The confluence of risks alongside the reopening boost, China’s stimulus measures and peaking inflation imply that a wide range of outcomes is possible. Bill Maldonado, Eastspring Investments’ Chief Investment Officer believes that investment playbooks need to challenge the status quo to help investors stay nimble and seize the opportunities that arise.

Macro: Economic reopenings to help support global growth despite tightening liquidity and supply shocks.

1. What is your outlook for the global economy and are central banks at risk of tightening into a recession?

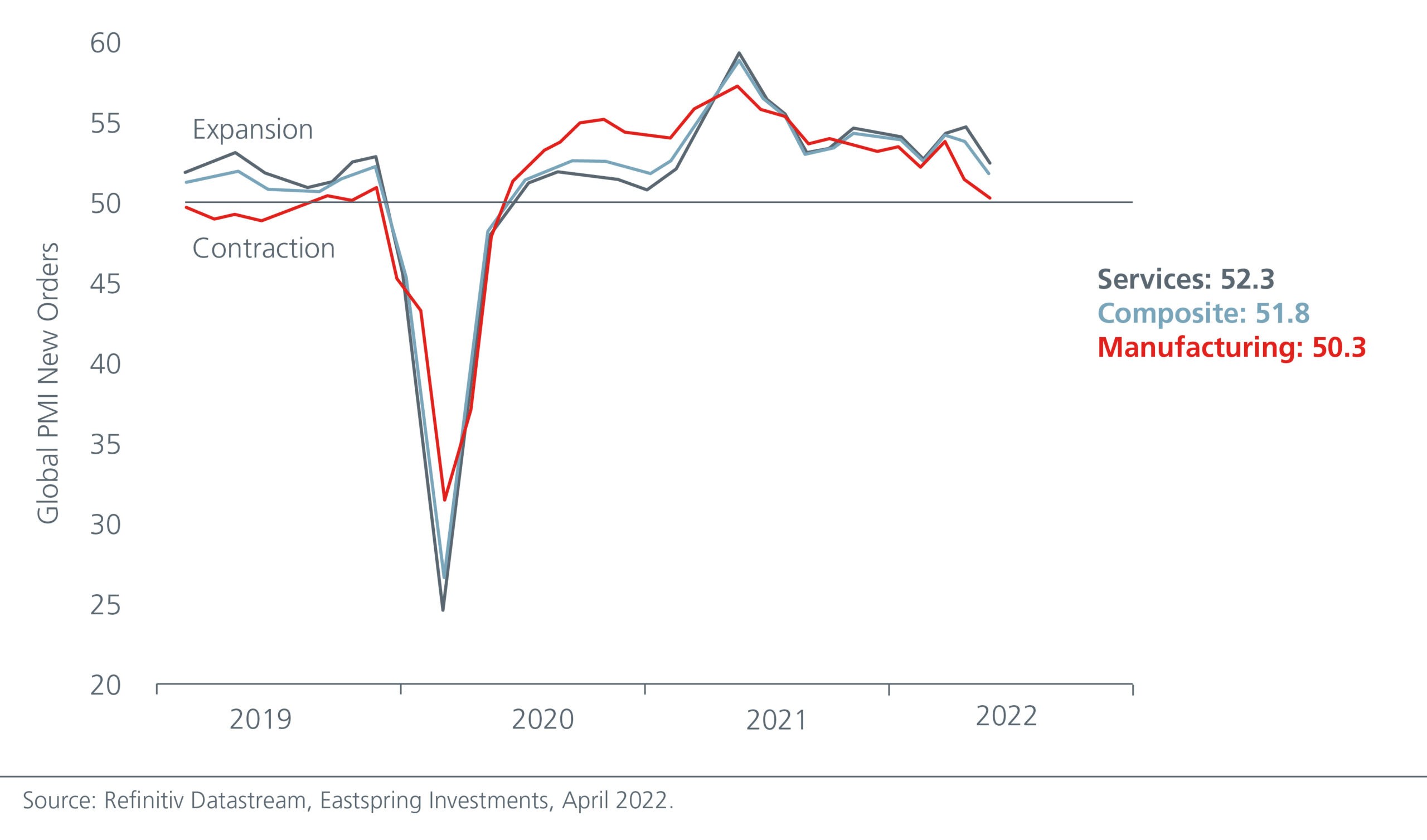

Global growth conditions will continue to be challenged by a confluence of existing headwinds (e.g. Russia-Ukraine crisis, hawkish central banks, rising yields, supply shocks), in addition to China’s zero COVID policy. Fig. 1.

Fig. 1. Global growth is slowing from 2021’s peak

In the US, we believe that the consumer outlook is mixed as actual data indicate that consumer spending is seemingly resilient (e.g. pent-up demand, USD2.3 trillion of excess savings, decreasing household debt-to-disposable income), however surveys are signalling a deteriorating outlook. We note that giant US retailers Target and Walmart recently missed their quarterly earnings estimates. Meanwhile, Europe is hit hardest by the supply disruptions stemming from the Russia-Ukraine crisis and as such faces higher risk of stagflation in the near term.

We believe that developed market economies, largely the US, are still transitioning to a ‘late business cycle’, and thus it may be too early to call for a recession. The US Federal Reserve (“Fed”) is prioritising its fight against inflation over boosting near-term growth. There is a risk that it may hike rates into a growth restrictive territory and tip the US economy into a recession. The outlook for the emerging market (“EM”) economies is more mixed. While EM Asia anchors on China’s growth trajectory, other EMs face imported inflation, due to a stronger US dollar and supply disruptions.

On balance, economic reopenings post COVID should be supportive of global growth, but tightening financial conditions alongside hawkish central banks, imply a wide range of outcomes. We are monitoring recession risks and will stay nimble to navigate the uncertainty and volatility.

2. How would the Asian economies fare against this backdrop?

With the decline in COVID restrictions globally, consumption is likely to continue to shift from goods to services. As such, Asian economies with large domestic populations are expected to fare quite well. The ASEAN economies should benefit from the reopening boost; this should be especially positive for Thailand whose economy is highly reliant on tourism. Commodity-based economies like Malaysia and Indonesia should also see good GDP growth in 2022.

At the same time, higher commodity prices from supply chain disruptions, rising energy prices and reopening pressures have lifted inflation across Asia. Asian central banks have largely been slower to hike rates relative to their developed market counterparts, although the pace appears to be picking up. That said, they may be less aggressive given that higher food and energy prices, which are key inflation drivers in the region, will impact disposable income. With Asian governments’ greater fiscal flexibility, they are more likely to rely on subsidies to mitigate food and energy inflation shocks.

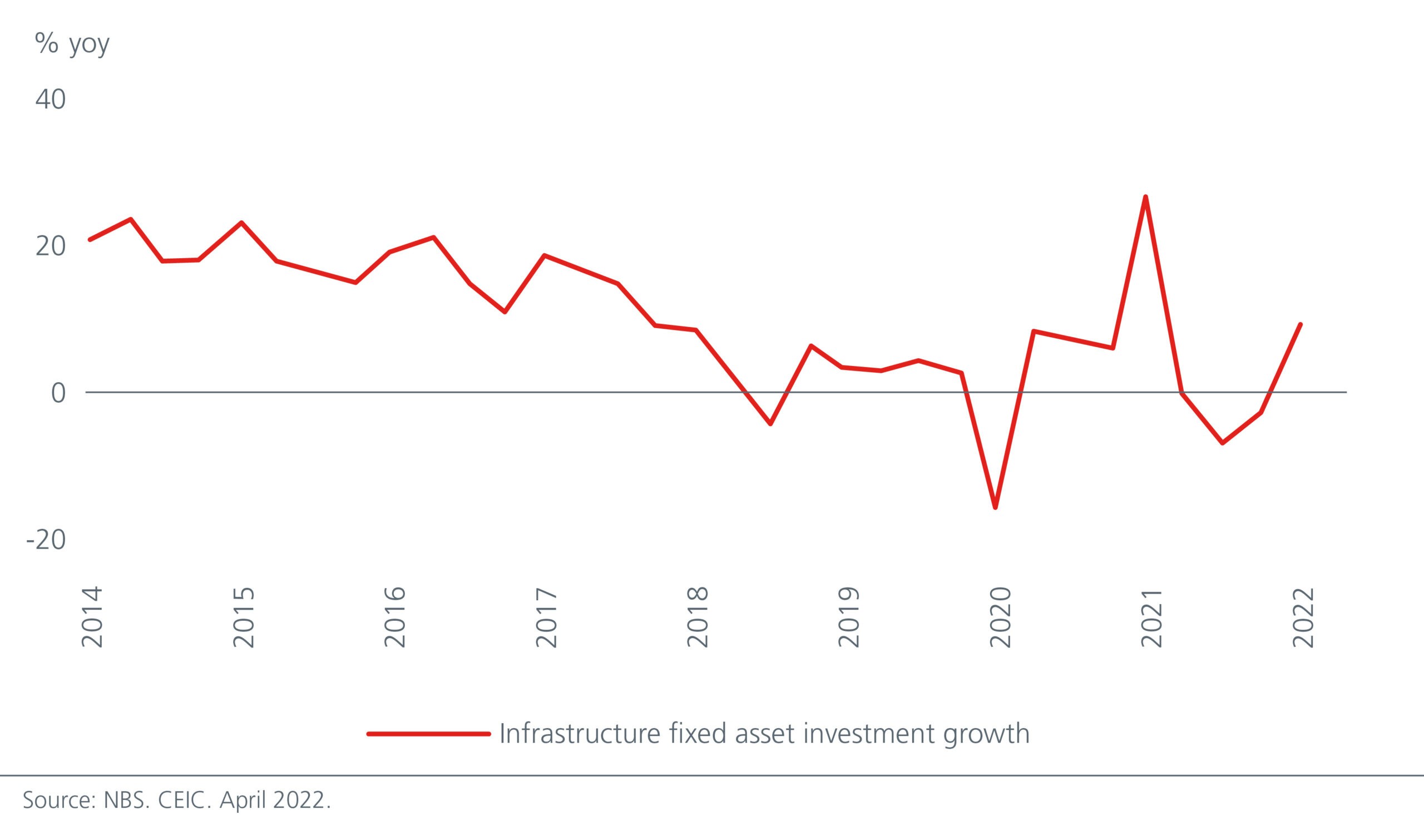

China’s economic woes are well telegraphed, and investors are mostly bearish on the economy. On a positive note, the learnings from the Shanghai lockdown could tweak China’s zero COVID policy and make implementation more pragmatic going forward. Investors therefore may not want to extrapolate the events in Shanghai to the rest of China. Meanwhile, greater fiscal support is forthcoming via tax cuts. Infrastructure investment is also expected to be an important growth driver. Fig. 2. The People’s Bank of China has been cutting the reserve requirement ratio, loan prime and mortgage rates. While we may have seen the worst for China’s economy in the second quarter of 2022, it would take time for these counter cyclical measures to be reflected in the real economy.

Fig. 2. Infrastructure investment is expected to be a strong growth driver for China

Asset allocation: The recent selloffs do not weaken the case for a traditional 60/40 portfolio.

3. Bonds and equities have both sold off in the first half of 2022. Does this weaken the case for a traditional 60/40 portfolio?

Historically, the correlation between bonds and equities is mostly negative (and hence provides the most diversification benefits) when valuations for both asset classes are not expensive. 2022 was unique in that both asset classes traded at relatively lofty valuations post-COVID, and we saw both asset classes experience large drawdowns recently.

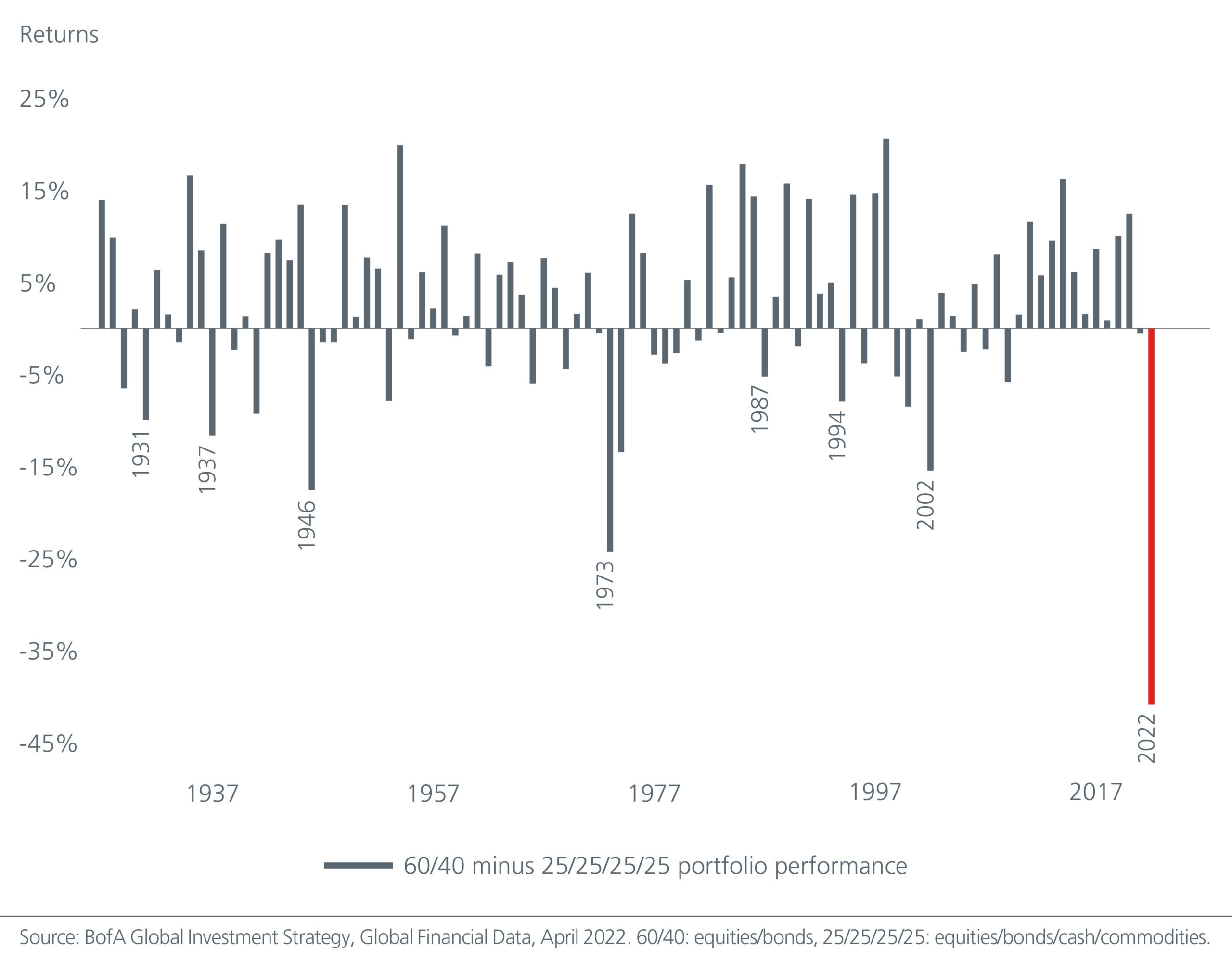

Time horizon is an important aspect when considering the case for a traditional 60/40 portfolio. Strategic asset allocation has shown to be the most significant contributor in meeting a portfolio’s return objective over the longer term (five to ten years). Hence, the recent selloffs do not on its own weaken the case for a 60/40 portfolio. Fig. 3.

Fig. 3. The 60/40 portfolio has consistently delivered over the longer term

Valuations for both equities and bonds have improved dramatically since the start of the year. We think the potential peak in inflation this year implies that the 60/40 strategy could resume its strong performance over the coming decades. At the same time, tactical asset allocation from asset pairs and equity risk premia from factors (Value, Momentum, Quality etc) provide uncorrelated alpha streams which can help mitigate potential drawdowns.

We believe broad diversification and liquidity are key considerations in a slowing growth and rising inflationary environment. Our multi asset team has implemented a number of medium-term tactical asset allocation investment ideas which are expected to add value over a three-to-twelve-month time horizon.

During times of high market volatility and high inflation, real assets, such as gold, are attractive havens. The team is constructive on US gold miners as a key source of diversification and inflation hedge. Historically gold miners tend to outperform US equities in a rate hike cycle. The team is also long global airlines as easing travel restrictions will see a steady recovery of the industry’s capacity and efficiency.

Equities and bonds: We favour low volatility, value and dividend paying stocks while peaking inflation presents opportunities to buy longer duration bonds.

4. Can the year-to-date outperformance in value stocks continue?

The change in expectations around inflation and interest rates is refocusing the market’s attention towards profitability and free cashflows. This is likely to continue to favour value stocks. Decarbonisation will also require massive infrastructure and capital expenditure over the next decade, which should benefit value sectors such as industrials and materials.

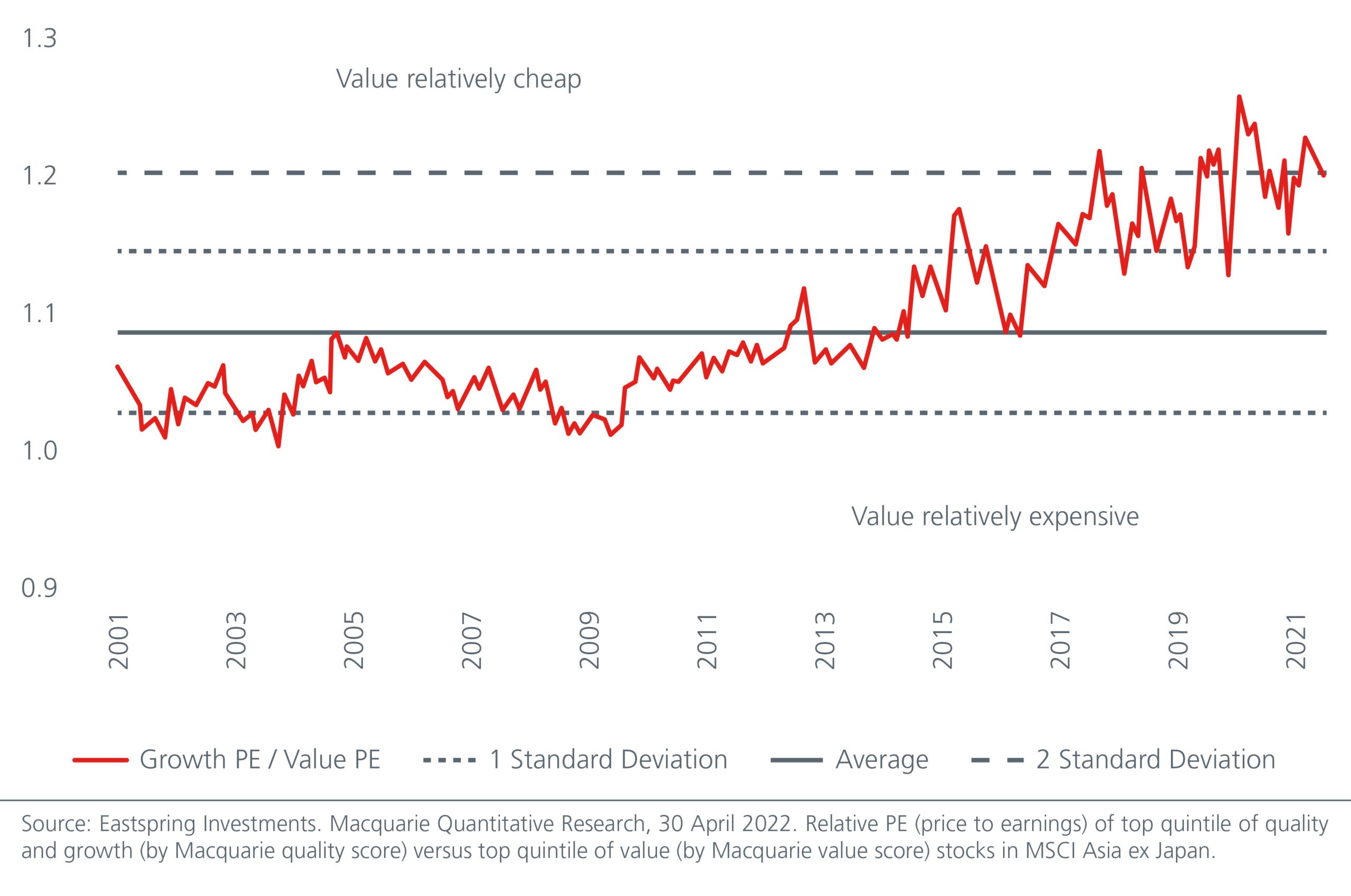

Rate hikes are also bringing back a focus on valuations. Given investor exuberance over growth stocks in the past decade, the valuation dispersion between value and growth stocks in Asia remains large even though value has started to outperform since November 2020. This suggests that there can be further upside to value stocks in Asia. Fig. 4.

Fig. 4. Value stocks are at a huge discount to growth stocks in Asia

The same thesis applies to the Global Emerging Markets and Japan where the valuation dispersion between growth and value stocks are still at extremes. Given the growth focus of many investors in the last decade, value stocks potentially offer alpha and diversification benefits to portfolios.

5. How can investors weather the more frequent equity market swings?

Low volatility equity strategies can help investors ride through choppy markets. This is especially so for Asian equity markets which are historically more volatile than developed markets and take longer to recover from market drawdowns. Low volatility stocks fall less during market declines, minimising the risk that investors exit the market at the wrong time. A portfolio of low volatility stocks generally represents firms with sounder leverage levels and have more stable and proven business models. As these stocks fall less in a bearish market, they only need to rise by a smaller magnitude to recover. This effect, when compounded over time, can potentially lead to superior long-term returns for investors.

Income from equities can also help add resilience to portfolios. Dividend paying companies are a buffer during volatile markets, providing a more consistent return of capital given their strong cash-flow generating ability. Dividend income is a long-term driver of Asia’s equity returns, accounting for 25% of total annual returns over the last 20 years1. In addition, Asia appears well suited for an income strategy as the number of stocks in Asia Pacific ex Japan that have dividend yields above 3% is almost twice that of Europe and more than three times that of the US2. A careful selection of good quality dividend paying stocks provides a stable income stream to investors.

6. Given the rise in bond yields, are there still opportunities within fixed income?

Higher inflation expectations and a hawkish Fed stance drove the 10-year US Treasury yield above the psychological 3% level in May, the first time since 2018.

While the 10-year yield has retraced slightly since, and may increase from here, we think the rise will be more orderly as US core inflation may start to moderate in the second half of 2022. If growth concerns cause inflationary pressures and rate hike expectations to fall, the 10-year yield trajectory may be lower from here.

We are slightly more bullish on US duration as valuations are starting to look more attractive relative to the start of the year. US investment grade credits are also starting to look more attractive due to the higher yields and spreads. Compared to Europe, they are less exposed to the Russia-Ukraine crisis and have better ability to service debt. Meanwhile after a rough start, US high yield credits stand to potentially benefit later in the year as long as the US economic outlook remains supportive.

We also find value in Asian bonds. Most 10-year local currency Asian bond yields are close to their 5-year highs and have crossed peaks seen during the 2018 Fed hiking cycle. Fig. 5. Meanwhile, the steepness across most Asian yield curves relative to their historical averages suggests that it makes sense for investors to add longer duration bonds. If risk sentiment improves, which we expect, we would likely see returns enhanced by the higher yields and more attractive credit spreads.

Fig. 5. Most Asian local currency 10-year yields are close to their 5-year highs

7. What is the outlook for China equities and Asian high yield bonds?

A variety of high frequency indicators, notably reported cases of infections and traffic congestion data, show that the COVID situation in China is improving at the point of writing. Pent up demand from easing lockdowns will boost domestic consumption. It could also lift China’s battered real estate sector as increased home viewings result in higher property sales. To achieve the government’s 2022 GDP growth target, however, we expect more aggressive fiscal and monetary policies in the second half of 2022. This would be positive for the China A-share market.

Within the Asian high yield bond market, we see selected value opportunities in India renewables. However, the outlook for China’s property sector is less clear. On a brighter note, the People’s Bank of China has been encouraging high-quality China property developers to acquire projects owned by the distressed developers, which can help to lower the sector’s default risk. We expect more support measures such as a relaxation of pre-sales proceeds by local governments, and further easing in mortgage and home purchase restrictions in Tier 1 cities.

Currencies: Further gains in the US dollar may be limited while the Chinese Renminbi should be more stable in 2H 2022.

8. What is the outlook for the US dollar and Asian currencies?

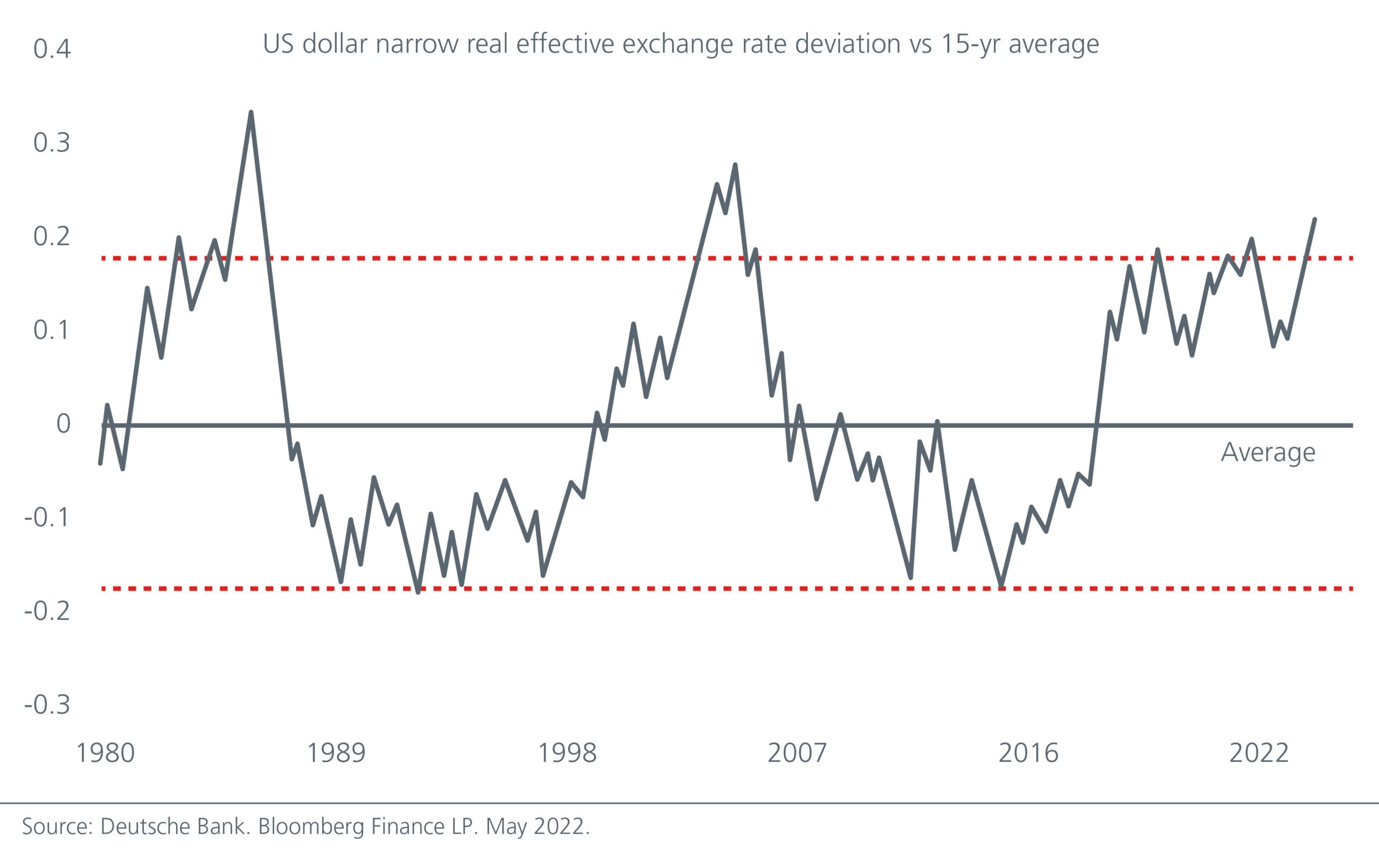

Widening interest rate differentials on the back of a hawkish Fed, relative to other central banks, and safe haven demand have supported the US dollar to date. Continued expectations of aggressive Fed rate hikes are needed to maintain the dollar’s strength. Should the Fed dial down its hawkish rhetoric, lower rate expectations could limit the dollar’s further upside.

Other factors may also cap the US dollar’s strength. Valuations appear stretched and institutional investors are also largely long the US dollar, potentially limiting further upside from additional increases in positioning. Fig. 6.

Fig. 6. The US dollar appears overvalued

On the Japanese Yen, we expect the currency to remain weak as long as the Bank of Japan maintains its ultra-dovish stance and the Fed continues to hike rates. Higher energy import prices will also likely continue to weigh on the Yen given that Japan heavily relies on natural gas imports.

Consistent with a supportive economic policy, the Chinese authorities are likely to desire a more stable Renminbi as well. This should act as an anchor for Asian currencies in the second half of 2022. Moreover, given Asia’s high levels of foreign exchange reserves, we believe that the region’s central banks would be able to intervene to prevent excessive currency weakness. We like the Singapore dollar given the Monetary Authority of Singapore’s currency appreciation policy. We also favour the Malaysian Ringgit and Indonesian Rupiah for their favourable terms-of-trade from higher commodity prices.

ESG: As decarbonisation gains momentum, Asia’s sustainable bond market will present increasing opportunities.

9. What are some of the key ESG considerations and opportunities for investors?

As decarbonisation gains importance in driving investment decisions, investors should be aware of the data quality and gaps. Carbon emissions can be classified into Scopes 1, 2 and 3. Scope 1 refers to direct emissions produced by a company while Scope 2 is the emissions produced by electricity generated or purchased by the company. Scope 3 refers to emissions that are in the company’s value chain and can be split into upstream (suppliers) and downstream (customers). According to the Greenhouse Gas Protocol, most emissions come from Scope 3. Yet it is sparsely reported as it is the hardest to measure. It is therefore important to understand these risks when making decisions based on carbon targets.

We believe there is no single approach to ESG or sustainable investing and do not avoid investing in a company simply because it has a poor ESG risk profile. We may still consider investing if we believe we can improve the company’s sustainability practices through active engagement with the management and the board.

Meanwhile, massive funding is required to combat the significant climate challenges confronting Asia. A large part of the financing will come from Asia’s bond markets, in the form of sustainable and green bond issuances, presenting investors with even more opportunities.

Risks: Rising geopolitical tensions, more supply shocks, and policy errors are on our risk radar.

10. What are the key risks facing investors in the next 6 to 12 months?

Geopolitical tensions remain an on-going source of market volatility. Equally, global growth could continue to be impacted by supply chain disruptions, higher inflation, and rate hikes. While we are cognisant of these risks, we caution against excessive investor bearishness. We do not expect global growth to fall off a cliff due to the waning impact of the Omicron variant, robust US labour market, generally healthy US corporate fundamentals, and increasingly attractive equity market valuations.

Separately, policy error is a key risk, be it excessive rate hikes or China’s zero COVID strategy. While policymakers in the past may have dealt with these risks separately, it is the confluence of these risks which is unprecedented. This means that policymakers have no similar experience to rely on.

Given the range of potential outcomes, we will continue to diversify our portfolios and have different playbooks to remain nimble.