There are no facts about the future — this much is certain.

But when policy uncertainty reaches extreme levels, it can send markets tumbling and weigh on business as well as consumer and investor confidence.

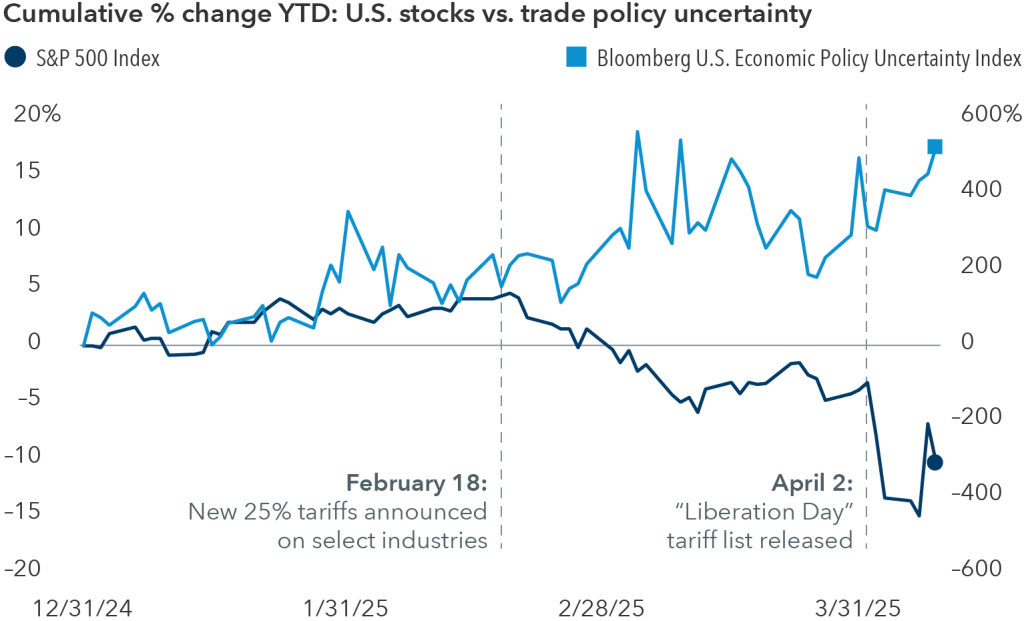

Since the Trump administration unveiled sweeping tariffs on 2 April, financial markets have swung wildly from steep declines to robust gains, often turning on the latest news headlines.

Trade uncertainty may continue to drive markets

Sources: Capital Group, Standard & Poor’s, Bloomberg Index Services Ltd. Percent change for the S&P 500 Index reflects total returns. As of 10 April 2025.

The tariffs represent the latest development in a fundamental shift away from the rules-based international order in place since the end of World War II. “This erosion of the old geopolitical order didn’t just start with the current administration. It’s been going on since at least the global financial crisis from 2007 to 2009,” says international policy advisor Tom Cooney.

What’s new is that the US, the leading defender of global free trade, is now seeking to reframe it.

In the near term, attempts to fundamentally restructure global trade, or even an extended period of uncertainty, could slow growth, boost inflation and raise the risk of a recession. Longer term, protracted uncertainty could negatively affect the reputation of the US as a reliable trade partner and security ally. On the other hand, markets could respond positively to announcements of swift and successful trade negotiations that rapidly lead to a new normal.

The wide range of potential policy outcomes presents unprecedented challenges for investors.

Night Watch sheds daylight on uncertainty

So what comes next for the global economy and markets? “When uncertainty reaches extreme levels, single-point forecasts can fall short in helping portfolio managers make good investment decisions,” says investment director Jayme Colosimo.

Enter the Night Watch, a team of Capital Group economists, political analysts and portfolio managers that explores market disruptions to help make better investment decisions.

Named after a painting by 17th century Dutch master Rembrandt, the Night Watch uses scenario analysis as a framework to explore a range of outcomes, rather than try to predict a specific result. “The goal is to gather a range of perspectives from across Capital to provide a dynamic forum for forward-looking scenarios,” adds Colosimo, “and ultimately connect these scenarios to investment implications.”

“We don’t make predictions,” says US economist Jared Franz, who chairs the Night Watch. “We try to identify a set of narratives that all plausibly construct a view of the future. We then connect investment implications to each outcome, so portfolio managers are prepared to make investment decisions as the future unfolds.”

The Night Watch has evaluated major crises including the Covid pandemic, global military conflicts and debt crises, among others. “The team looks to consider issues in advance or before they escalate and identify potential tail events in advance,” Colosimo says.

A framework for an uncertain future

This year, the group has taken on the Trump administration’s imposition of historic tariffs and shake-up of traditional security alliances. The groundwork for this analysis was launched shortly after President Trump’s election in November 2024.

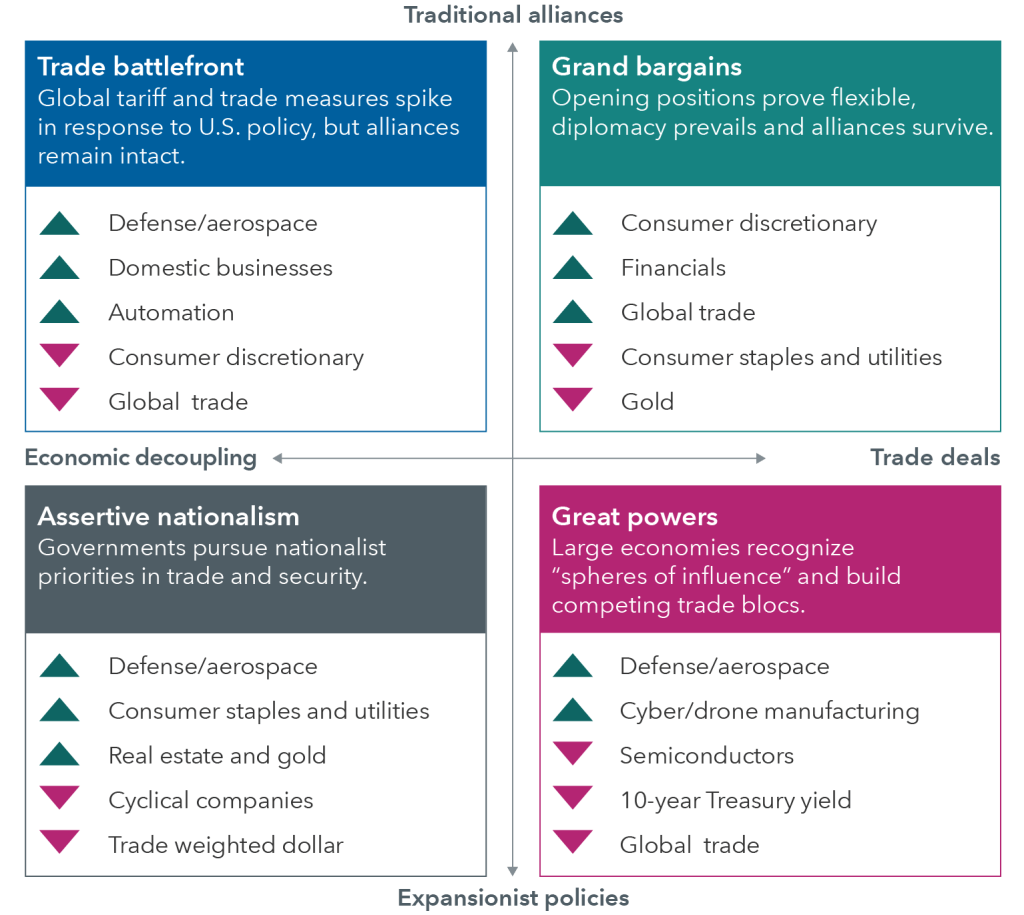

Geopolitical realignment: Potential outcomes and investment implications

The team has identified four broad potential outcomes: trade battlefront, grand trade bargains, return of global powers and assertive nationalism.

In the grand bargain scenario, traditional alliances are restored, possibly with some adjustments. Geopolitical conflicts are diminished, and political leaders strike broad trade deals. “This is the most benign scenario and generally a good environment for equity markets and the economy,” Franz says.

Isolationism, the inverse of that benign scenario, is characterised by a global trade war and increased use of hard power to address security concerns, with a tail risk potential for military clashes between major powers. “This is the worst-case scenario that combines trade wars with potential shooting wars,” Franz says.

The return of great powers would feature a mix of non-aggression pacts among the major powers, which would each dominate a regional bloc. “Think of this as going back to the age of empires, where the US, China and Russia each have individual spheres of influence,” Franz adds

Where are we today, and where are we headed?

The Night Watch team’s view is that the world has left the old order behind and recently entered the trade battlefront scenario, characterised by significant tariffs, technology export restrictions, and other protectionist measures that would accelerate economic decoupling and supply chain shifting. “This is the scenario of tough trade wars but not shooting wars, Cooney explains. “Great powers like the US and China clash in terms of technology and trade but have no wish for a military confrontation.”

If the world remains in a protracted trade struggle, economic growth will likely be more subdued, and inflation could rise, Franz says. “If these tariffs are around long term, we are likely to see slower growth beyond 2025. On the other hand, if trade deals are struck relatively quickly, then a transition to the grand bargain scenario becomes more likely.”

How long will it take for a clear picture of the new global order to take shape? Given the complexity of trade negotiations and the vast number of trading partners, investors should not expect a speedy resolution, Cooney explains. “The world is in a transition state. It took years to build the post-war order, and it could be several years before a new geopolitical order stabilises.”

“The Office of the US Trade Representative (USTR) does not have the capacity to iron out detailed agreements with some 90 countries during the 90-day pause that ends in July,” Cooney says, adding that the USTR, with a relatively small staff, has limited bandwidth to tackle many complex deals quickly. “This could be a multiyear process, especially with the largest and most complex trading relationships with economies like China and Europe.”

To calm markets, the Trump administration will want to announce a series of deals as swiftly as possible. These could be mini deals, which fall short of a full free trade agreement. During the first Trump administration, mini deals were reached with Japan, China and Brazil. It also could extend the 90-day tariff pause, though uncertainty would remain elevated and that could cause ongoing market volatility if each extension is accompanied by political brinksmanship.

“I do expect that the administration will look for some early deals with Japan and Korea, which would be easier to achieve,” Cooney says. “But renegotiating the US-Mexico-Canada Agreement is complicated, and formal negotiations haven’t started yet, so that will take some time. Similarly, negotiations with the EU will take quite a bit longer. And the US-China trade relationship, the core of this conflict, could take years and again only result in a partial trade conflict ‘ceasefire.’ Currently, there is no substantive government-to-government dialogue underway between China and the US.”

Lengthy negotiations could further weigh on markets and the economy. “The lack of certainty is one of the biggest problems here,” Cooney explains. “Companies will be reluctant to make long-term capital spending commitments without a firmer sense of the rules going forward.” Corporate spending could be depressed for an extended period.

Even after deals are struck, there is some risk that US credibility as a partner and linchpin of global trade and security could be diminished over the longer term, as could the world’s view of the dollar as a reserve currency and the perceived safety of US government debt, Cooney says.

Investment implications

For investors, the key to navigating this uncertainty is to stay humble about what’s knowable — not get anchored to a particular world view and prepare for the unexpected, believes Jody Jonsson, Vice Chair of Capital Group and an equity portfolio manager.

Jonsson seeks to strike a balance between defensive and offensive investments in her portfolio. “If there’s any favourable resolution, the markets could shoot upwards, as we saw when the announcement of a 90-day tariff pause on 9 April set off a strong market rally,” Jonsson says. “This is an important time to pay close attention to valuations and dividend income, a time when boring is beautiful.”

For example, insurance companies like Chubb do not export or import any goods, so their business would not be meaningfully impacted by tariffs. Elsewhere in financials, CME Group, which operates derivatives exchanges, has seen higher trading volumes when markets have been volatile.

“I also believe all of this strengthens the case for a globally diversified portfolio. It is tough to know when or where trade negotiations will succeed,” Jonsson explains.

Lastly, once trade negotiations begin to result in agreements, investors and companies will have some clarity, and the investing picture may brighten. “I do think that we’re probably at a point of maximum uncertainty right now,” Jonsson adds, “but eventually things will look less bad.”