Key Takeaways

- We believe modest allocation changes can reduce ESG risk marginally with little compromise on return and portfolio diversification.

- Significantly reducing ESG risk through asset allocation alone may have serious diversification and return consequences.

- While asset allocation changes alone can move the ESG dial, we believe that combining sustainable asset allocation considerations and ESG-related inputs offers the greatest potential for enhanced outcomes.

Demand for environmental, social and governance (ESG)-related investments has surged in recent years. Given the very different ESG-related investments and risks inherent in the available asset classes, the best way to integrate ESG considerations into multi-asset portfolios is less clear.

How much ESG risk reduction can investors achieve through asset allocation alone? We answer that question by demonstrating the return and diversification consequences of reducing ESG risk using asset allocation. The analysis shows we can modestly reduce risk with limited asset substitution and a slight compromise on return potential.

More significant ESG risk reduction, however, requires more severe asset class substitution and return give-up. Ultimately, we conclude that the most effective way to reduce ESG risk is through a holistic approach that combines asset allocation and manager selection.

Focused on Equity Allocation

We created a model portfolio with volatility (traditional risk) comparable to a typical 60/40 balanced portfolio for this study. Our work focused only on the equity allocation, arguably the key driver of multi-asset portfolio return. The equity universe also has much broader ESG coverage than fixed income, with ratings widely available across capitalization ranges, styles and geographies.

We varied the desired ESG risk exposure and evaluated the resulting return penalty to a series of efficient portfolios. Since our goal was to show what asset allocation alone can do to mitigate ESG risk, we didn’t adjust further to account for sector allocation, geography and security selection.

Modest Allocation Changes Helped Reduce ESG Risk

We found that it is possible to reduce our equity portfolio’s ESG risk using asset allocation alone. In other words, without considering the ESG risks/benefits of any individual securities we were able to reduce our model portfolio’s ESG risk without giving up much return potential. In our example, a 10% ESG risk reduction—considered a reasonable portfolio construction goal—is achievable with a modest return give-up. However, the allocation changes aren’t inconsequential. And more significant ESG risk reduction undoubtedly requires more substantial allocation changes.

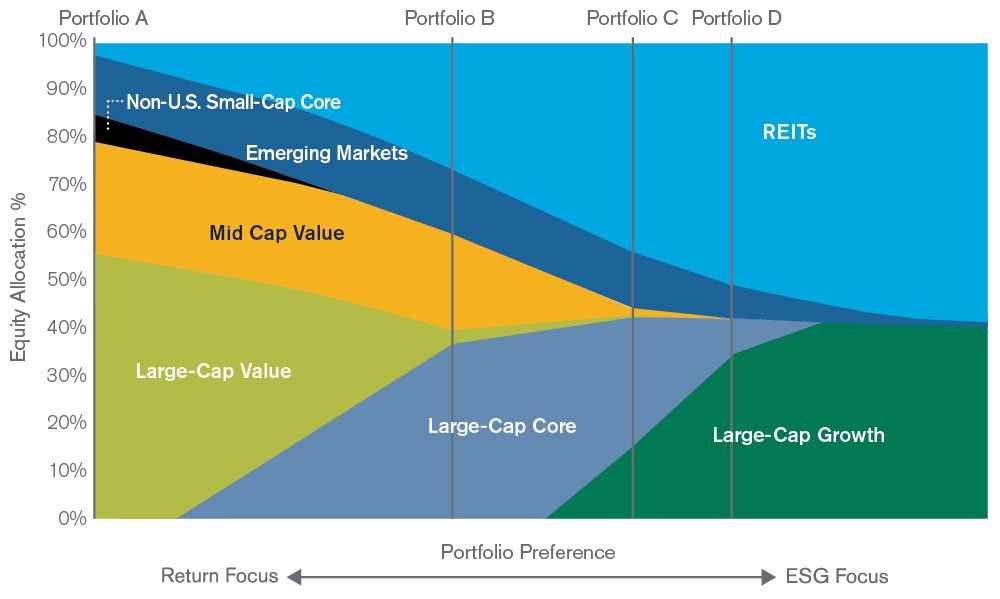

Figure 1 details these varying allocations. We see a significant preference for real estate investment trusts (REITs) over other equities and a shift from value equity into core and then growth as we ratchet down ESG risk. This reflects the more attractive ESG risk profiles of REITs and U.S. large-cap growth equities relative to value. We also see that a position in emerging markets equities (EME) is maintained until the ESG risk-reduction goal becomes quite high.

So, while EME looks unattractive in ESG terms in isolation, its return profile is compelling relative to its ESG risk. The result is that for all but the most ESG risk-averse portfolios, EME may provide an attractive trade-off for the exposure taken.

Figure 1 | Asset Allocation Can Help Fine-Tune ESG Risk for a Given Level of Volatility

Hypothetical Allocation Changes in an Equity Portfolio

Source: American Century Investments. Note: Hypothetical illustration. Results not intended to represent any actual investment strategy. Past performance is no guarantee of future results. The graphic depicts a hypothetical equity allocation in an efficient 60/40 stock/bond portfolio, created using American Century’s capital market risk and return assumptions1 and Sustainalytics ESG asset class scores2. This graphic is meant to illustrate the type and degree of changes required to reduce portfolio ESG risk using asset class substitution in the equity portion alone.

Significantly Reducing ESG Risk Required Diversification and Return Trade-Offs

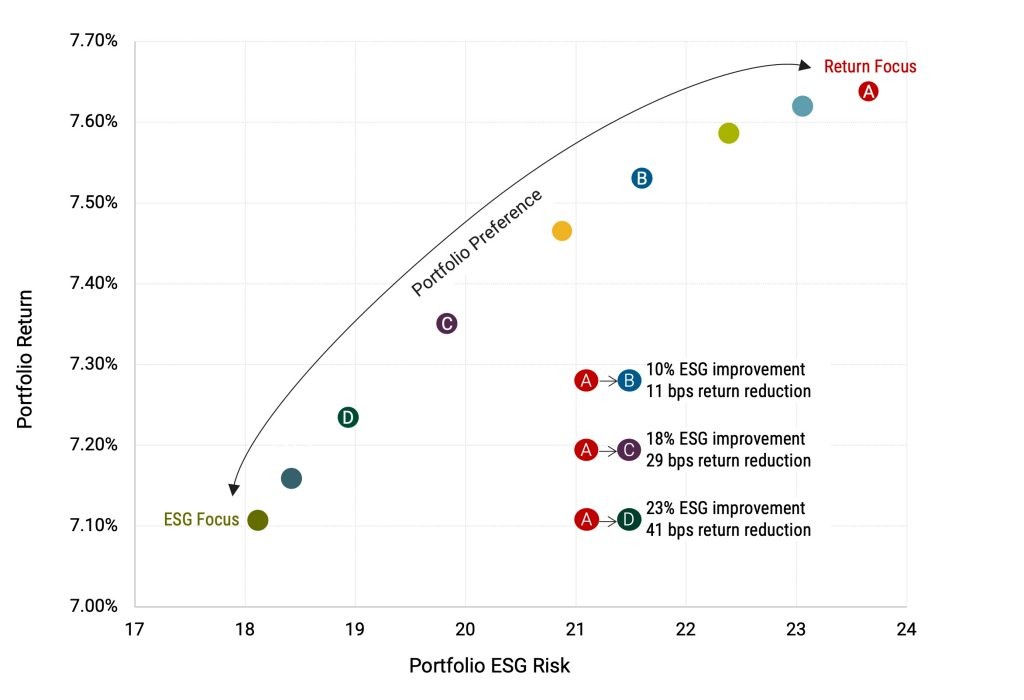

Figure 2 shows the trade-off in return versus ESG risk for a given level of volatility (standard deviation). The figure illustrates the extent to which reducing ESG risk using asset allocation strategies alone penalizes portfolio return.

Notably, the trade-off is nonlinear. Initially, a modest reduction in ESG risk allows some asset substitutions, such as introducing REITs in place of other equities, that carry little return penalty. Specifically, we see that we can realize a 10% improvement in ESG risk with relatively modest allocation changes while giving up only 11 basis points of return. This is designated Portfolio B.

However, as we seek to lower ESG risk more meaningfully, we must introduce less favorable trade-offs, such as forcing out mid-cap equity and EME. As a result, the efficient frontier in Figure 2 steepens, penalizing return at an increasing rate as we lower ESG risk (see points designated Portfolios C and D). The shape of this curve highlights the extent to which naïve attempts to reduce ESG risk through asset allocation alone may be undesirable.

Figure 2 | Reducing ESG Risk through Asset Allocation Requires a Return Trade-Off

Portfolio ESG Risk/Return Profile (Diversified Equity Portfolios, Standard Deviation Held Constant)

A Holistic Approach Is Preferable

The implication is clear—asset allocation presents opportunities to fine-tune portfolio-level ESG risk. We believe we can modestly reduce ESG risk through allocation adjustments with comparatively little return penalty. But more aggressive ESG risk reduction requires increasingly severe asset substitution and return penalties. As a result, we believe an integrated approach that includes individual security and manager selection is the best way to reduce ESG risk.