Boston – Fixed income markets are experiencing a challenging start to 2022. Heightened volatility in interest rates and credit spreads have driven returns lower across the yield curve and most sectors. In our view, actively managed multisector strategies — with a focus on higher-yielding, short-duration securities — can provide opportunities to reduce interest-rate risk and potentially improve returns.

Bond markets are reacting to a pivot by central banks toward a much earlier and quicker pace of monetary policy normalization than initially expected. That pivot is in response to inflation, which is proving persistent and poses risks to the upside. More recently, the geopolitical developments unfolding in Ukraine have added to economic uncertainty and volatility.

In response to events, the U.S. bond market has repriced sharply, leading to higher interest rates at the short end of the yield curve (1-3 years) than at the longer end (10-30 years).

Bond market repricing quickly

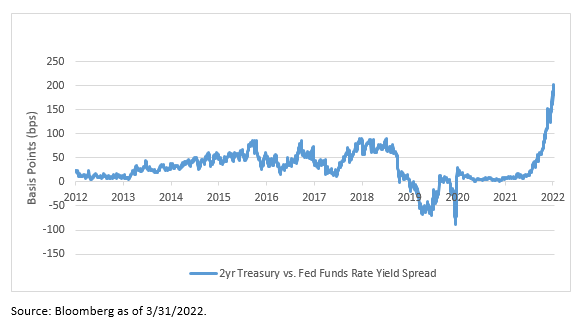

At the beginning of the year, market pricing implied the Federal Reserve would deliver three 25-basis-point interest-rate hikes in 2022. After the Fed began the rate-hiking cycle at its March 15-16 meeting, market pricing moved to suggest more than nine hikes for the year, implying moves in increments of 50 basis points. As a result, interest rates have risen across the yield curve, most noticeably at the front end. The two-year Treasury note is higher by more than 160 basis points since the start of 2022 (Display 1). Such steepness at the front end of the yield curve is highly unusual at the beginning of a rate-hiking cycle, which could boost the draw of these securities for investors.

Display 1: Sharp Rise at Front End of Yield Curve in 2022

Repricing in the bond market has led to a sharp rise in short-term rates, as illustrated by the move of the two-year Treasury note, increasing the attractiveness of this part of the market to short-term investors.

Consider risk-reward profiles of short-duration securities

We believe opportunities on the front end of the yield curve are now more attractive than on the long end, given the rapid repricing in the bond market. We think several factors — volatility, economic data (particularly inflation) and more clarity around Fed intentions — could lead to further repricing, with the potential for an overshoot. Current valuations, however, provide a strong investment case for short-duration fixed income securities:

1. A significant number of rate hikes have already been priced in. Starting yields matter, as they cushion the impact of rising rates.

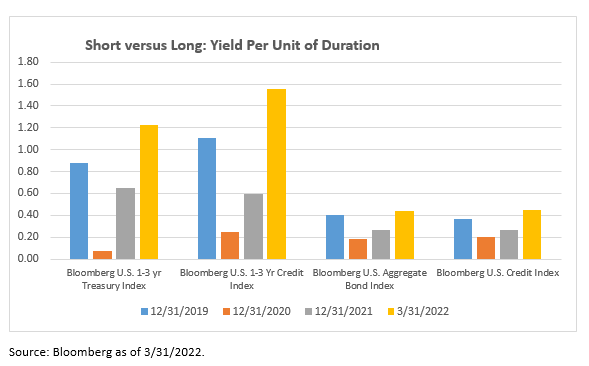

2. Yields at the front end of the yield curve (1-3 years) look attractive relative to the longer end (10-30 years). Indeed, the flattening of the curve has left the front end providing considerably more yield per unit of duration risk — a measure of sensitivity to interest rates — than the intermediate and longer ends (Display 2).

3. Yields on many short-duration sectors are now materially higher than yields on longer-duration sectors — giving investors another reason to reexamine the risk-reward trade-off of short strategies.

Display 2: Short-Duration Yields Rise Sharply in 2022 Relative to Long

Applying a multisector approach

Actively managed multisector strategies can provide further opportunities to reduce interest rate risk and potentially improve return in a rising rate environment. To capture the best opportunities, we see value in overweighting certain securities typically not held in benchmark indexes, including:

Floating-rate securities: These securities feature coupons that reset higher as short-term rates rise — a feature that offers some principal protection, given their inherently very short duration. We find significant opportunities in the investment-grade part of this market, including U.S. money center banks and AAA-rated senior tranches in the non-agency commercial mortgage-backed securities (CMBS) sector.

Securitized assets: Asset-backed securities (ABS), such as consumer and auto loans, offer short durations and often amortize, paying down a portion of their principal each month alongside their coupons. In a rising rate environment, this allows investors to reinvest these proceeds at higher yields and reduces volatility, given the “pull-to-par” nature of the securities.

Short-duration high yield: Given our expectations for a strong economy and low default rates in 2022, we continue to focus on high-yield “rising star” candidates — issues moving from high yield to investment grade. We believe spreads on select BB-rated securities are attractive and should help mitigate interest-rate volatility with their higher yields. The potential for spread tightening on ratings upgrades could further enhance total returns.

Fundamentals favor companies and consumers

The sharp rise in interest rates has been accompanied by wider credit spreads in many sectors. We attribute this to broader market volatility and elevated bond supply in the market, rather than a deterioration in credit fundamentals. Corporate and consumer balance sheets are coming into this hiking cycle from a position of strength. Continued strong earnings growth and net cash positions built during the recovery should benefit corporations, while leverage in the consumer sector has declined. Strong employment and wage growth should help to at least partially offset the impacts of higher inflation.

We continue to avoid the higher-quality parts of the nonfinancial corporate bond market, where narrow spreads offer poor relative value and do not compensate for some deterioration in fundamentals. We are maintaining above-average portfolio liquidity, which allows us to take advantage of opportunities as they arise.

Bottom line: Higher inflation and rising interest rates have led to volatility and repricing in the fixed income market. Alongside repricing, the yield curve has flattened, with short-duration securities now offering higher yields than longer-duration bonds. As both inflation and rates are likely to move higher in the foreseeable future, we believe short-duration securities offer many investors an attractive option, particularly an active, multisector approach.

Past performance is no guarantee of future results.

Bloomberg 1-3 U.S. Treasury Index measures the performance of U.S. Treasury bonds maturities of 1-3 years.

Bloomberg U.S. 1-3 Year Credit Index measures the performance of investment-grade U.S. corporate securities and government-related bonds with maturities of 1-3 years.

Bloomberg U.S. Aggregate Bond Index is an unmanaged index of domestic investment-grade bonds, including corporate, government and mortgage-backed securities.

Bloomberg U.S. Credit Index measures the performance of investment-grade U.S. corporate securities and government-related bonds.

Investing entails risks and there can be no assurance that any strategy will achieve profits or avoid incurring losses.

The value of investments may increase or decrease in response to economic, and financial events (whether real, expected or perceived) in the U.S. and global markets. As interest rates rise, the value of certain income investments is likely to decline. Investments in debt instruments may be affected by changes in the creditworthiness of the issuer and are subject to the risk of non-payment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Investments rated below investment grade (sometimes referred to as “junk”) are typically subject to greater price volatility and illiquidity than higher rated investments.