Private credit is growing in importance as a source of capital. It gives investors premium yields and flexibility, but requires specialist skills and market access.

Growing in importance

Private credit may have started as a niche of the bond market, but it is fast growing in importance – thanks to its attractions both as an asset class with stable risk adjusted returns and as a source of corporate funding. For investors, it offers both alpha (additional yield) and an ability to tailor lending to meet a preferred risk profile. For borrowers, it helps to diversify sources of funding, particularly in the segment of the market dependent on underwritten and syndicated bank loans.

In a nutshell, the borrower gets more flexible access to capital, the investor the possibility of securing higher returns.

For a relatively new market, which began life as a source of liquidity when the global financial crisis caused high yield and syndicated loan markets to seize up, private credit is already showing great potential.

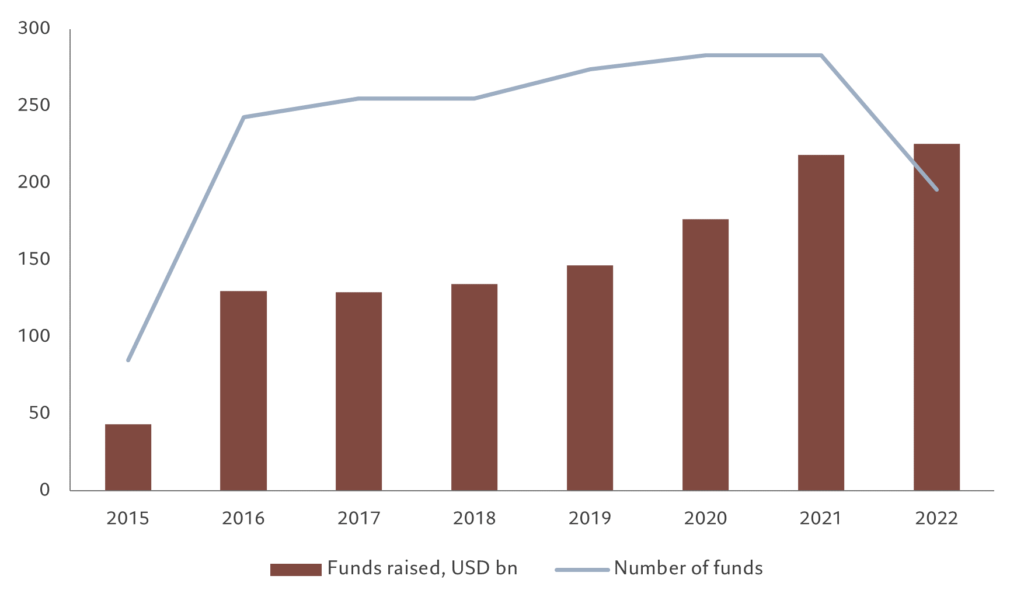

The investment industry holds some USD1.5 trillion dedicated to private credit, albeit USD500 billion of that is still in the form of dry powder – money held by investors but yet to be lent – according to Morgan Stanley estimates.1 Demand has been growing at around 10 per cent a year during the past decade, broadly keeping pace with the much larger private equity segment. Overall, the market for private credit has the potential to grow to some USD3 trillion over the next decade, which is roughly 10 per cent of the USD37 trillion fixed income market, according to Bloomberg Intelligence.2

Fig. 1 – Burgeoning market

Global private debt fundraising, USD bn, and number of funds

There are several trends fuelling this growth. For one thing, tighter regulations are making it more onerous for banks to lend to companies. At the same time, managers and owners of smaller and mid-sized companies are increasingly turning their backs on the equity market for finance – whether because they are wary of the regulatory burden of a public listing or because they don’t wish to dilute their own stakes. These trends have emerged at a time when investors are looking for better ways to allocate long-term capital, (i) with equity-like returns but without the volatility and (ii) with fixed-income-like yield stability but without duration risk.3

[1] https://www.ft.com/content/42297b43-7918-4734-b6d5-623c6d6fa00f?shareType=nongift

[2] “Private credit vs banks, asset-based finance,” Bloomberg Intelligence, 09.06.2023

[3] Duration expresses the degree to which bond prices move when interest rates change. High duration implies that a rise in official interest rates will result in a larger fall in the price of the underlying bonds

New sources of funding

When Silicon Valley Bank (SVB) and Signature Bank failed back in March, fears rippled through the US economy that small- and medium-sized companies would find themselves starved of new funding. The funding squeeze, however, had in fact long pre-dated those banking failures with the raft of regulatory changes that were introduced in the wake of the global financial crisis of 2008. Capital requirements became more demanding making it harder for banks to extend loans to riskier borrowers. These capital requirements are set to increase, intensifying the need for alternative financing.

Meanwhile, the jump in official interest rates that fatally wounded SVB and other banks had already caused a spike in volatility in the asset backed securities market – an important source of corporate funding, for which banks have been traditional intermediaries.

Time was when corporate management might have sought an alternative source of funding by selling equity in the public markets. But during recent decades that’s become a less attractive source of capital.

Private sources of capital are helping to fill the gap. Hitherto, that’s mostly been private equity. But private credit is fast growing as investors become aware of the attractions of this new asset. And while private credit has served the mid-sized market for some time, it is fast becoming a presence in the wider market as an alternative to syndicated leveraged loans, which means providing credit to larger firms as well.

A capital solution

Investors are being drawn to private credit for a variety of reasons.

Not least rising interest rates.

Because private credit, specifically senior direct lending, tends to be in the form of floating-rate loans, these tend to be attractive in an environment in which central banks are tightening or keeping rates high longer than had been anticipated – as is the case now.

And because private lending locks investors in for longer periods, it offers an uplift on the yields available in public markets – for each level of risk.

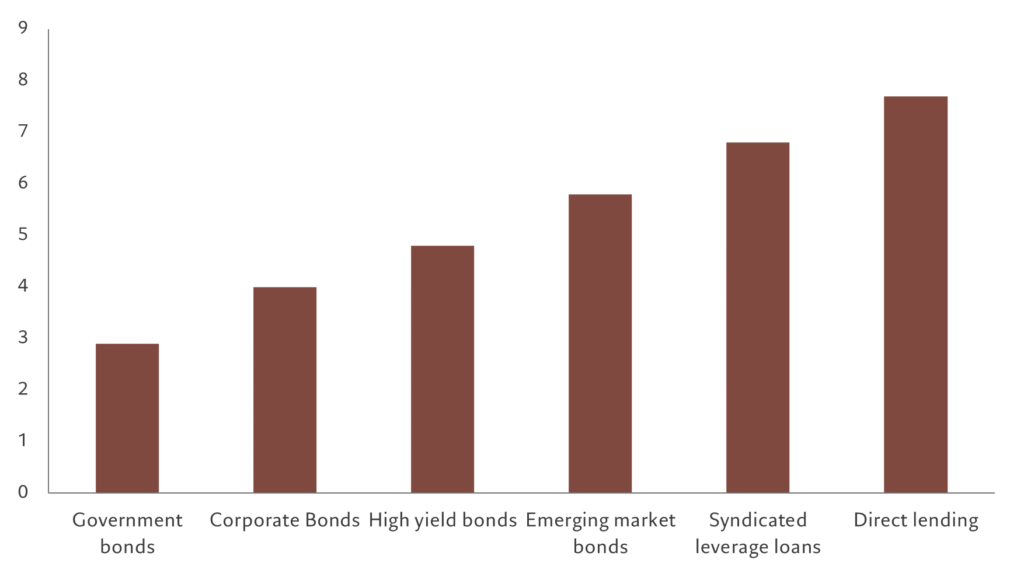

Goldman Sachs research shows that direct lending has consistently produced better returns than high yield credit and leveraged loans over the long run.

From 2010 to 2022, direct lending has generated 10 per cent average annual returns, compared to 4 per cent for high yield debt and 3.2 per cent for leveraged loans, the investment bank found. What’s more, by being locked into their holdings for longer periods, investors are less vulnerable to the psychological pressure exerted by minute to minute market repricing. It protects them from a key source of underperformance – selling at the bottom. They can also benefit from the stricter lender-protection covenants than are typical in the public markets, where the syndication of loans among a number of investors tends to favour a lowest-common-denominator approach to investor protection.

Fig. 2 – Beating the field

Risk adjusted yields adjusted for long-term loss rates, %

Source: StepStone, Q2 2022. Public Markets Data: Government Bonds Data based on Barclays US Agg. Treasuries; Investment Grade Credit reflects the yield to worst of the Barclays Global Agg. Corporate index; HY Bonds Data based on CS HY Index; Syndicated Leveraged Loans based on yield (3yrs life) on BB rated loans and the Broad index (CS data) minus the historical loss rate since 2010 as of April 2022. Direct Lending Data: Direct Lending First Lien based on Thomson Reuters and StepStone estimates (Loss rate estimation on StepStone’s database); Direct Lending Second Lien Loans based on yield of Second Lien loans (Thomson Reuters and StepStone estimates) minus the estimated loss rate for second liens (estimation on StepStone’s database) as of April 2021. Long-term average loss rate based on data series available for the respective asset class from 2004 onward.

For borrowers, the bespoke nature of the loan agreements serves to provide more tailored solutions to capital requirements. Access to senior direct lending can prove a dependable source of capital that’s much quicker to raise than through the traditional bank loan syndication process. Companies are willing to pay a premium for that access.

In cases in which companies have secured long-term funding at lower rates, demand for fresh capital can be met with privately raised mezzanine debt (see box below). This avoids breaching most favoured nation clauses. These clauses force issuers to reprice any existing senior debt if the new issuance at an equivalent seniority is made at higher interest rates, so that existing investors don’t lose out. Some company owners also prefer mezzanine debt financing to issuing equity, because it prevents ownership dilution.

[See Box for various types of private credit]

Specific risks, specialised skills

Although private credit offers investors the flexibility to mitigate risks, as with any bespoke contracts loan agreements need to be structured carefully.

But at the same time, direct lenders need to understand the nature of the collateral, not least how to claim in the event of default and how to realise the value.

They also need to familiarise themselves with the intricacies of the markets the companies operate in. Some borrowers will inevitably fall on hard times. How portfolio managers deal with these periods to keep loans performing is crucial in generating excess returns.

“Private credit can be an important source of returns at a finely tuned level of risk. “

Carefully constructed portfolios in which loans are diversified across sectors and geographies are a minimum. Given the locked up nature of the capital, understanding their liquidity needs is paramount.

And given that private credit’s performance has historically been based on low and stable interest rates, the new era of higher, more volatile rates will prove a challenge as well as an opportunity. Previously, many lenders were rewarded for taking on more risk when underwriting loans. Now, the rewards are more likely to accrue to lenders with rigorous credit analysis and the skills to structure loan agreements that offer adequate investor protection. Given the growing importance of private debt to the economy, regulation of the sector is certain to tighten.

But with that all in mind, private credit can be an important source of returns at a finely tuned level of risk. For asset allocators, a market which previously was dominated by the banking system is now ripe for more mainstream adoption. The market is evolving to serve the financing needs of the real economy. This should give investors the choice between a highly diversified approach or specific risk return profiles that suit their own risk tolerances or market views.

Box: Private credit for all risk preferences at various stages of the economic cycle

Direct lending

is senior debt where loans are typically secured by collateral and most often feature floating rate coupons. These loans are made to support growth, acquisitions or general refinancing.

Mezzanine debt

is debt that is subordinated to the senior debt but above the equity. It will have distinct features, including warrants that allow for some participation in the performance of the company’s equity value. This is higher risk than senior debt (though there are mechanisms like Payment-In-Kind that help to reduce default risk) but should offer greater returns.

Distressed debt

encompasses loans to companies in a weaker financial or operational position. These companies may require restructuring to provide the best returns to the investor.

Venture debt

is loans to early stage growth companies with limited cashflow but high future option value.

Private asset backed financing

bilateral deals where the loan is attached to an underlying source of cash flow, such as car, aircraft and equipment leases. This real asset collateral helps to mitigate default risk. It is a private market upgrade on traditional Asset Backed Securities, which are bundled together and intermediated by banks and sold into the secondary market.