- Credit metrics should remain healthy through 2024, even as revenues and earnings growth are likely to slow as the macro backdrop starts to bite

- Most companies continue to enjoy fixed rate funding at significantly below market cost. Still, the average cost of debt is expected to increase with lower-rated issuers particularly exposed to the higher funding risk

- Sector breakdowns show TMT, gaming and transportation holding up well, but real estate and parts of basic industry struggling

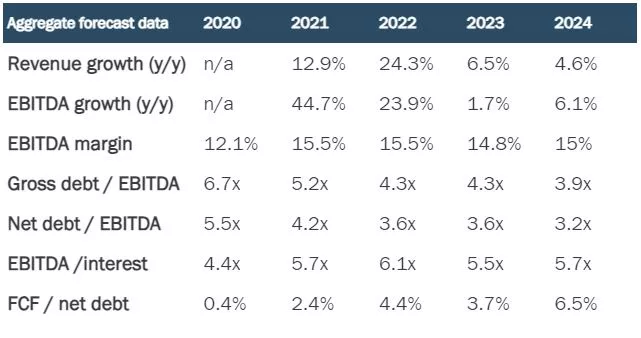

Throughout the remainder of 2023 and into 2024 we expect European High Yield (EHY) market revenues and EBITDA (earnings before interest, taxes, depreciation, and amortisation) growth to slow, as the deteriorating macro backdrop starts to impact corporate earnings. In aggregate, we forecast EBITDA growth of 1.7% in 2023 versus 23.9% growth in 2022 (Figure 1).

Figure 1: aggregate forecast data

Free cash flow (FCF) and interest coverage are expected to remain healthy through 2024, although we expect some deterioration through the remainder of 2023 due to higher funding costs. Overall, however, the impact of higher interest rates remains relatively muted given the predominantly fixed-rate or hedged structures.

We expect the average cost of debt to increase by 100bps to 4.4% from 2021 to 2024, significantly less than the circa 450bps increase in yield for the EHY market seen over the past two years.

Applying a further 300bps to our 2024 cost of debt, as a proxy for prevailing BB/B yields, would see interest coverage fall from 5.7x to 3.4x and FCF/net debt decline from 6.5% to 3.9%. Lower-rated issuers are particularly exposed to this increased cost of funding and refinancing risk remains a key area of focus.

Sector commentary

Basic industry We forecast a 17% decline in EBITDA in 2023 as higher interest rates and sustained inflation has started to impact demand in chemicals and building products. This effect is being amplified by destocking, which looks set to run into the second half of the year. The building products sector is also exposed to a deferral in “big ticket” spending, while new-build demand is down 20%-30% year-to-date.

Automotive The Covid-19 pandemic and subsequent supply-chain constraints suppressed auto sector performance from 2020-2022, notably for suppliers. For 2023 we expect around 10% EBITDA growth, despite the more challenging consumer backdrop, as production improves alongside falling commodity costs and cost restructuring. The first half of 2023 will likely prove better than the second half.

TMT The technology, media and telecom sector is expected to have a relatively stable earnings development, reflecting our view that cost inflation can ultimately be passed through via relatively modest price increases. We expect to see some timing-related margin pressure in this regard in 2023, though see positive EBITDA growth overall and stable leverage.

Gaming The sector has recovered strongly, post Covid lockdowns, and has continued to display resilience to any potential customer downturn. Mergers and acquisitions (M&A) continue to be accretive to financials with generally strong FCF supporting deleveraging, which is a focus for gaming management teams. Bond maturities tend to be longer for this sector, but recent issues have seen strong demand, mitigating a substantial step up in financing costs.

Transportation We expect airlines and rentals to have another year of above-trend growth, with continued evidence of pent-up demand, tight capacity and ongoing pricing power. However, the sustainability of this into 2024 looks increasingly challenged given the broader back-drop. We expect some normalisation in profitability into next year.

Pubs and leisure Gym memberships have shown signs of quick recovery back to pre-Covid levels, with companies also able to pass on cost inflation. This has resulted in a healthy growth in revenues and per-member yield, which have been used in bolt-on M&As in efforts to expand networks. In 2023 and 2024 we expect membership levels to moderate without causing deterioration in the overall fundamental health of the credits. Pubs and casual dining names have been the first to start showing signs of trouble as they struggle to fully pass on higher labour and produce prices to consumers with lower levels of disposable income. We expect this trend to continue, making this sub-sector the riskiest in the leisure space.

Retail We expect growing food retail revenues, largely reflective of higher input costs partially offset by weaker volumes and customers trading down. EBITDA margins slightly expanding year-on-year in 2023 reflect slightly improved gross margins and significantly lower energy costs, partially offset by continued “price investment” as sector competition remains intense. In non-food retail we expect moderate sales growth as inflation offsets weaker volumes within the context of a challenged consumer. EBITDA is expected to come down as cost pressures remain elevated.

Real estate The sector remains very challenged with valuations under pressure and a high leverage picture leading to concerns about capital structure sustainability for many issuers. Revenue is expected to decline year-on-year, reflecting a small volume of disposals in what remains a very subdued transactions market, partly offset by like-for-like rental income growth. Cash generation is expected to remain very limited as reduced capital expenditure is offset by higher interest costs. Interest coverage is also declining, although debt stacks are largely fixed rate so it will take time for the full effect of higher rates to be felt.