In our global investor survey on Asian fixed income, respondents pointed to economic fundamentals – notably, rising inflation, post pandemic GDP growth, and tapering – as key factors that weigh most heavily on their fixed income portfolios. These factors are driving a reassessment of their bond exposures and Asia’s bonds look set to be beneficiaries.

In response to the above macro concerns, the respondents reveal consistent interest in diversifying their bond holdings, reducing their overall fixed income exposure, but also broadening their fixed income portfolios to include new markets and bond classes. Interestingly, the survey reveals that global investors faced with a limited yield potential of developed market bonds are tilting to Asia.

Asia’s long-term growth fundamentals remain attractive and investors globally seem increasingly willing to invest in this growth. Asian government and corporate bonds offer relatively attractive yields compared to similarly rated bonds in the developed markets. We discuss these macro concerns and the impact these may have on Asian fixed income markets amid the current volatile environment.

The end of a low inflation era?

Nearly three out of four respondents in the survey are worried about inflation. This is not surprising since the latest data from North America and Europe indicate that consumer price inflation has hit levels not seen in more than a decade. Inflation has risen in major economies in conjunction with the growth rebound from the impact of the pandemic, higher energy costs and the global supply chain bottlenecks.

While most major central banks in developed markets do not seem to be in a hurry to raise rates and continue to argue that the recent price spikes are “transitory” due to base effects, others have gone ahead to tighten policy. Norway’s central bank is the first in the developed world to raise rates. Bank of New Zealand too raised interest rates for the first time in seven years. Investors are now waiting to see if the US Federal Reserve will be forced to begin raising rates earlier, even before full employment is achieved.

Over in Asia, inflation has remained benign as a result of repeated rounds of lockdowns, which have crimped domestic demand. See Fig. 1. While the recent spike in energy prices has similarly stoked inflationary concerns in Asia, the inflation sensitivity of Asian economies to higher energy prices has historically been relatively muted due to factors such as, price rigidities, the nature of electricity pricing agreements, and time lags. The benign trajectory for food inflation and a negative output gap across most Asian countries will also allow most central banks in the region to stay on hold longer to support the fledgling recovery in the region.

Fig. 1 Asia has enjoyed lower inflation than its peers historically

The only exception being the Bank of Korea, which is the first Asian central bank to hike rates in this policy cycle on the back of rising property prices and robust growth momentum. Asian central banks have demonstrated ability to look past commodity price inflation in the past, seeing it as a tax on growth rather than having long lasting impact on inflation expectations. We therefore expect Asian bond markets to be more resilient than global bond markets given this policy framework.

Global growth recovery to remain uneven

More than sixty percent of the survey respondents ranked post pandemic growth as their next biggest concern. While the World Bank has forecast global growth to expand by 5.6% in 2021, the strongest showing in 80 years, the rebound following 2020’s Covid-19 induced contraction appears to be peaking. Forward looking indicators such as the new export orders index is showing signs of a slowdown. Another issue weighing on survey respondents is the uneven pace of growth. Developed markets seem on track to catch up with the pre-pandemic trajectory of GDP; for the US by 2022 and Europe by 2025. In contrast, this catch-up may not take place in Emerging Markets (EM) and the overshoot in EM growth relative to pre-pandemic forecasts is much more moderate likely due to the deep scarring from the pandemic.

Lagging vaccination rates amid new waves of Covid-19 infections have forced many Asian countries to reimpose social restrictions, curbing domestic consumption, slowing factory production and reducing the pace of growth. China too has recently reported weaker than expected economic activity. That said it is worth noting that should growth slow further in China, there is still a large room for the People’s Bank of China to ease monetary policies as well as provide fiscal stimulus which distinguishes it from the other major economies. This is viewed as a major policy advantage for China.

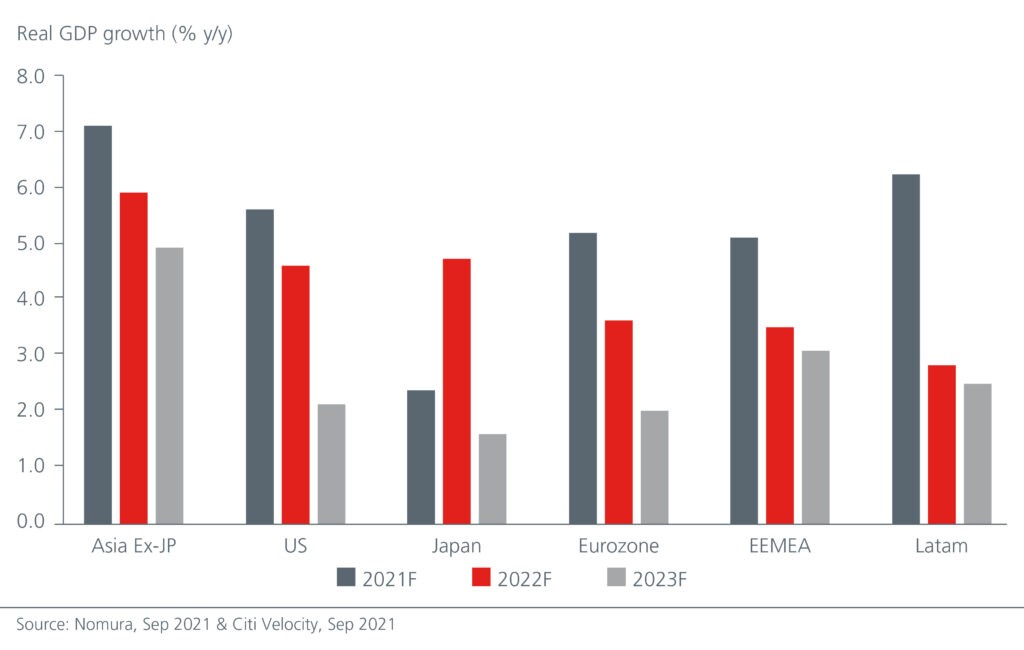

Meanwhile another Asian giant, India, is experiencing strong recovery momentum amidst rising vaccination rates, re-opening, and relatively lower daily Covid cases. The outlook for other Asian countries, where Covid-19 outbreaks have been more severe, is less promising. Still, the region is expected to experience highest growth globally in 2022 and 2023 (see Fig. 2).

Fig. 2. Asia to remain the world’s highest growth region

Tapering without a tantrum

Next, we address the issue of tapering – the 3rd concern cited by the survey respondents drawing reference from 2013’s bond taper tantrum. Then, the US Fed’s tapering signal of the quantitative easing programme came as a shock to markets given that it had only begun a few months earlier. Rattled bond markets were appeased only when the US Fed subsequently set a clear delineation between a tapering signal and an interest rate policy signal.

We think the chances of a tantrum seem less this time. For one, the US Fed’s intention is well telegraphed, and it clearly signalled the year end as the start of the tapering process. Moreover, fixed income markets have also grown substantially since 2013 and the Fed’s asset purchase reductions may not have a significant impact. Investors too appear to have come around the view that tapering is a done deal. This has led to lower amounts of portfolio flows into EMs this time around and in turn limits the impact of a tapering induced volatility for bond markets.

In fact, we believe the risk of early rate hikes is more negative than tapering. For now, we expect the US Fed to hike rates at the end of 2022, six months after tapering ends.

Implications for Asian bonds

At the point of this writing, bond markets have been facing volatility triggered by inflation data and China’s capital markets have seen significant regulatory changes. That said, from a global perspective, Asia remains the high growth region where the movement from traditional bank lending to capital market financing continues.

Given the sanguine inflation outlook in Asia, we are less worried about rate hikes in Asia and we think that the road to policy normalisation seems some time away. This offers tactical trading opportunities in Asian local currency government bonds based on intra-Asian differentiation on interest rate outlook and debt dynamics. Corporate issuers, too, could benefit from the generally supportive macroeconomic picture in the region.

For sure, the Asian high yield credit sector has taken a hit given the ongoing default risks faced by China’s property sector and careful credit selection is required to seize alpha in this segment. In contrast, the order books for Asia high-grade issuers’ bonds have remained healthy. We believe the current global growth forecasts and transitory inflation will remain supportive of risk assets and Asian credits will likely continue to benefit from the global search for yield.