As investors reassess their risk expectations towards the Chinese property sector and the Asian High Yield bond market, we believe that opportunities exist for the discerning investor. While we remain selective in the near term, we note that the incentive for China’s property sector to deleverage has never been stronger, paving the way for better fundamentals over the longer term.

In the recent weeks and months, uncertainty over property developer Evergrande’s ability to meet its interest and coupon payments had sent ripples across Asia’s bond market, and in particular the Asian High Yield bond market.

This is hardly surprising since China accounts for 50% of Asia’s High Yield bond market, with the Chinese property sector making up a significant share. In the near term, the developments surrounding Evergrande are likely to weigh on investor sentiment towards the sector.

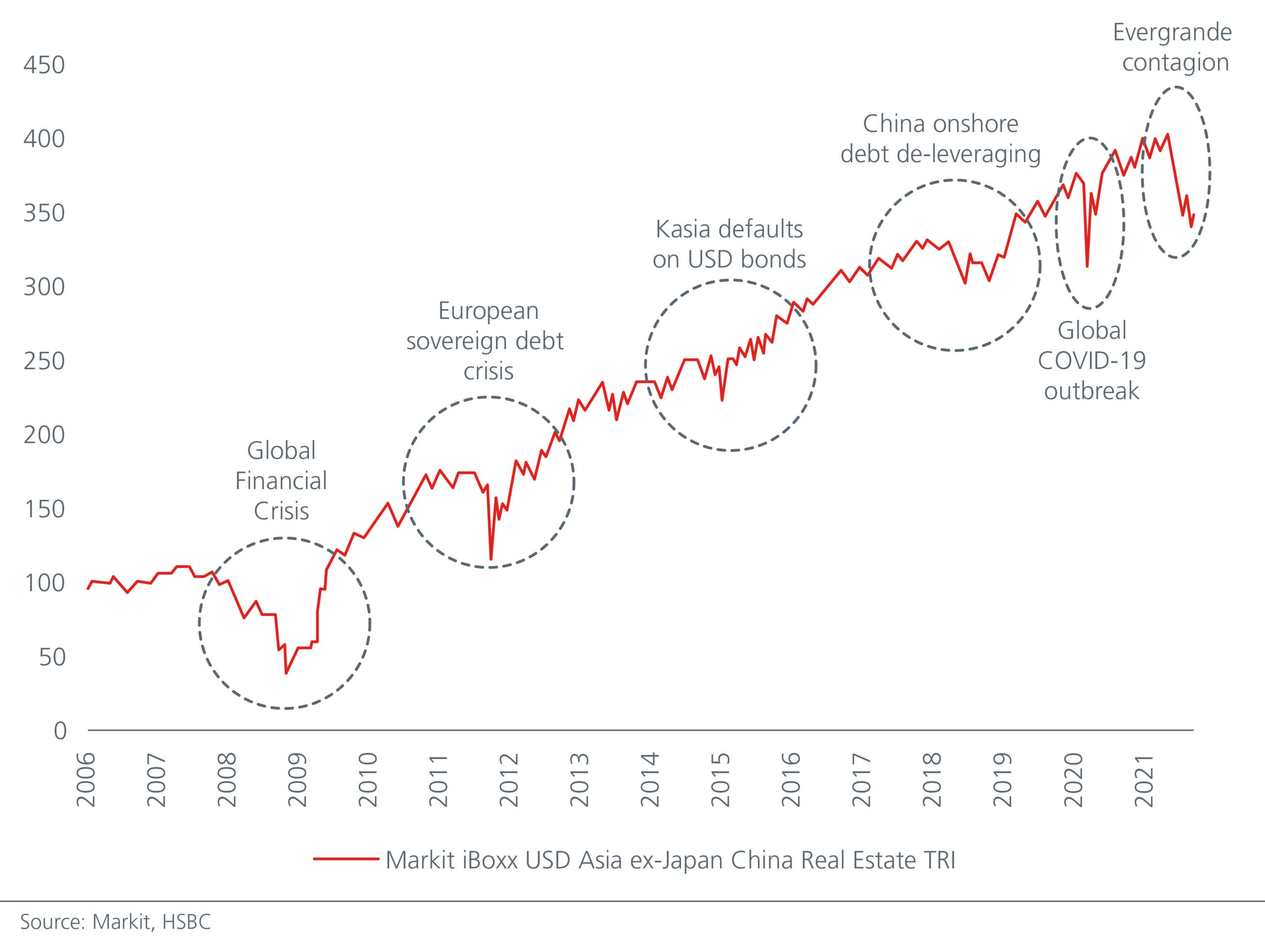

The Asian High Yield bond market is no stranger to volatility, yet, the market has been able to deliver positive returns to investors over the long term. See Fig. 1. That said, the Evergrande episode presents longer term ramifications and lessons for investors.

Fig. 1. Positive long term returns despite volatility

Reassessing risk expectations

Investors are likely to reassess their risk expectations towards the Chinese High Yield property bond sector. This would probably result in higher bond yields and wider spreads. Single B-rated issuers and companies with a weaker liquidity profile will find it increasingly challenging to access funding, since the Chinese government’s policy measures to rein in leverage in the property sector are likely to stay.

In recent months, the Chinese authorities had weighed in on mortgage approvals and borrowing rates for first time home buyers, tempered the pace of rental growth in the cities and lowered the premiums developers paid for land. In the first half of 2021, the more stringent mortgage policies slowed cash collections at the property companies, while housing price caps and elevated land costs caused gross EBITDA and margins to trend lower. Meanwhile, although some companies made progress in meeting the government’s “Three Red Lines” policy by June this year, investors need to ensure that improvements in the debt ratios did not come at the expense of higher commercial acceptance bills and minority interests.

This reassessment of risk expectations in the China property sector will instil greater discipline among investors, and companies. Investors will need to be more discerning while the aggressive “high growth-high leverage” business model pursued by many property developers may gradually become a thing of the past. The latter would be in line with the Chinese government’s goal – to bring down leverage in the property sector, increase housing affordability and to direct resources to other strategically important sectors such as advanced manufacturing, technology and renewable energy.

A healthy property sector desirable

While China’s property sector has historically been subject to episodes of policy-driven volatility, it remains an important driver of the Chinese economy for now. It accounts for 27.3% of the country’s Fixed Asset Investment in 2020 and is a key revenue source for many local governments. The Chinese government would therefore prefer to have a healthy property sector than to see multiple large-scale defaults, which could potentially trigger widespread systemic risks.

Chinese property developers had enjoyed positive revenue growth in the first half of 2021 and the contracted sales performance in the first eight months of the year has also been decent. Encouragingly, property inventory (link to Chart of Month article) levels are also much more reasonable. Many developers had slowed down land bank acquisitions in the first half of the year which have helped to conserve cash as liquidity conditions tightened. While debt/EBITDA ratios may have deteriorated marginally in the first half of this year on the back of lower profit margins, net debt/equity and debt/capital ratios were generally stable if not slightly lower compared to end 2020’s levels.

Over the longer term, China’s growing middle class, urbanisation and the development of China’s megacities are likely to continue to support the revenues of the property sector. China’s deleveraging exercise will also ultimately instil stronger market discipline and improve credit fundamentals across the sector.

Opportunities for the discerning

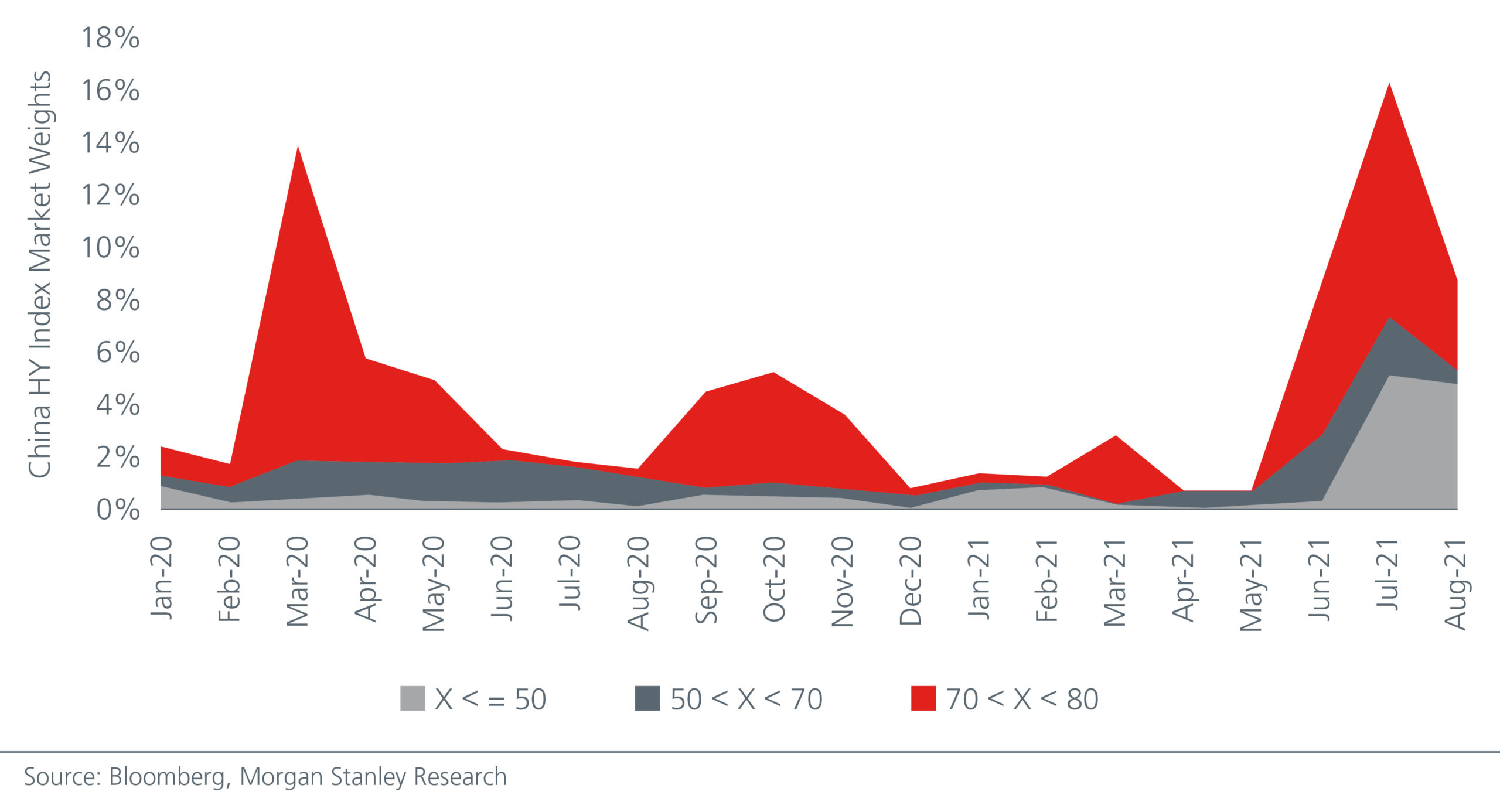

Although investors may expect higher default rates in the Asian High Yield bond market going forward, we believe that opportunities exist for the discerning investor. In China’s High Yield bond market, the percentage of bonds trading below fifty cents to the dollar has risen sharply in recent months. See Fig. 2.

Fig. 2. Investors are already pricing in higher default rates