Equity income funds have historically been a staple of many long-term savings portfolios. But their appeal has waned in recent years, with some wealth managers believing that selecting shares from a pool of dividend-paying companies – often from out-of-favour sectors – is a bit outdated, unfashionable even.

To be fair, the equity income sector has none of the excitement of investing in high-growth sectors like technology and returns have lagged the more growth-focused indices over the past decade.

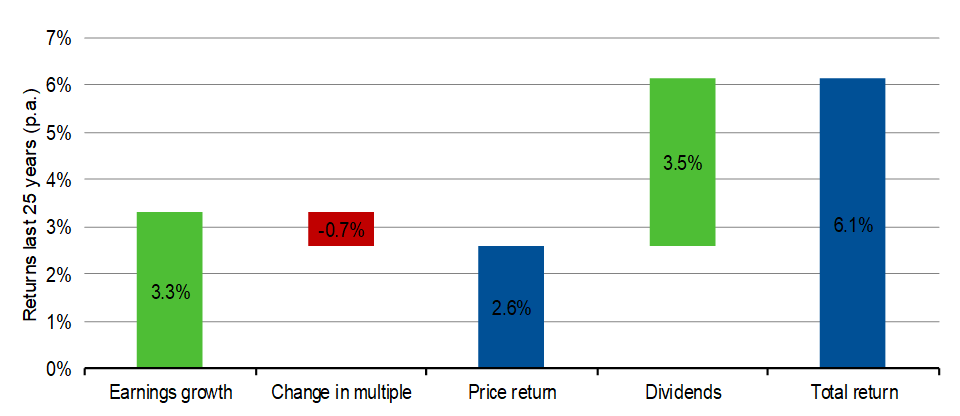

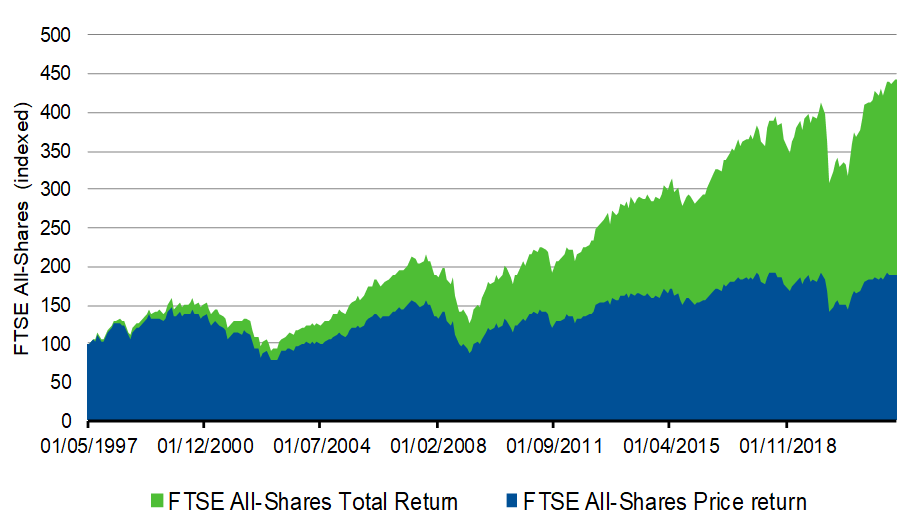

But dividends should not be discounted as a valuable source of returns; over the last 25 years they have accounted for over half of the FTSE All-Share Index’s total return of 6.1% per annum. And the picture is similar over 10 years where the All-Share Index delivered 7.2% a year, of which 3.8% was generated by dividends.1

Spoilt for choice or Hobson’s choice?

We believe successful equity income investing is about seeking out robust businesses with strong barriers to entry, which generate cash – and preferably oodles of it. Why start with cash-generative companies rather than high dividend payers? Because any dividends should be paid out of the cash a company generates, and the more cash generated the better, as this gives a firm more options. There are in essence three options at a company board’s disposal – reinvest the cash flows into the company; pay down debt; and/or distribute dividends.

Some firms will do all three in one year. But a company with lot of cash and a management team in a hurry to spend it can be more of a curse on shareholders than a boon. Take Marconi’s dash into telecommunications equipment during the dotcom bubble, following the sale of its defence arm. 2 Its big cash pile disintegrated very quickly. Suffice to say, cash needs to be invested wisely.

But the reverse is also true. The less cash generated by a company, the fewer the options it has, while generating little or no cash over sustained periods often leaves a firm with Hobson’s choice, i.e. none whatsoever.

Fundamentally, the optimal outcome is finding companies which generate enough cash to grow and pay dividends. Maintaining a corporation’s health should be the main priority for all long-term investors, whether income or growth orientated. Companies should be encouraged to constantly reinvest, refresh capital assets and spend on technology upgrades to allow them to compete both now and in the future.

Investor bias

Often, the essence of a growth investor’s arguments is that assuming a company can generate a superior return on capital, then it should reinvest all the cash it generates into the business. However, the key word is ‘assuming’. Capital in the growthier parts of the stock market has been free flowing in the last 10 years given the backdrop of record low interest rates (which lower the opportunity cost of investment) and buoyed by the returns generated by some well-known technology stocks. But there could also be a risk that too much capital has flowed into these areas, depressing future returns.

Investors have inbuilt biases and there is nothing like a new story to get the investing juices flowing, often leaving rationality at the door. Much as we try and rid ourselves of these biases they keep cropping up and consign investors to making sub-optimal decisions. Leuthold Group estimated in March 2021 that over 200 of the 1,500 NASDAQ Index constituents had not been profitable in any of the prior three years yet had a combined capitalisation of $2.3trn.3 That’s a lot of capital tied up in loss-making companies. Conversely, investing in dividend-paying companies, with their typically lower valuations, can provide diversification for investors, offsetting their holdings in growth companies.

Each to their own

Investors often ask what an acceptable dividend payout ratio for a company is – the ratio of what is paid out in dividends compared to the firm’s earnings. Essentially, they are asking how much of its earnings should a company retain for growth and how much should be paid out to investors. Personally, I do not think there is a set formula which applies to all companies when it comes to payout ratios. Much depends on the industry in which it operates and its capital structure. Does the company require large one-off investments to grow? Or can marginal capacity be added each year? Does demand and hence cashflow fluctuate a lot? We believe dividend payments should be not too little and not too much.

Compare for example an oil company and an insurer. An oil company’s overall production volumes will remain relatively stable until new fields are discovered and brought online. Developing a new oil field involves capital expenditure…and lots of it. On the other hand, those firms whose financial structure or business model requires little capital for growth – such as an insurer – lend themselves very well to income investing. They can pay out most of the post-tax cashflow as dividends.

Take Admiral Insurance, which has grown its customer base from 1.1 million policyholders in 2005 to 8.4 million by the end of 2021, up a remarkable seven and a half times.4 Admiral was one of the first insurers to really embrace the internet, even starting its own comparison site confused.com and branching into new products such as multi-car policies.

Its innovation also extended to its financing. Through reinsurance and co-insurance relationships with third-party insurers, Admiral hasn’t had to retain huge amounts of capital to finance its growth. It effectively utilises the balance sheets of its partners to do most of the underwriting and earns a commission. Its partners benefit from diversification credits on their solvency capital and earn a profit stream from the underwriting. So, unlike an oil company where the growth is dependent on intermittent but sizeable capital expenditure, Admiral has been able to grow strongly without onerous capital requirements. Admiral’s earnings have increased over five times in the last 15 years while the dividend payout ratio has exceeded 90% in every one of those years.5 This combination of income and growth is what can make income investing a powerful, long-term compounding strategy.

Bite the bullet

Management teams and investors need to be realistic though. Consumer tastes change, regulations get tougher and the competitive environment may deteriorate due to an influx of start-ups with cash to burn. There is no point paying an unchanged dividend while hoping things will improve. Where excessive cashflow is being paid out as dividends, investors should be prepared to forego some of this income.

It may seem strange, but we have advocated for certain companies to cut their dividends to allow greater reinvestment into the business. GlaxoSmithKline has laboured under an unchanged dividend since 2014. We believe the board’s decision to cut the dividend this year is in the best interests of the company as it splits into a global specialist pharma company and a global consumer healthcare company (Haleon) later this year.6 The reduced cash demands from the dividend will give both companies more financial flexibility to execute their growth plans – better to have a lower dividend today from a business with a brighter future, than bleed the company into administration.

Sage is another example of a company that has taken the decision to reinvest a greater proportion of its free cashflow to accelerate the technology transition of its accounting software from on premises to in the cloud. The decision appears to be bearing fruit. Investment in cloud-enabled products and increased marketing has generated positive feedback from implementation partners, independent consulting firms and most importantly strong customer uptake. This investment necessitated cuts to group earnings when first announced in 2019 and while the dividend has not been cut, we do expect dividend growth to lag earnings growth over the next few years.

ESG and income: Two sides of the same coin

As custodians of our investors’ capital, the asset management industry is key to promoting change especially on environmental, social and governance (ESG) issues. It has long championed governance issues, but there is a realisation that more needs to be done on social and environmental challenges. The industry is increasingly taking management teams to task where it feels companies are falling short of best practice. Income investing has a prominent role to play given much of the sector’s assets tend to be focused on cash generative, dividend-paying companies which are often in some of the more established industries. However, there is a growing realisation that investors need to be pragmatic as well as principled.

The Ukraine crisis has brought this issue into the spotlight. Western European governments are desperately trying to wean themselves off Russian gas, while ensuring there is adequate electricity generation to keep economies moving. Society must encourage the development of renewable energy sources and the adoption of electric vehicles, but any holistic solution needs to include the oil and gas industry. We cannot turn off fossil fuel with the flick of a switch.

As well as reducing emissions such as carbon dioxide and methane associated with the production of oil and gas such as leaks, we need to reduce the emissions as the oil and gas is used. This will involve investment into carbon capture and storage systems. These systems capture carbon dioxide emissions at source, such as in power stations, as the gas or oil is burned to heat boilers, then purify and compress the gas. The gas is then injected into impermeable rock formations underground to trap it there. The infrastructure spend needed to facilitate such a network will be huge. We cannot rely solely on governments to sponsor this development; it will need the oil and gas industry to play its part.

As Dr Myles Allen, one of the authors of the UN Intergovernmental Panel on Climate Change (IPCC) for its 3rd, 4th and 5th Assessments said: “If you work or invest in the fossil fuel industry, don’t walk away from the problem by selling off your fossil fuel assets to someone else who cares less than you do. You own this problem, you need to fix it. Decarbonising your portfolio helps no-one but your conscience. You must decarbonise your product”.7

Our role as income investors is to encourage our holdings to improve their sustainability. The world will benefit from new technology, but the battle against climate change needs established companies and their shareholders to play their part.

Reports of equity income’s death are greatly exaggerated

Equity income investing may be going through a lull, but it is far too early to write it off. I firmly believe it brings good disciplines which could generate long-term rewards to the patient investor. Dividends have accounted for over 50% of the return from the FTSE All-Share Index over the last 10 and 25 years. The flow of capital out of the some less fashionable sectors over the last five years has left valuations at attractive levels, both in absolute terms and relative to supercharged growth companies. Furthermore, income investors have a role to play in driving the sustainability agenda of our investments.

[2] Marconi catches the telecoms cold | Business | The Guardian

[3] Leuthold Group, March 2021

[4] Admiral Group annual report 2021

[5] Admiral Group annual report

[6] GSK slashes dividend as it outlines growth prospects – Investors’ Chronicle (investorschronicle.co.uk)

[7] Myles Allen: Fossil fuel companies know how to stop global warming. Why don’t they? | TED Talk