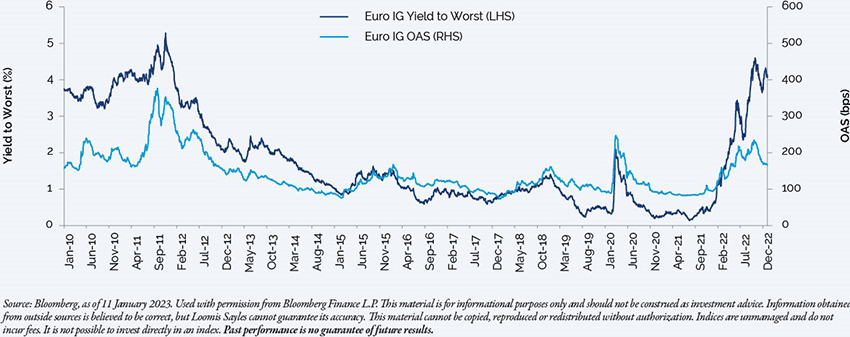

Rate volatility was a major driver of global bond markets in 2022. European investment grade bond (IG) spreads reached 10-year highs! What’s your view on current spread levels and where might they go from here?

We believe recent spread tightening will prove to be a false relief rally. The recent positive momentum encouraged market participants to deploy cash balances and invest inflows heading into year-end, with a tilt toward BBB-rated securities and new issues. Additionally, with poor liquidity in euro IG, inflows have driven spreads tighter than fundamentals would otherwise imply.

Current valuations appear attractive historically, especially when considering all-in yields. However, we have a cautious outlook and expect spread widening from current levels. We expect rates to remain volatile and economic weakness to drive fundamental credit deterioration. Combined, we believe these factors could lead to a turbulent 2023 in credit markets.

Let’s talk more about fundamentals. Why do you think they’ll deteriorate in 2023?

So far, fundamentals have remained healthy, with EBITDA up slightly across most sectors, net leverage flat and interest coverage near record levels. However, we see reasons to be cautious as we turn the page on the calendar. We expect monetary policy to exert pressure on the growth outlook in 2023, which could squeeze corporate earnings and bring a recession into sight. Additionally, we fear some of the recent earnings resilience is the result of companies offloading built-up inventory backlogs that aren’t likely to be repeated in 2023. The recent warm weather in Europe has provided energy cost relief for European corporates, but in our view will remain a significant risk and headwind through next winter.

Considering the economic backdrop, we expect negative rating migration in the coming quarters. Net rating migration and the composite PMI are strongly correlated historically. While many point to high interest coverage ratios as a strength, we expect the metric to deteriorate. Fifty percent of euro IG debt outstanding will mature by 2026.1 Assuming maturing debt is refinanced at the current index yield (~4.5%), European IG corporates would see a €10-€15 billion interest cost increase per annum.2

What are the key technicals at play in the market going into 2023?

We believe there are many factors driving a technical dislocation in spreads, notably the European Central Bank’s (ECB’s) and Bank of England’s (BOE’s) withdrawal from the markets, material outflows in 2022 that have begun to reverse, and the dislocation in swap spreads.

Euro IG spread and Yield

The ECB announced a more hawkish plan for reinvestment wind-downs in mid-December. The ECB has set a target of reducing its Asset Purchase Programme portfolio by 50%, or €15 billion of bonds on average, from March to June 2023. Given an average of €30 billion of the bonds on its balance sheet are due to mature each month, this equates to a 50% balance sheet runoff. As a result, we anticipate relatively healthy reinvestments in the Corporate Sector Purchase Programme portfolio of about €2 billion per month to start the year, but this could drop off sharply to €1-€1.5 billion from April. The ECB has yet to announce its target for the second half of the year, but the market generally expects a continued wind-down. The lower level of support from the ECB could have negative implications for the euro IG market in times of broader economic weakness.

The BOE has resumed unwinding its Corporate Bond Purchasing Scheme after halting the monetary assistance plan due to LDI-driven volatility. The BOE is expected to sell a minimum of £200 million per week but has been running its sales well above that, at an average of £475 million for active weeks.3 The BOE now holds £9.75 billion in corporate bonds that it aims to sell by early 2024 at the latest,4 which implies a slowing of the current pace of sales. We believe a slower pace could be viewed as a relative positive for the corporate bond market, though it could still weigh on spreads in weak periods especially if front-loaded.

The euro IG market reached a peak of €17.7 billion in outflows in 2022.5 However, fund flows have rebounded with consistently positive inflows in mutual funds and ETFs since early November. This is partly due to higher all-in yields providing support to absolute returns for the year. The UK IG market also experienced outflows, particularly after former Prime Minister Liz Truss’ mini-budget triggered volatility that led to stress and cash needs for LDI investors. While the UK market has stabilized, inflows back into the asset class have remained muted.

Lastly, we believe the ECB’s unwind of quantitative easing (QE) could ease stress in the swap spread6 market, which in turn could make valuations look more attractive on a Z-spread basis. Z-spreads are the primary measure of credit risk used in European markets and reflect the difference between IG market yields and swap rates. ECB buying has limited sovereign supply and, among other technicals, driven swap spreads near historically wide levels. As a result, Z-spread valuations have narrowed and appear less attractive. We expect sovereign issuance to pick up in 2023 as the ECB unwinds QE and EU countries increase issuance to fund support packages. We believe increased sovereign supply could relieve the dislocation in the swap spread market, becoming a positive tailwind for credit valuations as Z-spreads normalize. However, we caution that higher sovereign supply could lead to lower demand for corporates.

1 Bank of America, 22 November 2022.

2 Bank of America, 22 November 2022.

3 Citigroup, 6 January 2023. Because of the holiday period, there were numerous weeks when the Bank of England was not selling. Active weeks refers to the weeks when the bank was actively selling.

4 Bank of England, 16 December 2022.

5 JP Morgan, 2 December 2022.

6 Swap spreads are the difference between the fixed component of a given swap (which is a contract to exchange fixed interest payments for floating-rate payments) and the yield on a sovereign debt security with similar maturity.

Loomis, Sayles & Company, L.P.

A subsidiary of Natixis Investment Managers

Investment adviser registered with the U.S. Securities and Exchange Commission (IARD No. 105377)

One Financial Center,

Boston, MA 02111, USA

www.loomissayles.com

This communication is for information only and is intended for investment service providers or other Professional Clients. The analyses and opinions referenced herein represent the subjective views of the author as referenced unless stated otherwise and are subject to change. There can be no assurance that developments will transpire as may be forecasted in this material.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization.

Copyright © 2023 Natixis Investment Managers S.A. – All rights reserved