Following the outperformance of Latin American stocks in 2023, the outlook for next year looks more challenging. Slow economic growth and fiscal deficits will dominate the agenda again. In this Macro Flash Note, Economist Joaquin Thul looks at the outlook for Brazil and Mexico for 2024 and how despite some domestic challenges, it remains positive for equities in Latin America.

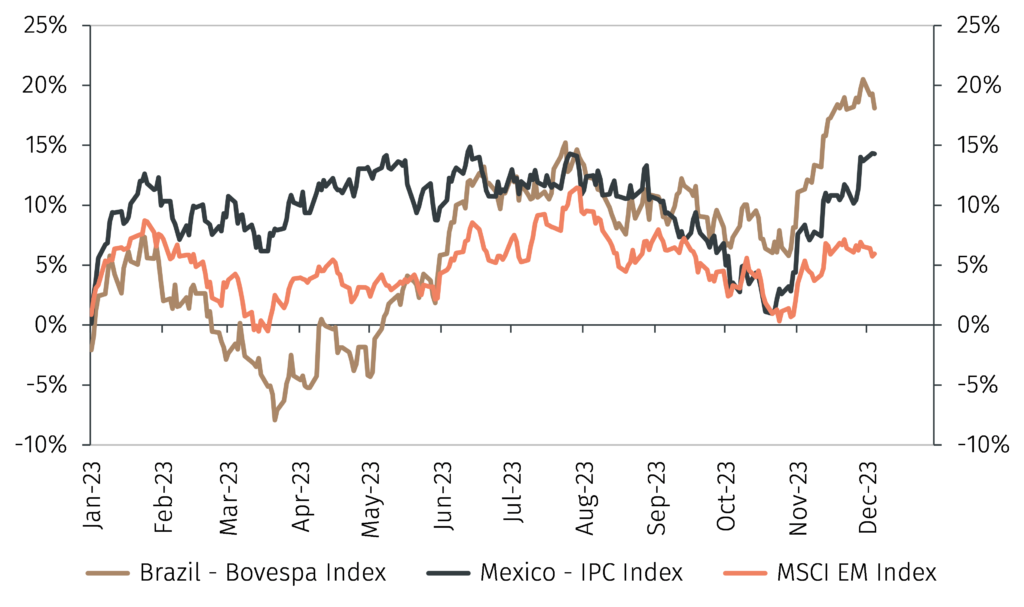

Equity markets had a strong performance year-to-date, with developed market stocks outperforming emerging market stocks by over 10%. Within emerging economies, performance has been mixed. While Chinese stocks are down by over 12% in 2023, equities in Brazil and Mexico are up by 15% and 12% respectively in local currencies YTD. They have both outperformed the MSCI Emerging Markets index this year (see Chart 1). In US dollar terms, stocks in Brazil and Mexico have outperformed the EM index by over 20%.

Chart 1. Outperformance of equities in Brazil and Mexico

(Total Return in local currencies YTD %)

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 7 December 2023.

Looking into next year it is worth analysing the macroeconomic outlook for Latin America’s largest economies. After a year of better-than-anticipated economic performance, 2024 is expected to be characterised by slower GDP growth, monetary policy easing, stronger exports and challenges from fiscal side and climate events.

Brazil

There is anticipation that the global economy will avoid a deep recession next year. In line with that, Brazil is expected to avoid a sharp GDP contraction in 2024. Growth is expected to decline from 3% this year to just over 1.5% in 2024, attributed to a softening of domestic demand and reduced capacity for further fiscal expansion.1 According to IMF estimates, China’s economy growth is expected to decelerate from 5% in 2023 to 4.2% in 2024. Therefore, better-than-expected growth in China, Brazil’s main trading partner, and a soft-landing scenario in the US would support demand for Brazilian exports and contribute to GDP growth. However, volatility in commodity prices and the potential reemergence of inflationary pressures in food prices could create headwinds to activity.

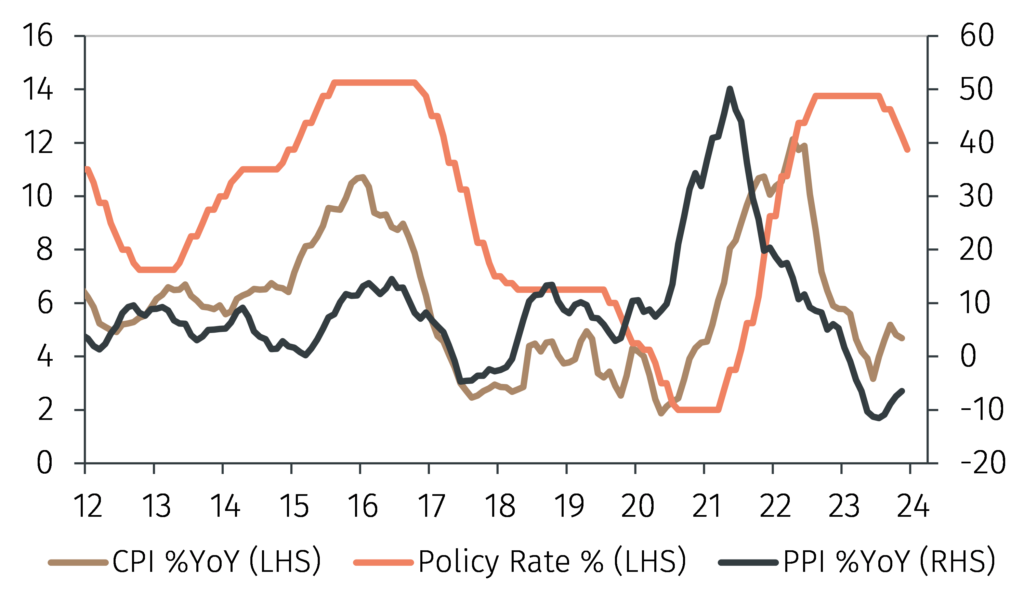

The Central Bank of Brazil has already started easing monetary policy, delivering four 50bps rate cuts since August 2023. The Selic rate, currently at 11.75%, is expected to keep declining to 9%-9.5% by the end of next year. Inflation has fallen from a peak of 12% year-on-year in April 2022 to 4.68% in November 2023, helped by a decline in global goods prices and strong supply of agricultural products (see Chart 2).

However, the impact of El Niño on agricultural and fishing production in 2024 could be meaningful.2 Agricultural output is already expected to be weaker than in 2023 and could exert a potential drag on GDP and inflation by raising food prices.

Chart 2. Central Bank of Brazil already cutting rates following progress to contain inflation

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 14 December 2023.

Reducing the fiscal deficit will be trickier and slower than initially anticipated. The government of President Lula proposed a new fiscal framework with a fiscal deficit target of 0.5% of GDP in 2023 and close to 0% by 2024. This is unlikely to be met. A tax reform would improve the ease of doing business. However, it is still unclear whether there will be political agreement of any significant changes.

Mexico

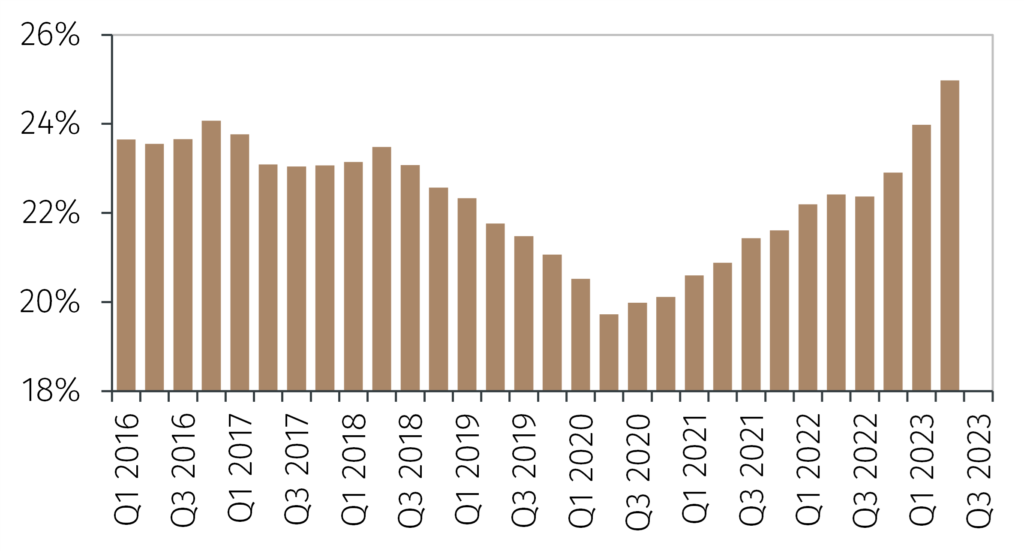

According to IMF projections, Mexican GDP growth is expected to fall from just over 3% in 2023 to 2% in 2024. The strong performance of the US economy in 2023 partially explains the better-than-expected growth in Mexico this year. This has been mostly related to fixed investments, which has only recently recovered from a declining trend between 2019-2020 and had a strong impulse in 2023 (see Chart 3). Mexico will be a clear winner from ensuring supply chains for manufactured goods remain in place and not affected by political noise around the US election. If the US economy slows meaningfully in 2024, it could also expose some of the weaknesses in Mexico.

Chart 3. Mexico gross fixed capital formation

Source: LSEG Data & Analytics and EFGAM calculation. Data as of 7 December 2023.

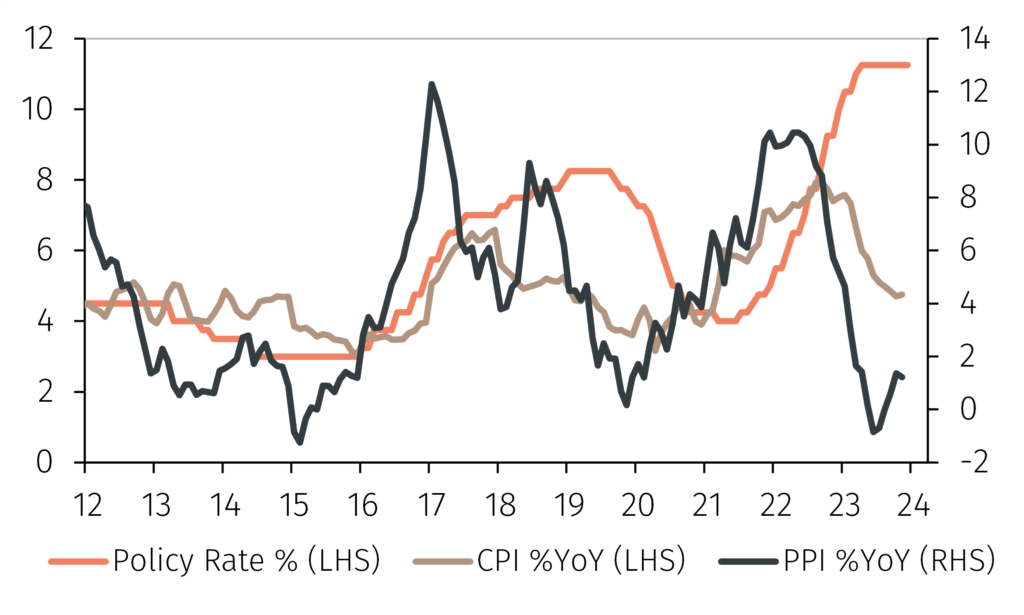

Interest rates have been at a historical high of 11.25% since March 2023. Inflation has declined from a peak of 8.5% year-on-year in September 2022 to 4.3% in November 2023 but remains above the 3% target. The Bank of Mexico is expected to start cutting rates before the end of Q1 2024 (see Chart 4). Together with Colombia, Mexico is among the few central banks in the region that have not already started easing monetary policy.

Chart 4. Bank of Mexico to start easing monetary policy in Q1-2024

Source: LSEG Data & Analytics and EFGAM calculations. Data as of 7 December 2023.

Mexico will hold Presidential elections on 2 June which is likely to keep markets volatile in the first half of 2024. The candidate of incumbent MORENA party, Claudia Sheinbaum, is leading in the polls. She is expected to follow the same line as Lopez Obrador and, if Donald Trump wins the US Presidential election, the relation between Mexico-US should remain respectful. Candidates have not released their economic plans yet, which makes it difficult to anticipate any proposed reforms. But some potential issues have already appeared on the fiscal side, with a fiscal impulse in the first half of the year estimated at around 1.2%-1.5% of GDP, which should fade after the election and coincide with a slowing of the US economy. The overall deficit is expected to widen to over 5% of GDP in 2024.

Conclusion

The outlook for Brazil and Mexico is relatively positive. Next year should be characterized by lower in global GDP growth, and neither Brazil nor Mexico will be able to escape this trend. However, a soft landing of the global economy should help to cushion the impact. Brazil will benefit from strong commercial ties to China while a mild recession in the US will be positive for Mexico.3

The effects of high interest rates will be felt on domestic activity. Central banks are expected to continue, or start, cutting interest rates through 2024 which should give an upside to equity markets. Key challenges concern fiscal policy with reduced capacity to increase spending, given existing fiscal rules, as overall deficits remain high.

Developments around ‘El Niño’ will be important for crops in Brazil and commodity exports. This will be less of a concern for Mexico which relies more on manufacturing exports than agricultural products. Overall, the outlook for the first half of 2024 is supportive of financial markets in both economies. However, challenges could arise in the second half of the year if fiscal problems are not resolved.

1 IMF World Economic Outlook, October 2023.

2 ‘El Niño’ is a climate pattern that describes the unusual warming of surface waters in the eastern Pacific Ocean, affecting ocean currents, coastal fisheries and local weather from Australia to South America.

3 Mexican exports to the US represent 78% of Mexico’s total exports.