The recent release of fourth quarter economic data from Beijing confirmed that the Chinese economy grew 5.2% in 2023, hitting the government’s target of “around 5%”. However, base effects due to slower growth in 2022 masked underlying weakness. In this Macro Flash Note, Economist Sam Jochim analyses the latest data.

The National Bureau of Statistics (NBS) reported that China’s GDP grew by 1.0% quarter-on-quarter in Q4 2023 in seasonally adjusted terms. This was below the 1.5% expansion in Q3 2023, yet year-on-year growth increased from 4.9% to 5.2%. The reason for this was the base effect.

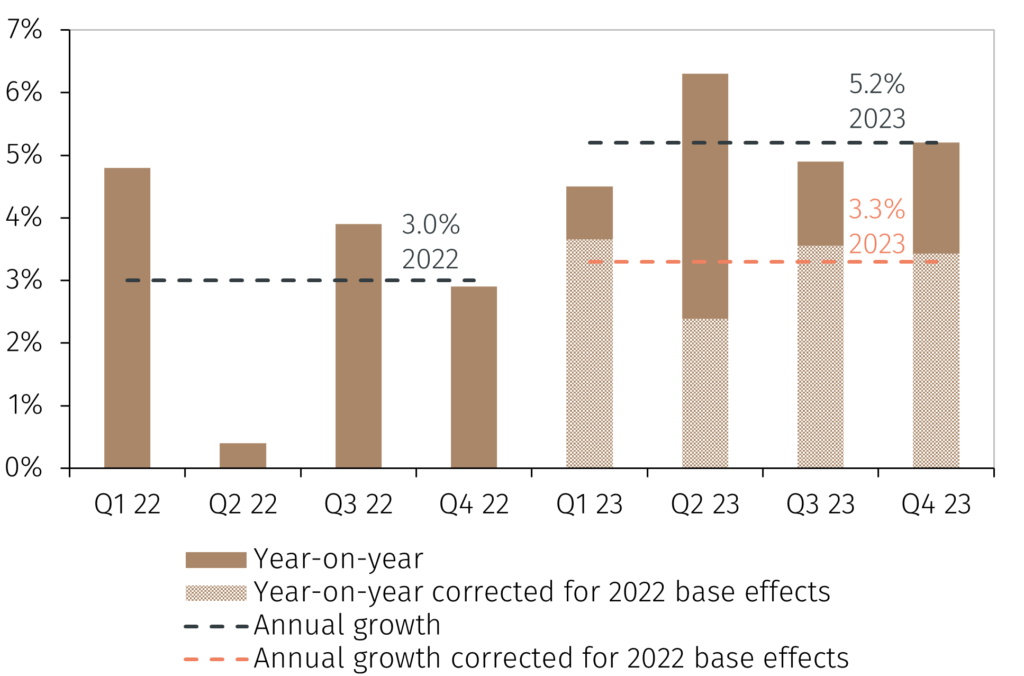

China’s year-on-year GDP data in 2023 has been consistently flattered by the fact it is relative to a year of weak growth in 2022, when the economy’s slowdown was compounded by President Xi’s zero-Covid policy. Positive base effects have therefore masked underlying weakness in GDP data in 2023. While the NBS reported that the Chinese economy grew 5.2% in 2023, EFGAM calculations show that in the absence of base effects, this growth rate would have been around 3.3% (see Chart 1).1 This implies that base effects boosted China’s annual GDP growth by 1.9 percentage points last year, consistent with the 2 percentage points reported in the Financial Times.2, 3

Chart 1. China’s GDP (% change, year-on-year)

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 18 January 2024.

It is difficult to assess accurately the true impact of base effects without using a robust statistical analysis. For reference, GDP measured as a two-year compound annual growth rate rose 4.1% in 2023, above our initial calculation but still below the NBS data and government target. What is clear is that without base effects, the picture is one of a Chinese economy that struggled to gain meaningful momentum in 2023. Multiple factors contributed to what became a disappointingly predictable pattern of underwhelming economic data releases.

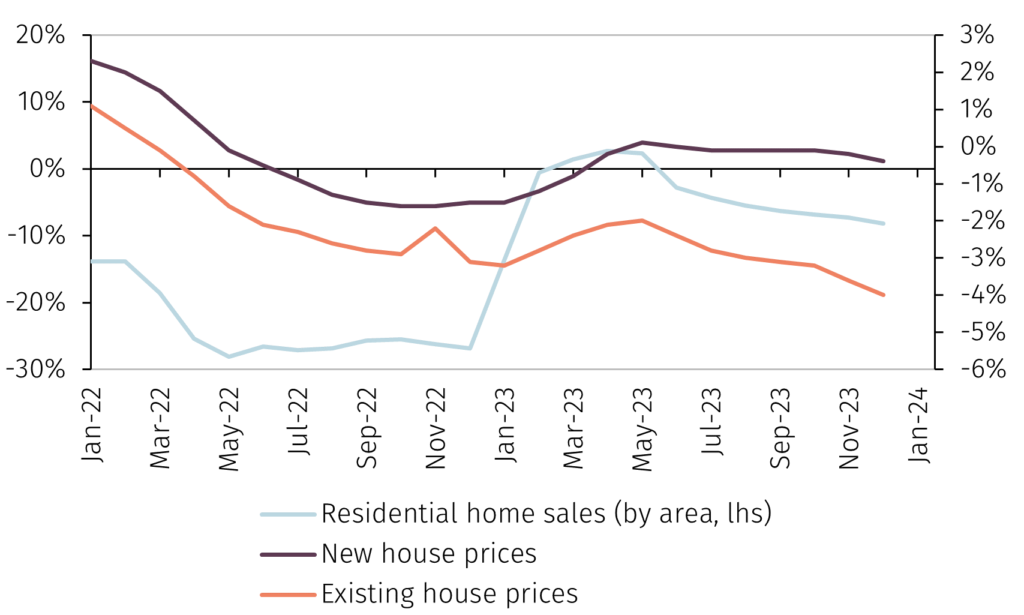

Perhaps most notable was the impact of the real estate crisis. China’s government aimed to support the sector through a range of policies in 2023, though the measures appeared to have little impact.4 With ongoing property sector deleveraging, real estate investment has been in a declining trend for over a year, decreasing 9.6% year-on-year in December, and home prices and sales have been falling (see Chart 2). The recent announcement that China’s housing ministry and financial regulator will create a fund to support the financing needs of real estate projects may provide a glimmer of hope for the sector in 2024, though the material impact is yet to be discovered.5

Chart 2. China’s real estate prices and sales (% change, year-on-year)

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 18 January 2024.

Real estate makes up around 70% of gross household wealth in China.6 Falling house prices therefore create a significant negative wealth effect, which provides one possible explanation behind weak consumption in 2023. Given consumption accounted for 82.5% of annual GDP growth last year, continued declines in wealth pose serious risks to China’s growth outlook in 2024. This is compounded by the absence of a low comparative base, which boosted 2023’s numbers. For example, retail sales rose 7.4% year-on-year in December but just 2.7% when measured as a two-year compound annual growth rate.

What’s more, the situation could get worse. While the overall unemployment rate in China was low at 5.1% in December, youth unemployment stood at 14.9%.7 Notably, this is the first month it has been published since June 2023 when a record high 21.3% was reported. Since then, Beijing has corrected its methodology to exclude students, meaning it is difficult to say how December’s figure relates to June’s. High youth unemployment constrains the demand for new homes in the short-term. A shrinking population will compound this in the medium- to long-term.

In turn, local governments have a funding problem. Sales of land use rights is the largest source of non-tax revenue for local governments, which face around RMB 1.69 trillion (USD 237 billion) of debt maturing in the first half of 2024.8

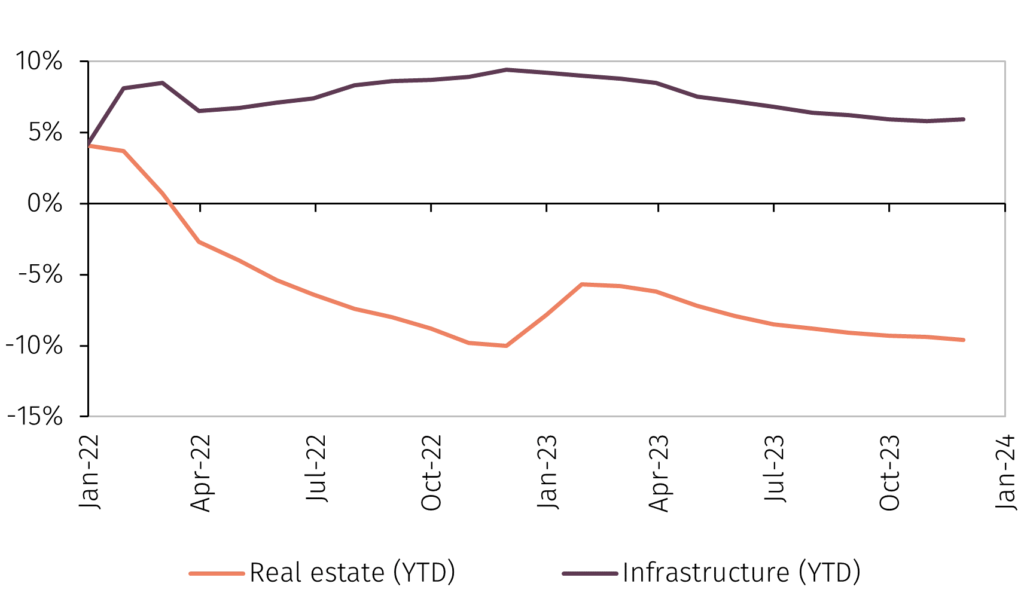

Nonetheless, infrastructure investment, which is financed by local governments, remained strong in 2023 (see Chart 3). Stimulus in 2024 will likely focus on supporting this expenditure, which will be an integral driver of China’s economic growth this year. A case in point was the issuance of RMB 1 trillion (USD 140 billion) of sovereign bonds in October 2023, focused on preventing a decline in infrastructure investment in Q1 2024.9

Chart 3. China’s fixed asset investment (% change, year-on-year)

Source: LSEG Data & Analytics and EFGAM calculations. Data as at 18 January 2024.

In summary, China’s economy grew 5.2% in 2023, hitting the government target of “around 5%”. However, this number was flattered by large base effects. The property sector deleveraging continues to weigh on the economy and is a further headwind for consumption and local government finances. Stimulus to date has focused on preventing a decline in infrastructure investment and more is possible in 2024. In the absence of positive base effects this year, it is possible that China’s economic growth continues to slow. Beijing will set its GDP growth target at the National People’s Congress in March, which will be a key watchpoint to set expectations for the year ahead.

1 EFGAM’s calculations were made by performing OLS regressions on quarterly GDP growth rates from 2010-2019 and using this to back out trend-implied growth rates for each quarter in 2022. New GDP data was then estimated for each quarter of 2022 and year-on-year growth rates for 2023 were calculated based on this new data.

2 https://go.pardot.com/e/931253/43-566e-461f-a865-f9e215459cc7/3vyrk/317325628/h/T6o4vNA3u1pd6QwYXjZF81VQBWfDEwRpusHTYQzCifE

3 As a robustness test, GDP measured as a two-year compound annual growth rate rose 4.1% in 2023, above our initial calculation but still below the NBS data and government target.

4 A timeline of key measures taken to support the real estate sector in 2023 is provided here: https://go.pardot.com/e/931253/ed-property-sector-2023-11-08-/3vyrn/317325628/h/T6o4vNA3u1pd6QwYXjZF81VQBWfDEwRpusHTYQzCifE

5 https://go.pardot.com/e/931253/ion-housing-sector-2024-01-12-/3vyrr/317325628/h/T6o4vNA3u1pd6QwYXjZF81VQBWfDEwRpusHTYQzCifE

6 https://go.pardot.com/e/931253/roding-faith-in-the-government/3vyrv/317325628/h/T6o4vNA3u1pd6QwYXjZF81VQBWfDEwRpusHTYQzCifE

7 Youth unemployment in China is defined as the unemployment rate for persons aged 16 to 24.

8 https://go.pardot.com/e/931253/nment-debt-sources-2023-10-17-/3vyry/317325628/h/T6o4vNA3u1pd6QwYXjZF81VQBWfDEwRpusHTYQzCifE

9 https://go.pardot.com/e/931253/bt-support-economy-2023-10-24-/3vys2/317325628/h/T6o4vNA3u1pd6QwYXjZF81VQBWfDEwRpusHTYQzCifE