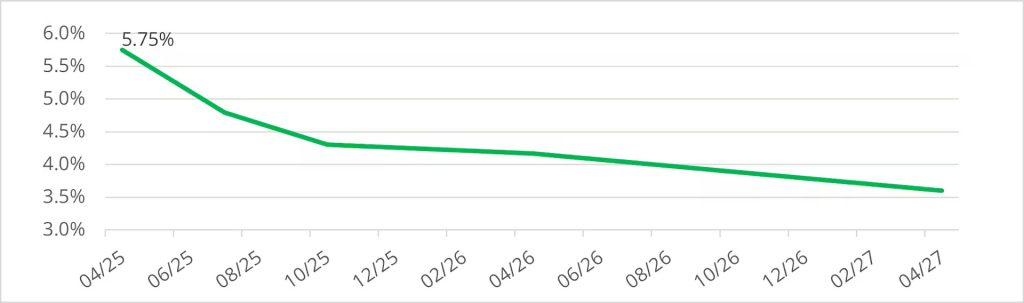

With the recent shift by the NBP towards a highly accommodative monetary policy and economic data, inflation and real wages trending downwards, we have taken a long position on Polish real rates, which are currently at 3%. Given the uncertain global context marked by the trade war, we do not believe they are sustainable at these levels and there is a chance that the curve could go even lower if there is more bearish economic data.

Poland 10-year inflation linked bond. Real rates are trading above 3%

Source: Carmignac, Bloomberg, 24/04/2025.

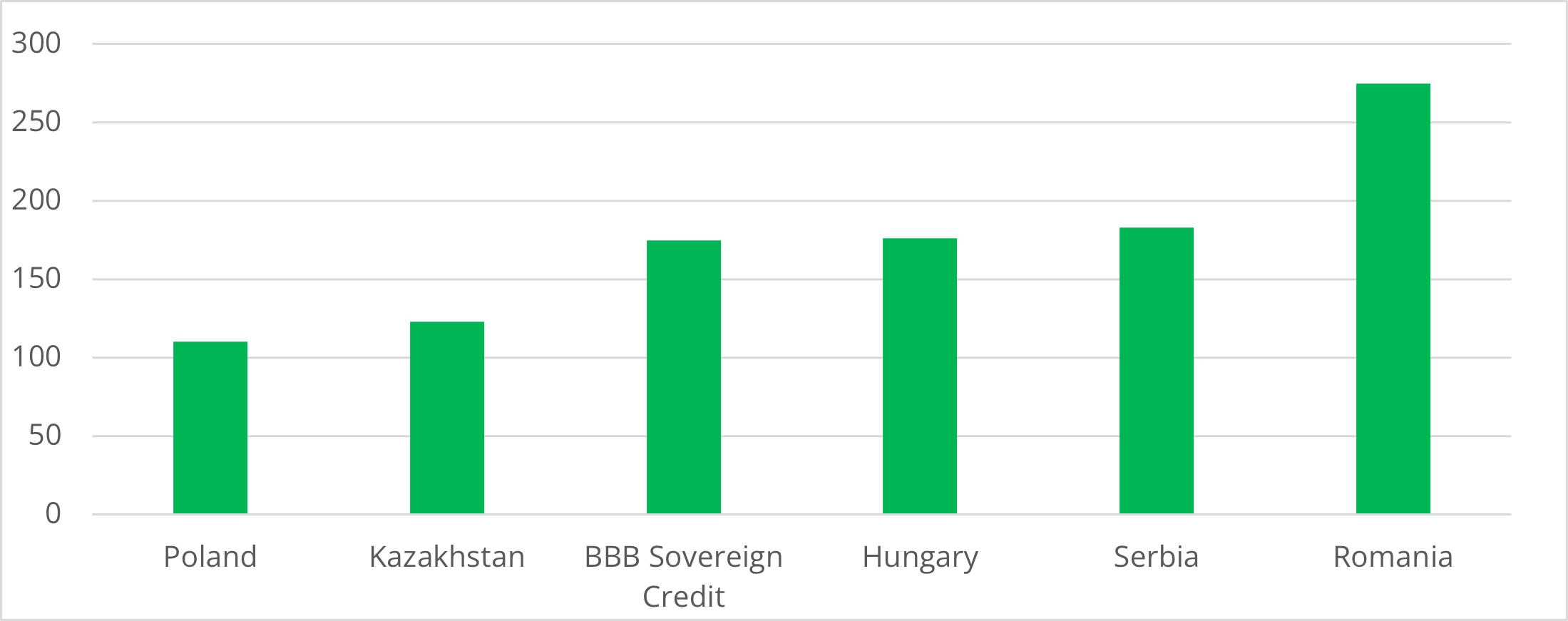

We see value in Hungarian hard currency debt where credit fundamentals continue to improve, driven by strong balance of payments dynamics and deleveraging, with a particularly notable decline in government external debt. Valuations are attractive, particularly relative to other global EM credits, and we believe spreads have yet to reflect an improvement in geopolitics.

We are also long Hungarian rates, which are offering yields close to 7% at 10-year maturities. Although the National Bank of Hungary (NBH) may consider easing monetary policy ahead of the 2026 elections, its options are constrained by high foreign exchange vulnerability and renewed underlying inflation pressures. Nevertheless, the evolving economic context might support a more dovish stance, potentially enabling some monetary easing later this year or in 2026.

Hungary sovereign spread versus eastern European peers

Source: Carmignac, Bloomberg, JP Morgan indices, 24/04/2025.

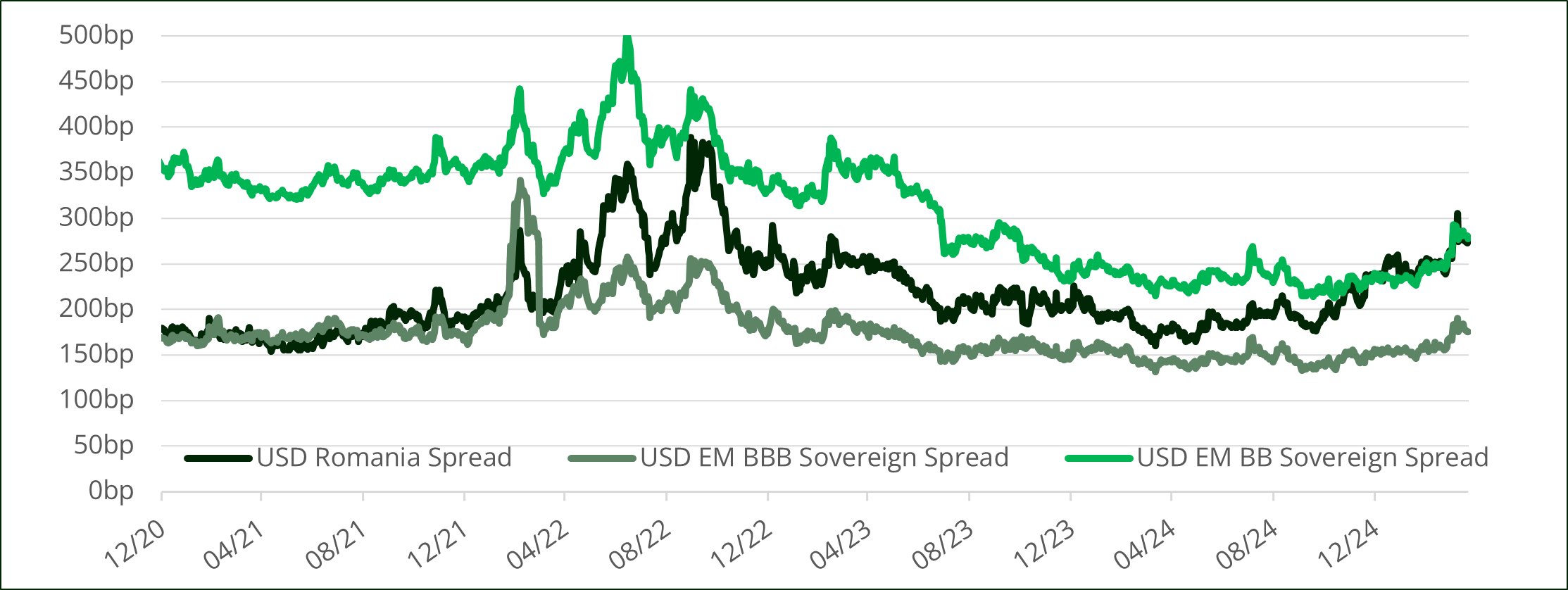

While Romanian hard currency debt has been a conviction in the portfolio in recent years, thanks to solid growth, substantial EU funds and FDI inflows and relatively low debt levels, we have sold the position given the uncertainty surrounding the elections and the lack of visibility on the candidates’ intentions for fiscal consolidation.

Today, hard currency bonds look more attractive on a valuation basis relative to peers as downgrade risks have diminished with the formation of the new coalition government. On the USD side, Romania is now trading around 100bp wide to BBB averages and flat to BB averages.

That said, we remain on the sidelines until there is more clarity on the upcoming elections due to the risks involved. However, if the grand coalition continues after the elections, we would be optimistic about the 2025 outlook and could then reposition on Romanian debt.

Romania sovereign spread versus BBB/BB. Romania now trading as a BB credit

Source: Carmignac, Bloomberg, JP Morgan indices, 24/04/2025.