the reforms can be implemented and may prefer to wait for tangible results before adjusting their expectations. Second, the euro’s performance is influenced by much more than Germany alone. At present, for example, political and economic developments in France continue to weigh on the common currency.

2.3 Alternative investments

Real estate affected on multiple fronts

Investors were probably encouraged most initially by Friedrich Merz’s statement that there would be no expropriation of residential housing companies. While Germany’s legal framework — or more precisely, the division of powers between the federal and state governments — could still create complications, the market initially interpreted this announcement as a positive policy signal. More significant from a structural perspective may be the plan to fully abolish the additional national capital buffer for residential mortgage lending from the beginning of 2027. Introduced only in 2022 and already reduced from 2% to 1% of loan volume in May 2025, its removal would free up additional financing capacity for new housing construction.

Further support for the real-estate sector, particularly for affordable housing, could come from the Germany Fund, which may also be used to finance new residential developments. More broadly, any measure that reduces supply-side constraints — such as bureaucracy, administrative requirements or lengthy approval procedures — should have a positive impact on a market characterized by a pronounced supply-demand imbalance.

In a section of the reform package announcement entitled “Growth and Fairness,” the coalition also pledges stronger support for future-oriented industries. These include the automotive sector, chemicals and pharmaceuticals, clean technology, the circular economy, mechanical engineering, battery-cell production, semiconductor manufacturing and the broader field of artificial intelligence. In our view, this could have positive spillover effects for commercial real estate — particularly office and logistics properties — in key economic hubs such as Munich and Southern Germany, Berlin, Hamburg and the Rhine-Ruhr region

3 / Conclusion: Germany as a Litmus Test for Europe’s Revival

The reform package alone will not fix Germany’s growth weakness overnight. However, together with higher investment, an improving industrial cycle and measures to address bureaucracy, labor shortages and supply-side constraints, it could lay the foundation for a noticeable improvement in growth prospects. For investors, the key may therefore be less any individual measure than the interplay between reform momentum, implementation and cyclical tailwinds.

Germany is Europe’s largest economy. If reforms can be implemented and investment set in motion there, the effects could spread positively across Europe as a whole. However, as many investors are likely to remain sceptical about Europe’s reform capacity and speed of implementation, we see the opportunities created by the reform package less in a short-term market reaction than in a gradual rebuilding of confidence. Visible progress on implementation, investment momentum and reducing bureaucracy should, over the medium term, help improve international investors’ perception of German and European assets.

In our view, the package is most likely to support German equities, especially domestically focused sectors such as construction, real estate, retail, banking and business services, with small and mid caps potentially benefiting most from reduced bureaucracy, stronger investment and an improving cyclical backdrop. For alternatives, real estate could benefit from lower political risk, additional financing capacity and support for affordable housing, while infrastructure-related assets may gain from higher public investment and faster approval processes. By contrast, the expected impact on Bunds and the euro looks more limited and gradual, as bond markets have already priced in higher public borrowing and currency investors may wait for visible evidence that reforms are being implemented.