Asia’s dominance of the global semiconductor supply chain is likely to remain unrivalled in the near term. Efforts by the US, Europe and Japan to create a viable alternative, as well as China’s determination to increase domestic chip production, would impact economies, manufacturers, existing supply chain players as well as investors in the longer term.

Asia largely dominates the global semiconductor supply chain. Taiwan Semiconductor Manufacturing Company (TSMC) is the world’s largest foundry, with revenue of USD13.3 bn and a market share of 52.9% in the second quarter of 2021, according to Taipei-based market intelligence provider TrendForce.1 Samsung comes second, followed by United Microelectronics Corporation. In fact, only one firm – Israel-based Tower, on TrendForce’s list of the 10 largest foundries does not come from Asia.

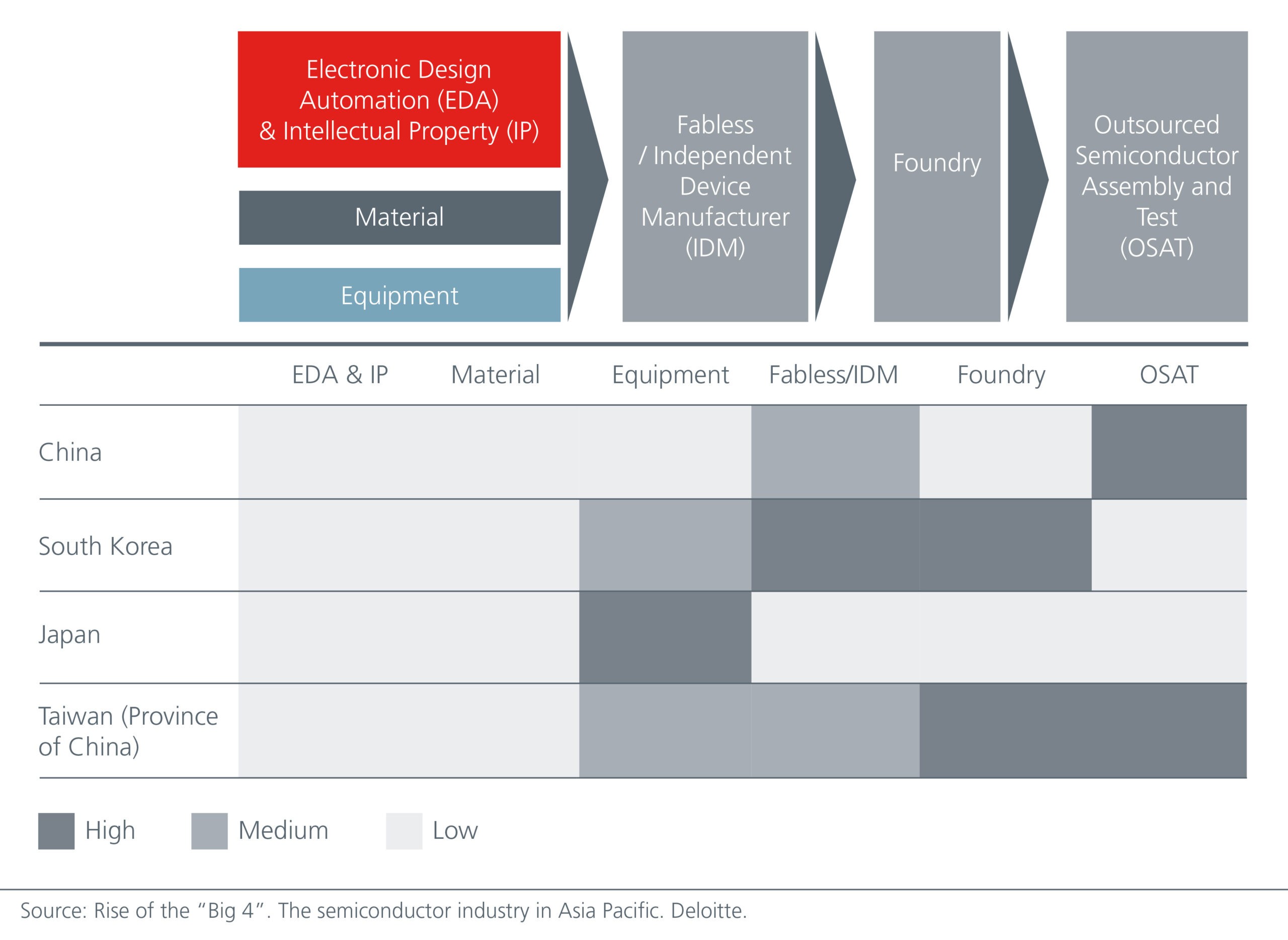

Asian powerhouses are not just found in semiconductor manufacturing, but also in Integrated Circuit design as well as testing and packaging. Many Asian companies are also key suppliers of semiconductor equipment and materials. See Fig. 1. However, multiple factors are driving a reshaping of the global semiconductor supply chain.

Fig. 1. Asia dominates the global semiconductor supply chain

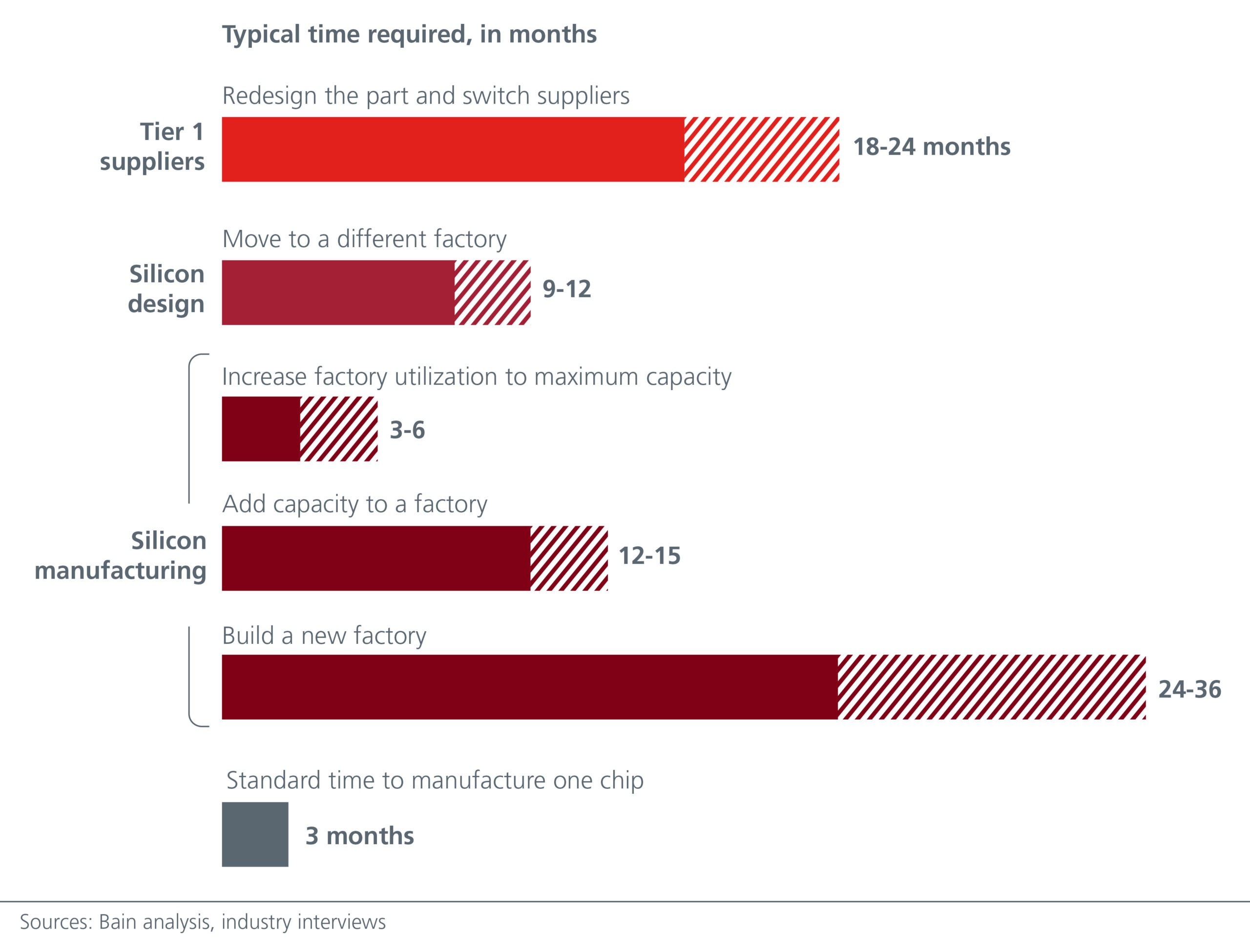

Governments globally are calling for more resilient and alternative semiconductor supply chains as the recent shortages in semiconductor chips hurt production of automobiles, smartphones and consumer electronics. Chip shortages is forecasted to cost the world’s automobile industry USD210 billion in lost revenues this year, according to American consultancy AlixPartners.2 Although the chip shortage is linked to strong resurgent demand as a result of work/learn-from-home set ups and insufficient global semiconductor capital expenditures, the lockdowns and covid-related production disruptions in Asia exacerbated the situation. Unfortunately, most solutions to the chip shortage have long lead times. See Fig. 2.

Fig. 2. Most solutions to the chip shortage have long lead times

With semiconductor chips powering everything from computers to healthcare and military equipment, governments globally are seeing the strategic importance of having their own domestic chip production. Having more than 80% of the world’s semiconductor output concentrated in Asia also potentially holds countries and companies, hostage to geopolitical risks in the region.

Regional hubs in the making

The US government is planning to upgrade its capability to design and manufacture semiconductor chips domestically. Although US companies make 85% of the chip sector’s design software, it only produces 12% of its chips. In the US Innovation and Competition Act, USD52 bn worth of subsidies has been set aside for investments into semiconductors. Part of the country’s strategy is also to have more chips produced by Asian companies in the US. TSMC, for example, already operates a foundry in Washington State and is investing tens of billions of dollars to build factories in Arizona. Samsung has a plant in Texas and recently announced that it would be investing USD17 bn to build a next-generation foundry, likely within the state.

Europe too is looking to become more self-sufficient as chip shortages have crimped economic growth. It wishes to double its share of the global chip manufacturing market to 20% by 2030. The recently announced European Chips Act seeks to create a state-of-the-art European chip ecosystem, including production which will not only secure chip supply but will also develop new markets for ground-breaking European tech. There is likely to be more incentives for investments in the semiconductor industry in Europe going forward.

Meanwhile Japan is seeking to restore some of its former glories. In the late 1980s, Japan’s chip industry was the largest in the world. Its market share has since declined, although Japan still plays an important role in supplying the world with semiconductor equipment and materials. Acknowledging that it would be challenging for one country to supply all the necessary technologies, Japan’s new prime minister Kishida has called for liberal, democratic countries to work together to keep the semiconductor supply chain in friendly hands. In June, Japan approved a USD338 mn semiconductor research project with TSMC. TSMC could also reportedly start operating its first chip plant in Japan as soon as 20233.

The China wild card

As the world’s largest manufacturing hub, China is the biggest semiconductor consumer in the world, yet it only accounts for 7.6% of global chip sales4. Meanwhile 95% of China’s installed chip capacity is for chips with nodes of 28nm or above5, lagging behind industry leaders that are planning to roll out 3nm processes in the near future.

China’s urgency to increase domestic chip capacity and reduce reliance on external suppliers has risen on the back of rising political tension between China and the US. Export bans by US and its allies prevent Chinese companies from accessing advanced chipmaking technology and equipment. China’s road to achieve 70% self-sufficiency in semiconductors by 20256 will require significant amount of capital, talent and time.

That said, China has size to its advantage – its ability to rapidly scale a technology once it reaches maturity is unparalleled. It is also a global leader in outsourced assembly, packaging, and testing (OSAT), with 38% of global market share in 2020. At the same time, China is an important front-end wafer manufacturer with 23% of global wafer capacity located in the mainland. Importantly, China’s semiconductor industry enjoys significant government support.

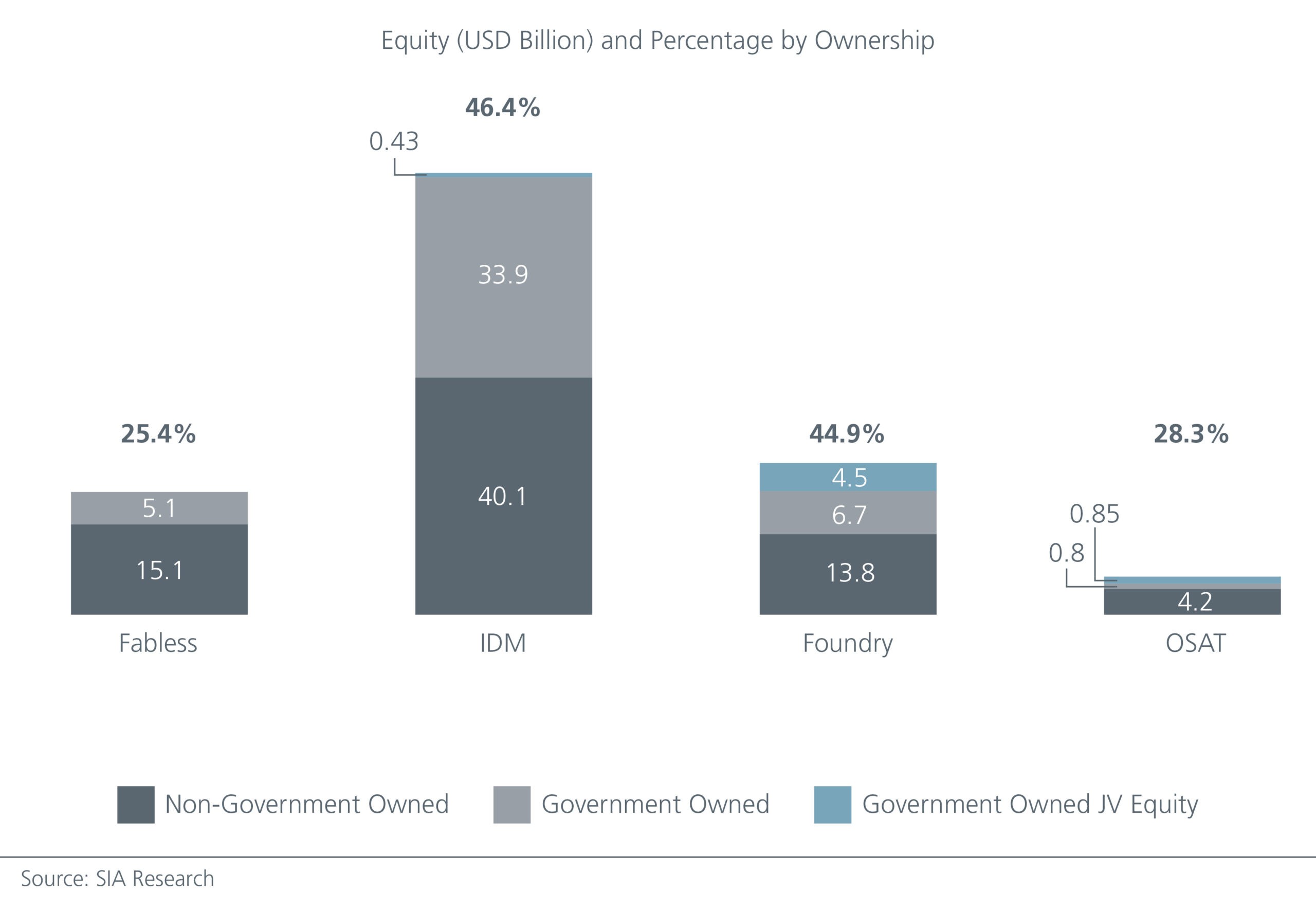

The Chinese government has committed USD150 bn till 2030 to build a thriving domestic IC ecosystem. This does not include the grants, low-cost loans, cheaper utility bills and reduced land costs which the industry enjoys. According to the Boston Consulting Group, the cost of building and operating a fab in China is 37% lower than in the US. With 43% of registered capital (totalling USD51 bn) in the Chinese semiconductor industry directly or indirectly owned or controlled by the Chinese government, the state has significant influence over the direction of the industry. See Fig. 3.

Fig. 3. Equity (USD bn) and percentage by ownership

Implications

In the near term, Asia is likely to continue dominating the semiconductor supply chain given the amount of time, capital, expertise, and supporting ecosystem needed to build up a viable alternative. With the short supply of logic semiconductors including microcontrollers (MCUs) and power management integrated circuits (PMICs), as well as increasing digitalisation, the logic semiconductor value chain is likely to provide attractive opportunities for investors.

In the longer term, a supply chain closer to home can result in lower lead times, greater efficiencies and reduced costs for manufacturers in advanced economies. Having a more stable source of semiconductor chips can help US, Europe and Japan enjoy greater economic security amid heightening global trade tensions. Meanwhile, TSMC and Samsung which are setting up more facilities outside Asia could benefit from having more diversified manufacturing bases and earnings. This could however affect domestic equipment and material suppliers in their respective countries. Companies that have stronger footprints in US and Europe may benefit more in a successful reshaping of the global semiconductor supply chain. Meanwhile, China, despite its challenges, is likely to be able to develop and produce semiconductors which are competitive enough for its needs.