Nearly a third (32%) of discretionary fund managers (DFMs) expect to write more investment trust business over the next six months, according to a survey by Research in Finance*.

Attractive discounts were cited as the top reason for this increase (82%), as well as strong performance of certain trusts (40%), increasing exposure to specialist assets (38%) and a more favourable view of investment trusts generally (38%).

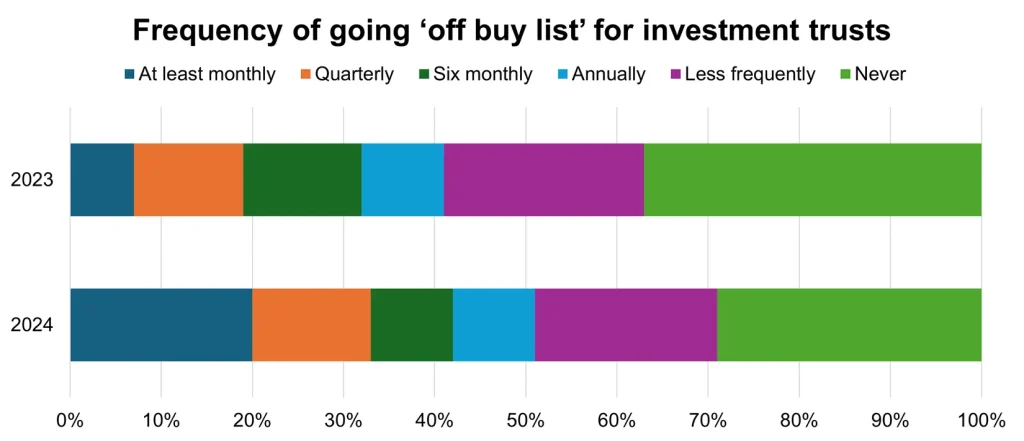

The survey of 157 DFMs, which was funded by a consortium of asset managers and the AIC, also revealed that wealth managers are increasingly turning to investment trusts outside their firms’ buy lists: 20% of DFMs now use off-list investment trusts at least monthly, up from just 7% last year.

The increased use of investment trusts that are not on firms’ buy lists coincides with a period of wider-than-usual discounts for trusts. As one survey respondent said: “We have seen a swathe of activity over recent months where we have sought to exploit attractive discounts across the space.”

Another noted particular interest in the renewables sector. “We are currently reviewing the renewables investment trust space, given the discounts available and structural drivers towards their usage,” they said. “The sector has been particularly hard hit by the interest rate increases and with these set to reduce in the near term [it] could be a good opportunity to buy in.”

Toby Finden-Crofts, CEO of Research in Finance, commented: “Our research shows that it’s not only the structural benefits of the products that are appealing but the access to some interesting and less accessible markets, such as private equity, infrastructure and renewables.”

Accurate cost disclosures could boost the sector further

Clearer and accurate cost disclosures could also mean that wealth managers feel more confident in branching out from their centralised buy lists and increasing exposure to the products in future.

For years, the UK Regulator’s interpretation of EU rules made it appear that investment companies were more costly to put money into than they were, but that headwind was removed on 19 September 2024 when HM Treasury and the FCA announced it was applying forbearance with immediate effect.

Gravis’s William MacLeod commented: “This news was long over-due but extremely welcome. Even though the forbearance is to take place with immediate effect, I suspect it will be November before the effects are felt by investors and investment companies. The database for costs is updated monthly, so it may take a few weeks for accurate costs to become the norm once more. As shareholders, wealth managers and their clients have been in steady decline for nearly seven years. I doubt we will see a rush to access these companies but a return to more normal levels of retail investor ownership now seems probable.

“There will be consultation on the replacement of PRIIPs legislation with the new CCI regime, which is eagerly anticipated. I can’t help but mention that the LSE response to the last consultation on this very topic resulted in 330 signatories requesting the exclusion of investment companies from the CCI. HM Treasury have announced there will be specific rules for investment companies which I’m sure everyone is keen to study and consider. ”

The full details of the announcement can be viewed here.

Important information

*The UK Investment Trust Study (UKITS) from Research in Finance is an annual survey of DFMs who are investment trust buyers. This year, 157 DFMs were surveyed, of whom 87% (137) were from firms with a centralised buy list.

This article has been prepared by Gravis Capital Management Ltd (“Gravis”) and is for information purposes only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Any recipients of this article outside the UK should inform themselves of and observe any applicable legal or regulatory requirements in their jurisdiction and are treated as having represented that they are able to receive this article without contravention of any law or regulation in the jurisdiction in which they reside or conduct business.

This article should not be considered as a recommendation, invitation or inducement that any investor should subscribe for, dispose of or purchase any such securities or enter into any other transaction in a fund affiliated with Gravis.

No undertaking, representation, warranty or other assurance, express or implied, is made or given by or on behalf of the Investment Manager or any of their respective directors, officers, partners, employees, agents or advisers or any other person as to the accuracy or completeness of the information or opinions contained in this article and no responsibility or liability is accepted by any of them for any such information or opinions or for any errors, omissions, misstatements, negligence or otherwise. In addition, the Investment Manager does not undertake any obligation to update or to correct any inaccuracies which may become apparent. The information in this article is subject to updating, completion, revision, further verification and amendment without notice.

Past performance is no guarantee of future performance.

Gravis Capital Management Ltd is authorised and regulated by the Financial Conduct Authority and its principal place of business is 24 Savile Row, London W1S 2ES.