Last week, there was a flurry of activity as each political party rushed to issue their manifesto ahead of the July 4th election. With some of the UK’s most pressing challenges high on the agenda – including climate change, energy security, transport, housing and digital infrastructure – infrastructure investment featured strongly among all the pledges.

Consensus views

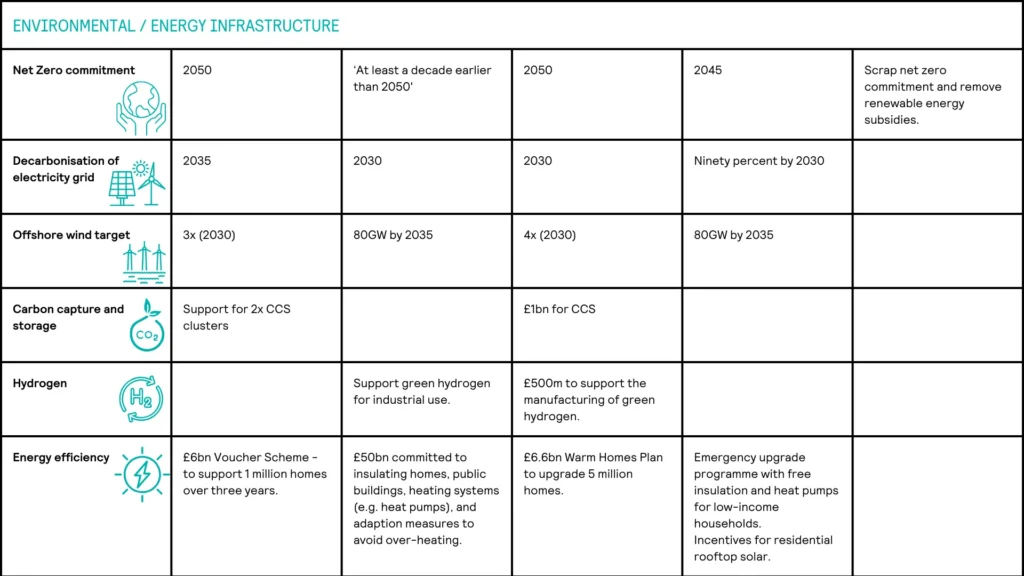

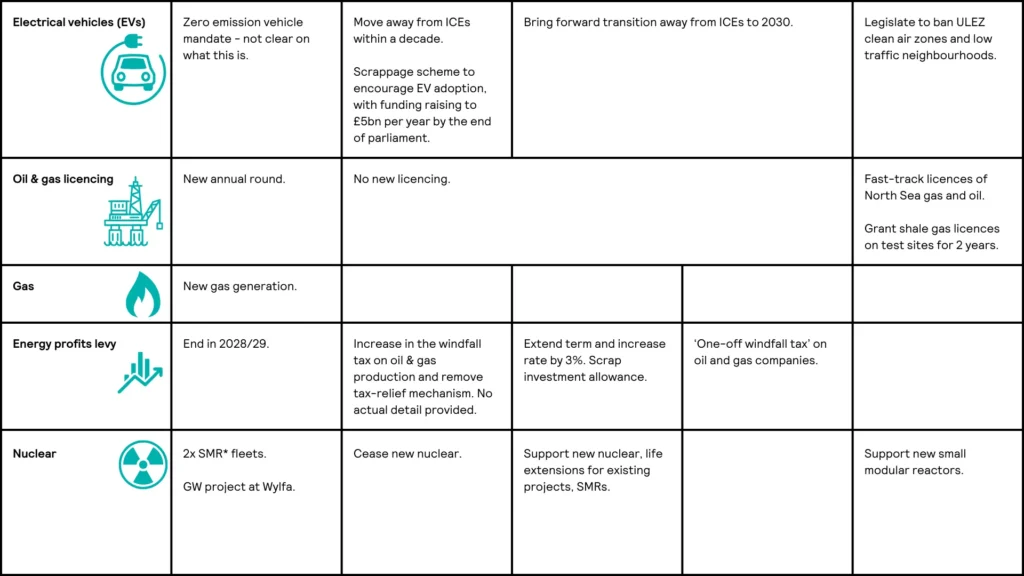

There is some consensus amongst the pledges. All parties – with the exception of Reform UK – maintain net zero commitments. The Liberal Democrats and Green Party propose bringing this forward from 2050 to 2045 and “at least a decade earlier than 2050” respectively. Labour and the Conservatives agree on carbon border tax mechanisms that would align UK carbon pricing with other countries, whilst the Liberal Democrats point to more explicit linkage between the UK Emissions Trading scheme and its European equivalent and a carbon tax. Labour and the Liberal Democrats would also reverse the current government’s recent delay of the transition to electric cars, with proposals for the move away from internal combustion engines brought forward to 2030.

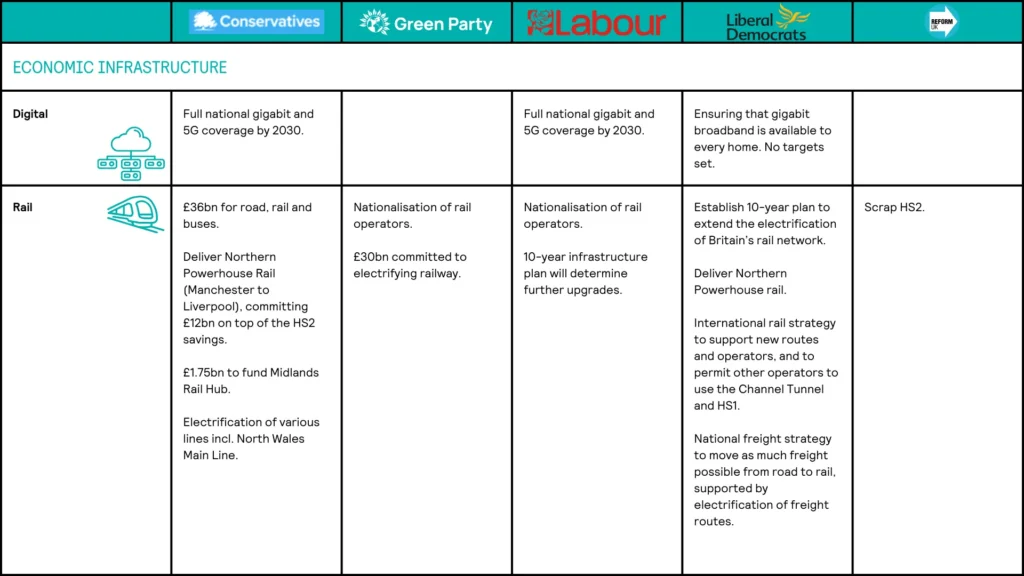

The need for new, affordable and high-quality housing and the need to reform the planning system across all infrastructure development is universal. Supporting UK jobs and bringing supply chains for infrastructure, particularly renewables, onshore is also a common objective. Finally, commitments are made by both Labour and the Conservatives to roll-out gigabit and 5G broadband nationwide by 2030.

Water sector reform is also a common topic among the political parties, with consensus that the regulator needs increased authority and the sector warrants a thorough review.

The Conservatives, Labour and Liberal Democrats are unified in proposing regulator powers to block executive bonuses where water companies have failed their environmental objectives. Labour goes further, stating it will bring “criminal charges against persistent law breakers” as well as fines. The Liberal Democrats would introduce a Sewage Tax on water company profits, and Labour are pledging to impose automatic and severe fines for wrongdoing and ensure independent monitoring of every outlet. The Conservatives will look to build on their current legislation of unlimited fines.

Divergent proposals

Dig into these headline objectives, however, and the more detailed proposals on how we achieve the headlines diverge significantly. We would also question to what extent in some cases the detailed proposals have been costed and/or what support mechanisms (capital or revenue based) would be required: in particular in respect of certain renewable deployment targets.

Labour, the Liberal Democrats and Green Party have aggressive targets to decarbonise the electricity sector: Labour and the Green Party by 2030, and the Liberal Democrats targeting 90% by 2030. This will require a significant investment but is also conditional on proposed reforms set out elsewhere to the planning system (including removing the current de-facto ban on approvals for onshore wind), reforms to wholesale markets and grid system upgrades. For example, Labour has set out targets to double onshore wind, triple solar power and quadruple offshore wind by 2030. In comparison, the Conservatives have pledged to treble offshore wind by next parliament. They have also adopted a more measured stance on the expansion of solar and onshore wind energy, aiming to safeguard rural landscapes and more explicitly point to the need to balance the green agenda with security of supply and cost of energy.

Whilst maintaining the 2050 net zero target, the Conservatives recent rhetoric of a ‘pragmatic’ transition is continued with a commitment to build new gas generation, and the intention for new annual licencing rounds for North Sea oil and gas are in conflict with Labour, the Liberal Democrat and Green Parties.

The role of nuclear is supported by all except the Green Party, with small modular reactors (“SMRs”) featuring in the Conservative and Labour proposals. The Conservatives are most specific, committing to approve two fleets of SMRs in the first 100 days, a new gigawatt plant at Wylfa, Wales, and committing to cut the approval process for new nuclear projects in half.

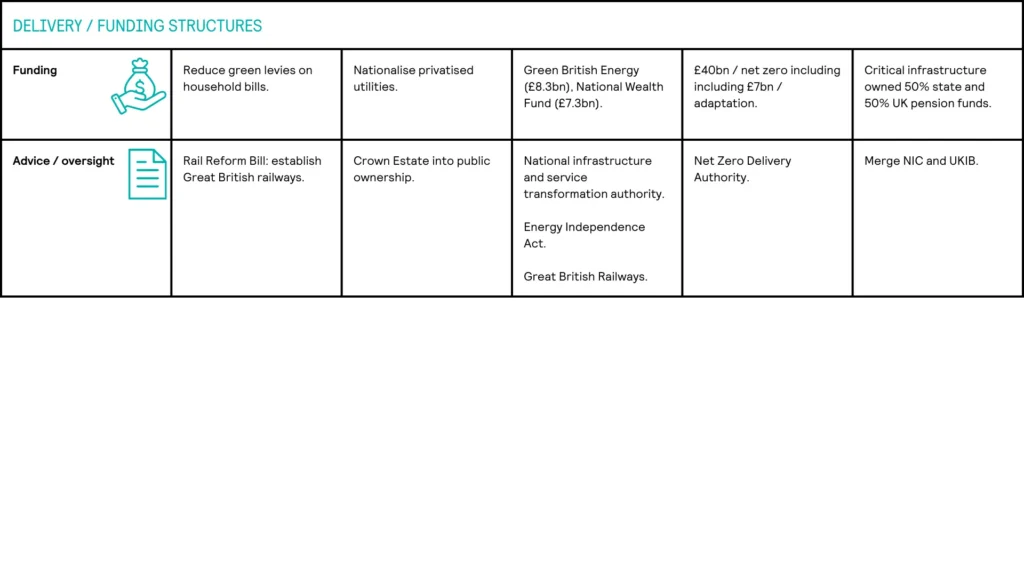

Detail on funding is not clear. Labour goes the furthest setting pledging to extend and increase the levy on profits from oil & gas companies to capitalise Great British Energy with £8.3bn and a £7.3bn National Wealth Fund and targeting ‘crowding-in’ of three times that amount. £1bn is earmarked for carbon capture and storage and £500m for green hydrogen. The conservatives have also made commitments to two carbon capture and storage clusters across North Wales and, the Northwest of England, and Teeside and the Humber. It is still not clear to us what Great British Energy will be doing. Will it essentially be a funder (Green Investment Bank mark 2? If so, what is the future role of the UK Infrastructure Bank?

Nationalisation on the cards

Nationalisation is on the cards: Labour in respect of railways, while Reform UK are proposing critical infrastructure is owned 50% by the state and 50% by UK pension funds. The Green Party propose all utilities are nationalised as well as the Crown Estate (who governs the offshore wind seabed leasing) being brought into public ownership. There is no reference, however, to the nationalisation of projects financed under the private finance initiative (“PFI”), distancing the current Labour leadership from the policies of the Corbyn administration.

Structures through which advice on infrastructure is provided to government, and the structure of public sector funding will also evolve. Labour would create a new National Infrastructure and Service Transformation Authority by bringing together existing bodies, although which bodies is not specified. We assume some combination of one of more of the National Infrastructure Commission (“NIC”), UK Infrastructure Bank (“UKIB”) and the Infrastructure and Projects Authority. Reform UK are explicit about merging the NIC and UKIB. The Liberal Democrats point to a widening of the NIC’s mandate to include environmental implications of national infrastructure decisions and would establish a Net Zero delivery authority.

Labour has also committed to develop a ten-year infrastructure strategy which will be aligned with its industrial strategy and regional development priorities and reform the planning regime to “forge ahead with new roads, railways, reservoirs, and other nationally significant infrastructure.” Though this appears to be an ambition rather than a plan currently.

There were no Labour manifesto references to the nationalisation of the water companies, but the Labour party would look to put failing water companies into special administration. It is, however, unclear what this means: will it be a similar regime to the Special Administrator Regime (SAR) for energy companies? The Conservatives have made an explicit pledge to review the (current) 5-yearly regulatory “Price Review” process. The Liberal Democrats, on the other hand, would look to transform water companies into public benefit companies and seek to introduce a single social tariff for water bills for those most vulnerable. Whilst ambitious ideas, any form of nationalisation or profit levy on these companies will need to be done in a shareholder friendly manner to ensure the UK remains attractive for business and investors, noting the large investment the sector desperately needs.

What this means for infrastructure investors

Regardless of which political party comes into power on the 4 July, the next UK government will have to deliver key infrastructure, whilst being business friendly, to support a high-growth economy. It is clear the required spending is vast over a multi-decade investment horizon, and the UK will be competing for capital against the US’s Inflation Reduction Act, the EU’s Green Deal Industrial Plan and REPowerEU.

Gravis will look to support the necessary infrastructure funding in the UK through its direct lending vehicles and open-ended funds that are invested in public securities.

Important Information

This article has been prepared by Gravis Capital Management Ltd (“Gravis”) and is for information purposes only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Any recipients of this article outside the UK should inform themselves of and observe any applicable legal or regulatory requirements in their jurisdiction and are treated as having represented that they are able to receive this article without contravention of any law or regulation in the jurisdiction in which they reside or conduct business.

This article should not be considered as a recommendation, invitation or inducement that any investor should subscribe for, dispose of or purchase any such securities or enter into any other transaction in a fund affiliated with Gravis.

No undertaking, representation, warranty or other assurance, express or implied, is made or given by or on behalf of the Investment Manager or any of their respective directors, officers, partners, employees, agents or advisers or any other person as to the accuracy or completeness of the information or opinions contained in this article and no responsibility or liability is accepted by any of them for any such information or opinions or for any errors, omissions, misstatements, negligence or otherwise. In addition, the Investment Manager does not undertake any obligation to update or to correct any inaccuracies which may become apparent. The information in this article is subject to updating, completion, revision, further verification and amendment without notice.

Past performance is no guarantee of future performance.

Gravis Capital Management Ltd is authorised and regulated by the Financial Conduct Authority; registered in England and Wales No: 10471852 and its principal place of business is 24 Savile Row, London W1S 2ES.