The European Central Bank kept its main interest rate at 2% after Eurozone annual inflation eased to 1.7% in January from 2.0% the month before. The fall was chiefly driven by lower energy costs. The core price measure which excludes the costs of energy, food, alcohol and tobacco fell to 2.2% from 2.3%.

The Bank of England held rates at 3.75%, though four of its nine rate-setting policymakers voted for a 25bp cut. The BoE lowered its forecast for growth in the UK to 0.9% from 1.2% for 2026 and to 1.5% from 1.6% for 2027.

In contrast, the Reserve Bank of Australia raised rates by 25bp to 3.85%, marking its first hike in over two years. The RBA was the first G10 central bank to switch from easing rates to hiking them. It cited persistent inflationary pressure and a tight labour market.

Around the world: Volatile equities

Stock markets endured a bout of volatility last week as concerns over the impact of new artificial intelligence offerings on established players and plans for increased AI spending weighed on technology stocks.

Over the week to Thursday’s close, the tech-heavy Nasdaq index was down by 5%, while the broader MSCI World NR index fell by 2% (in US dollar terms; source: FactSet; data as of 5 February 2026).

Gold – often viewed as a ‘safe haven’ in periods of turbulence – saw its price fall before rebounding over renewed US-Iran tensions and weak US jobs data.

Elsewhere, the UK’s blue-chip FTSE 100 index hit a fresh high.

Figure in focus: 53.0

US business activity expanded in January with stronger output in both the manufacturing and services sectors. The composite Purchasing Managers’ index rose to 53.0 from 52.7 in December – a reading above 50 indicates expansion.

Business activity in Japan expanded at its quickest pace since May 2023 with the composite PMI rising to 53.1 from 51.1, boosted by higher factory production.

However, Eurozone business activity slowed to a four-month low. The bloc’s composite PMI index eased to 51.3 from 51.5 as new orders rose only slightly and the job market stagnated.

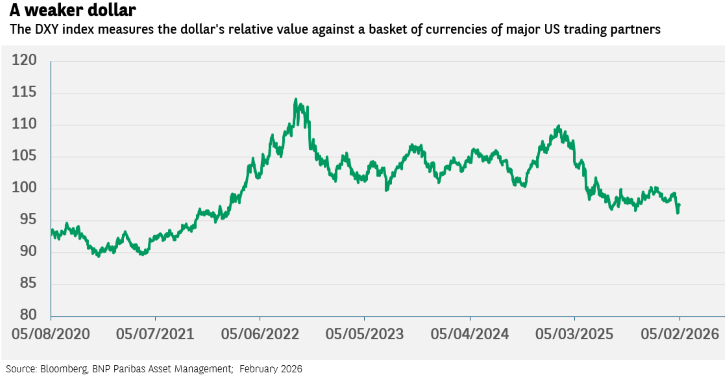

Chart of the week: A falling dollar

The US Dollar index plots the greenback’s value against a range of currencies of US trade partners. The DXY falls when the dollar weakens (i.e., loses value) versus the other currencies. It has fallen by over 10% in the 12 months through January.

Investors have been diversifying away from the dollar partly due to concern over the US government’s economic policies, but also to take advantage of opportunities outside of the world’s largest economy and further diversify balanced portfolios.

Words of wisdom: Project Vault

A new US government initiative to create a reserve of critical minerals to protect manufacturers from supply shocks and support US production.

The project will initially be funded by the US Export-Import Bank – the country’s official export credit agency. It will provide a $10bn loan, while a further $2bn will come from private capital.

The stockpile would include rare earths, copper and lithium as part of an effort to reduce the US’s dependence on China, which dominates the supply chain of many critical minerals.

Last week, the US, European Union and Japan announced they intended to work together to make their critical minerals supply chains more resilient.

What’s coming up?

- On Wednesday, China issues its latest inflation data; the US publishes a delayed update on job numbers.

- Thursday sees the UK report a preliminary estimate for fourth-quarter GDP growth

- The Eurozone follows on Friday with a second estimate of Q4 GDP. The previous estimate found the economy expanded by 0.3% in Q4, matching Q3’s growth rate.

- On Friday also, the US publishes its January inflation rate. In December, US annual consumer price inflation rose by 2.7%, matching November’s rate.