Key Takeaways

- Third-quarter earnings came in well ahead of estimates. The U.S. led the way with 82% of S&P 500® companies beating earnings expectations. Meanwhile, 65% of European and 60% of Japanese companies came in ahead of estimates.

- Margins were better than expected. Revenue growth improved, and companies passed along higher costs to their customers without destroying demand.

- Management teams are generally upbeat. In Europe, 90% of companies raised or maintained their guidance for 2022. Some of their U.S. counterparts were more guarded, with an above-average number lowering guidance.

- Supply chain disruptions should be manageable. Despite investor concerns and ongoing media coverage, most management teams expressed confidence that pressure is easing.

Strong Demand Driving Revenue Growth and Wider Margins

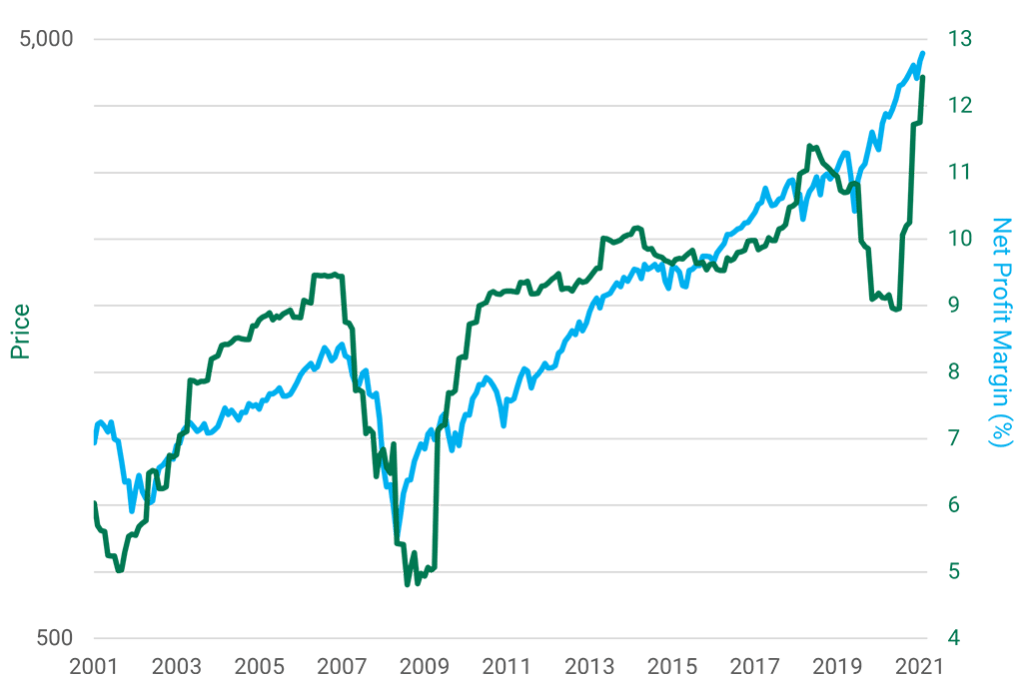

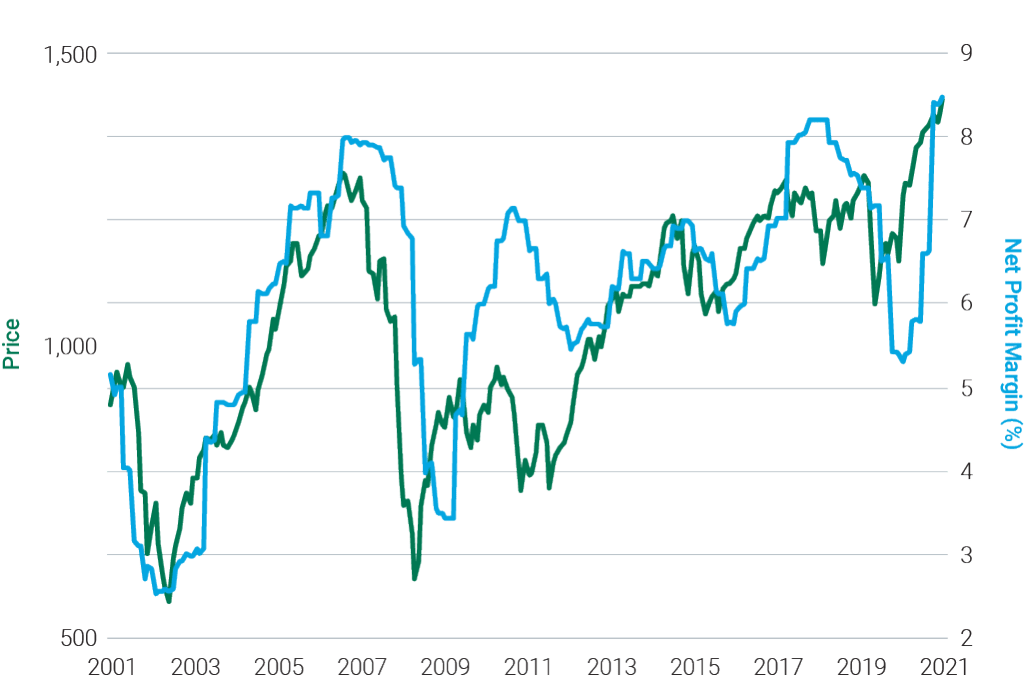

Despite concerns about inflation and rising input and labor costs, profit margins widened during the quarter. Robust demand, coupled with low inventory levels, gave companies enough pricing power to pass through rising costs without hurting sales. As shown in Figure 1, net profit margins for companies in the S&P 500 Index and the MSCI EAFE Index reached their highest levels in the last 20 years, sharply recovering from the COVID-related drop in 2020.

Figure 1 | Profit Margins Hit 20-Year Highs for U.S. and Non-U.S. Companies

S&P 500

MSCI EAFE

Data from 12/31/2001 – 11/22/2021. Source: FactSet.

Companies also reported stronger-than-expected revenue growth. Europe came close to topping a 10-year high with sales growth of nearly 30% compared to a year ago. Revenue growth was almost 18% in both the U.S. and Japan.

Management teams are optimistic about 2022 sales thanks to increased capital spending and supportive fiscal policy. Businesses also are benefiting from financially healthy consumers. Many shoppers feel flush thanks to government stimulus and more than a year of spending less on travel and other experiences outside their homes. We also saw some early holiday spending as consumers tried to get ahead of potential shortages in December.

Higher Prices Could Test Consumers’ Limits in Coming Quarters

For now, buyers seem willing to pay the going rate for most goods and services, enabling companies to pass through higher costs and maintain margins. Demand may wane in the future as consumers burn through their pandemic savings and start to push back on higher prices.

The timing of a slowdown in demand slows and an improvement in supply will significantly impact profit margins in future quarters. We could see continued improvement if demand remains strong at the same time input costs begin to decline. On the other hand, slowing demand while input costs remain elevated would hurt margins and earnings growth.

Management Teams Confident in Supply Chains

Recent earnings call transcripts confirm supply chain issues are top of mind for most management teams. About half of European companies talked about their supply chains. In the U.S., supply chain mentions were up 360% compared to the same period last year. While this has become a political football and the topic du jour in the media, most management teams expressed confidence that pressure is easing.

Macro data points also suggest supply chain conditions are improving. There has been a sharp decline in transportation costs, and commodity prices may have peaked. We’re also seeing factory production approaching full capacity in some Southeast Asia manufacturing centers as vaccination rates improve and COVID cases decline. This region is vital to many clothing and shoe manufacturers.

Trends We’re Watching

Consumer spending remains strong

Pent-up demand and high savings rates are tailwinds for consumer products and travel companies. Beneficiaries include LVMH. The Louis Vuitton and Hermes brands owner posted sales gains despite recent crackdowns in China, where it derives more than 35% of its business.

Outdoor and athletic apparel demand also is robust. Companies such as Puma and Adidas are working through supply chain challenges and have seen previously shuttered factories approach 90% capacity. While shipping delays will temporarily impact holiday sales, the management team is confident these issues are transitory.

Capital spending boosts industrial companies

Capital spending to upgrade manufacturing or move operations closer to home is positive for industrial companies. Many are seeing their backlogs grow even as they raise prices to cover higher costs. Beneficiaries include Keyence, a maker of industrial automation and inspection equipment, and Schneider Electric, a leader in the digital transformation of energy management and automation.

New product cycles and end markets spur technology spending

In Europe, more than 40% of firms have increased capital spending on projects to digitize business processes or expand capacity. Global IT services company Capgemini delivered better-than-expected earnings and reported strong order growth due to demand for digital solutions. Other examples include Japan-based IT services company Baycurrent, collaboration software company Atlassian and Infineon, the largest semiconductor supplier to the auto industry.

Transition in earnings growth leadership in the U.S.

Many companies that reported earnings losses in the third quarter last year saw positive results this quarter. This includes energy companies Phillips 66 and Exxon Mobil; travel-related businesses such as Expedia, Disney, Alaska Air and Delta; and “going out”-oriented names, including concert promoter Live Nation and casino operator MGM.

On the other hand, some companies that had strong earnings last year saw their profits decline year-over-year in this quarter. Examples include auto insurance providers Progressive and Allstate, which saw accident rates increase as people started driving more. Earnings also fell for auto manufacturers Ford and GM, “staying in”-oriented businesses like Amazon, Etsy and Discovery, and other “COVID beneficiaries” like Clorox and Sherwin-Williams.

The Outlook Remains Optimistic

Roughly 90% of European companies upgraded or maintained their earnings guidance for 2022. Their optimism stems from growing backlogs and inventory levels near historic lows. Coupled with strong demand, these conditions provide good visibility for future sales growth.

In the U.S., analysts expect earnings and revenue growth to remain strong but with year-over-year growth slowing compared to the record results of the last three quarters. While most companies remain optimistic, an above-average number of companies gave negative earnings guidance.

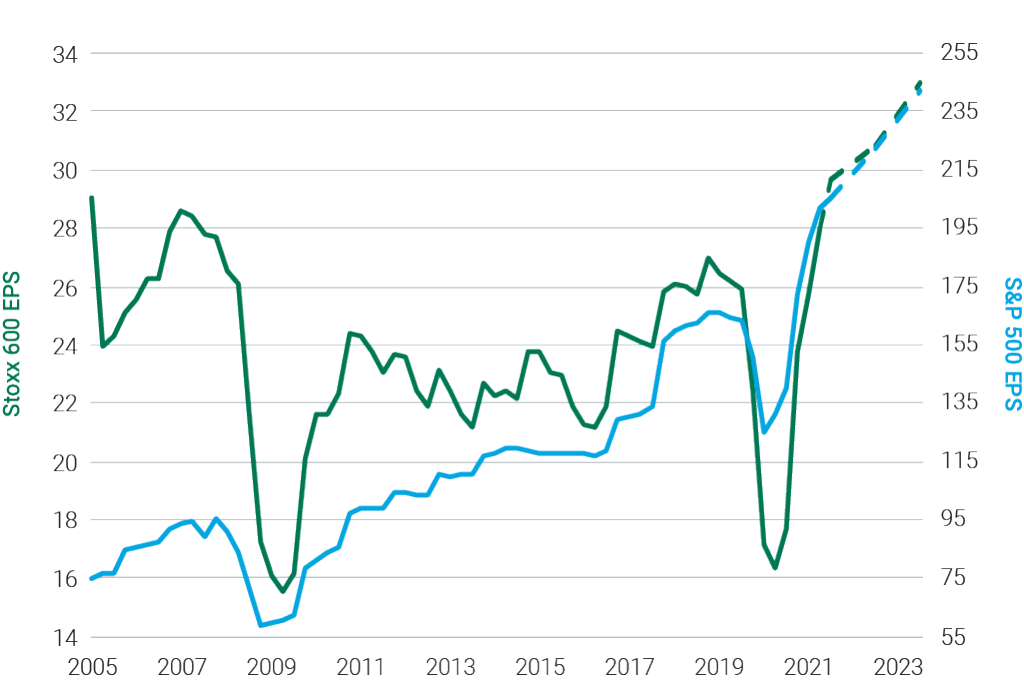

As shown in Figure 2, earnings have climbed out of a deep hole and reached pre-pandemic levels sooner than initially expected.

Figure 2 | Earnings Climb Past Pre-Pandemic Levels

Data from 6/30/2005 – 10/31/2021. Source: Bloomberg.

We Expect Investors to Become More Selective

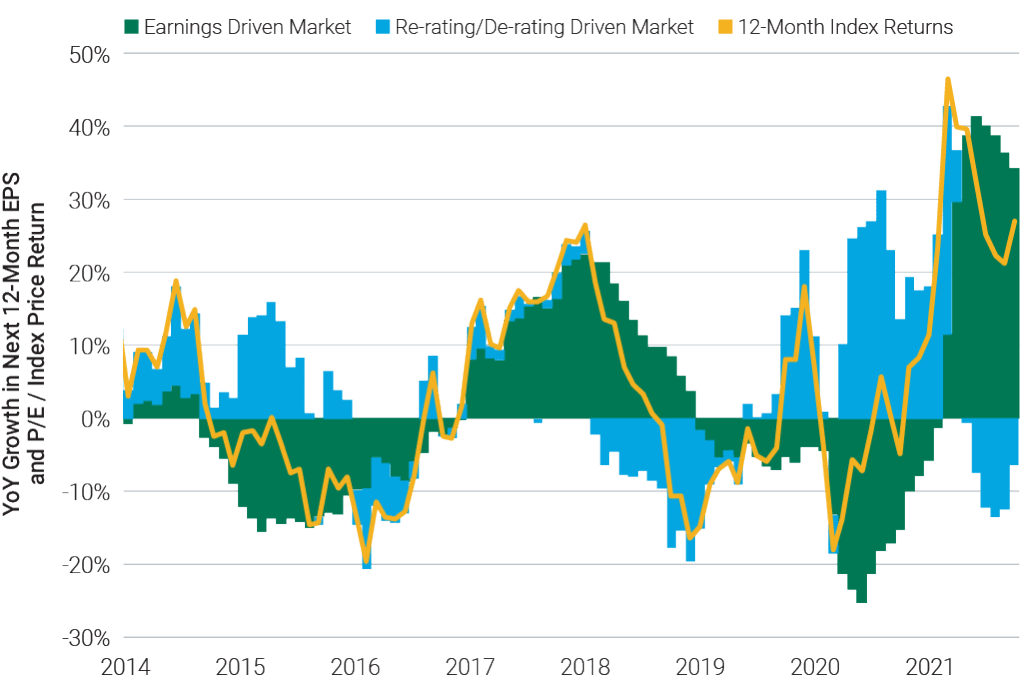

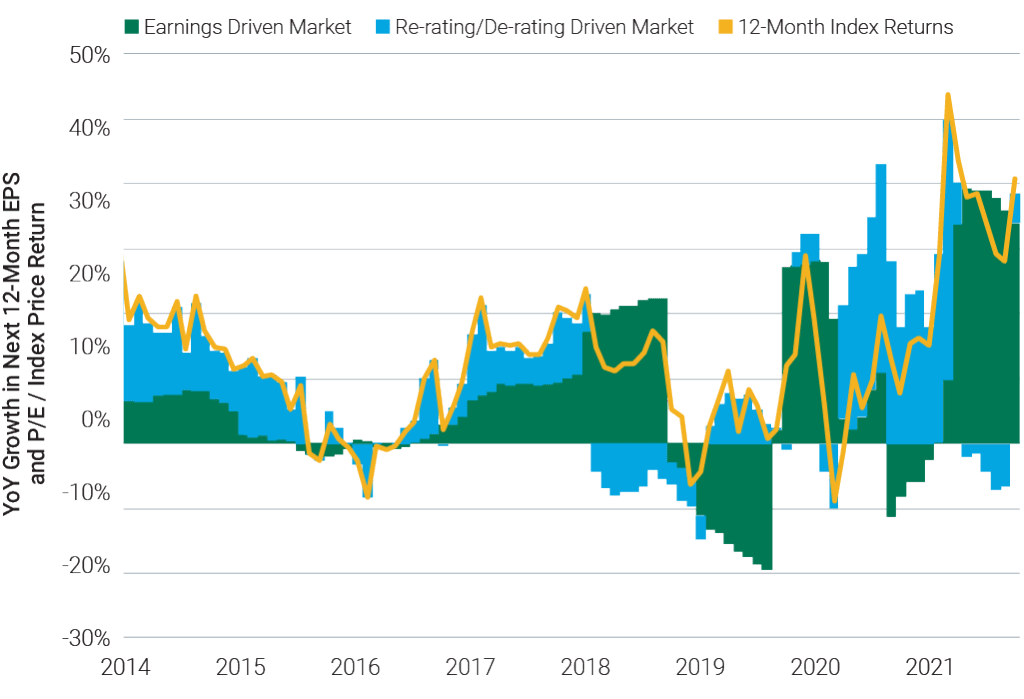

As fiscal and monetary stimulus fades, global economic data peaks and earnings growth normalizes, we believe earnings will be a primary driver of stock prices. After many years of multiple expansion supporting stock price performance, which you can see as the blue shaded areas in Figure 3, we have witnessed multiple contractions. We believe these conditions could lead to a higher dispersion of returns, creating a favorable environment for bottom-up fundamentals and security selection.

Figure 3 | Transitioning to an Earnings-Driven Market

MSCI ACWI ex-USA

Earnings-Driven Market = Year-over-year growth in next 12-month EPS, Re-rating/De-rating-Driven Market = Year-over-year growth in next 12-month P/E ratio.

Data from 12/31/2014 to 10/31/2021. Source: FactSet.

S&P 500

Earnings-Driven Market = Year-over-year growth in next 12-month EPS, Re-rating/De-rating-Driven Market = Year-over-year growth in next 12-month P/E ratio.

Data from 12/31/2008 to 10/31/2021. Source: FactSet.

We expect volatility in the new year, given the macro environment. Though earnings calls were generally upbeat, management teams are not without worries. Many are concerned about slowing economic growth in China, the potential for disruptive new COVID outbreaks, supply chain bottlenecks and inflationary pressure.