ASEAN has many structural advantages that offer investment opportunities for both growth and value investors. As the post COVID recovery gains momentum in the region, active investors seeking differentiated ideas can add alpha to their portfolios by tapping the diverse ASEAN markets.

ASEAN in general had avoided the full brunt of the pandemic in 2020 by closing borders early and restricting mobility. Hopes of a nascent recovery seen in late 2020 and early 2021 were quickly squashed when waves of a more contagious COVID variant swept through the region at a time when vaccination rates were still not at optimal levels. ASEAN economies were hit hard by renewed lockdowns, disrupting both consumption and manufacturing.

The worst appears to be over with COVID cases on the decline. Despite the challenging environment, the MSCI AC Asean index posted a flat performance of 0.21% in 2021. In comparison, the MSCI AC Asia ex Japan index declined by over 4%.1 As the recovery takes hold, investor interest is likely to be renewed especially since the region offers both growth and value investors diverse opportunities.

A growth boost from foreign direct investments

The reconfiguration of global value chains (GVCs) following the onset of the pandemic presented a great opportunity for ASEAN economies to upgrade their participation in GVCs. Typically, the decision to relocate GVCs will depend on factors such as labour costs, skilled labour access, infrastructure quality, and information communication technology development to name a few. The positive news is that ASEAN economies stack up relatively well on a number of these areas compared to other regions.

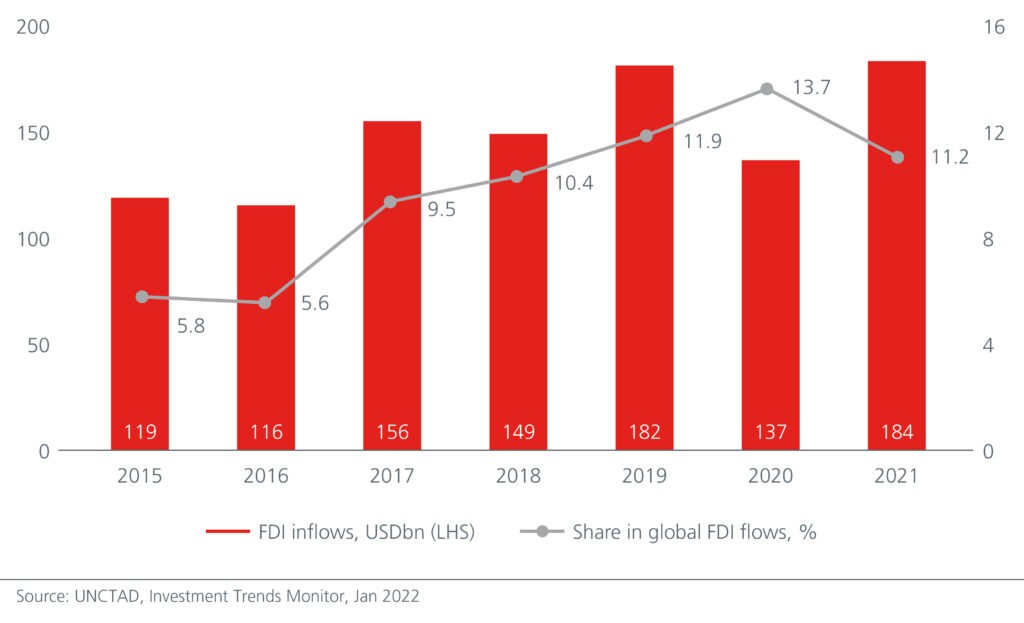

This is likely why the region was one of the top beneficiaries of global foreign direct investments (FDIs) in 2021; the total inflows rose by 35% year-on-year to USD184bn and even exceeded the 2019 pre pandemic figure of USD181bn.2 See Fig. 1. Moreover, the increases were seen across most member states.

Fig 1: FDIs are on the rise in ASEAN

Another factor underpinning the FDIs is the Regional Comprehensive Economic Partnership (RCEP). The RCEP is important as it unifies existing free trade agreements (FTA) between ASEAN and existing partners and will be the world’s largest FTA measured by GDP. RCEP increases ASEAN’s attractiveness for FDIs, relocation of value chain activities and production facilities. It is an opportunity for companies to have access to a single market of 600 million consumers. As more multinationals seek to diversify their operations, ASEAN should benefit from higher FDIs.

Investment implications: The bulk of ASEAN FDIs go to the manufacturing sectors. Countries such as Thailand, Malaysia and Vietnam are likely to benefit from the reconfiguration of GVCs, given the younger population and workforce. The region’s minimum wage levels are also an attraction to companies setting up manufacturing facilities. Separately, Indonesia is attractive for its natural resources. As geopolitical tensions intensify, the ASEAN investment is seen as more appealing given its exposure to commodities and the diversity of ASEAN markets.

ASEAN is expected to enjoy an investment revival after a two-year COVID-induced delay. Indonesia, Thailand, and Malaysia are standouts for FDIs. Meanwhile Philippines is expected to start relaxing some of Asia’s toughest foreign investment restrictions. Singapore should also benefit given its “flow-through” hub status. Within these ASEAN countries, we believe the commodity, tech and auto sectors are best positioned to reap benefits.

Infrastructure building at the forefront

The pandemic brought to fore the urgent infrastructure gaps in many ASEAN countries, forcing governments to identify healthcare, telecommunications, transportation, logistics and education as key focus areas in addition to basic services such as water and sanitation. From Indonesia to the Philippines and Vietnam, both hard and soft infrastructure is being given a big push.

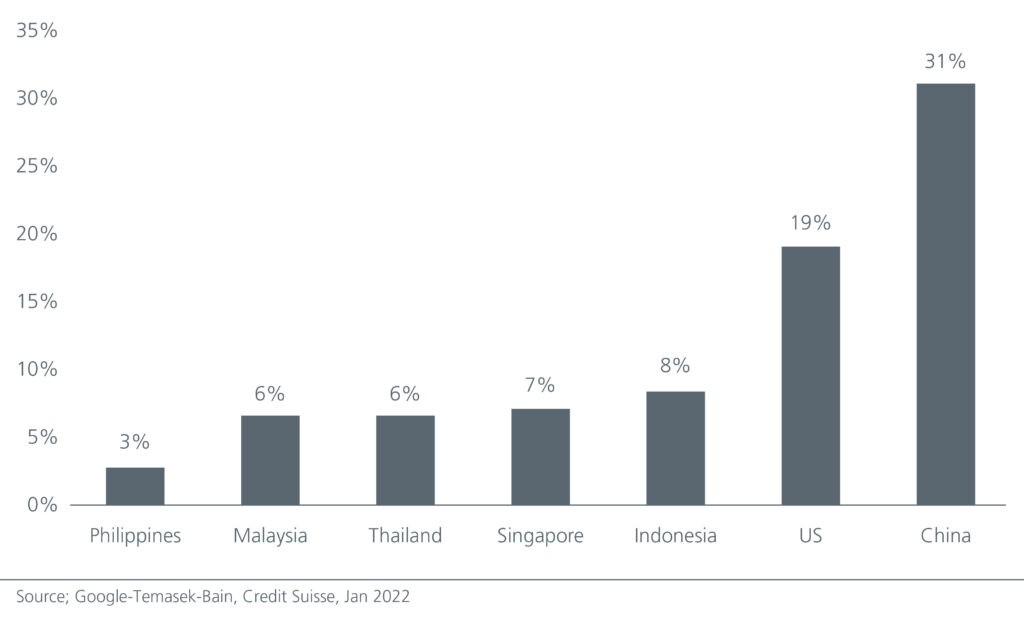

While hard infrastructure tends to be undertaken by the public sector, soft infrastructure is an opportunity for the private sector companies to play a huge role. ASEAN governments have come to recognise the importance of building a digital economy as key to overcoming inequality. Digitalisation presents investment opportunities in many areas such as education, fintech, e-commerce, healthcare, logistics, etc. The disruption caused by these new technologies and the current low penetration rates for e-commerce and fintech represent the future growth areas. See Fig. 2.

Fig 2: E-commerce penetration in ASEAN remains low

Furthermore, for ASEAN economies to reap the full benefits of the reshoring of supply chains, a key consideration is the availability of excellent hard and soft infrastructure. Strengthening the physical infrastructure, such as improving the efficiency of transportation links coupled with smart logistics and supply chain networks, should ease significant disruption to the supply chain. Ultimately, infrastructure development offers a long-term positive multiplier effect on growth and jobs.

Investment implications: We are seeing investment opportunities in Indonesia and Singapore. Currently, the new economy sectors remain under-represented in ASEAN, but they are emerging as a new strength. New listings in Singapore and Indonesia are adding breadth and diversity to ASEAN growth.

The parallel push for sustainability

The “greening” of ASEAN will be another growth area. The rapid urbanisation and development of the region’s mega-cities have significant environmental consequences. Currently around 50% of ASEAN’s 600+ million live in urban areas, with another 100 million more expected in the next 15 years; carbon emissions and waste generation are on the rise.

Given that ASEAN cities are amongst the world’s most vulnerable to the impact of climate change, sustainable urbanisation should be a top priority. The European Union has pledged EUR 5.1 million from 2021-2025 to help with the Smart Green ASEAN Cities programme, focussing on green and smart solutions through digitalisation and the use of technologies.

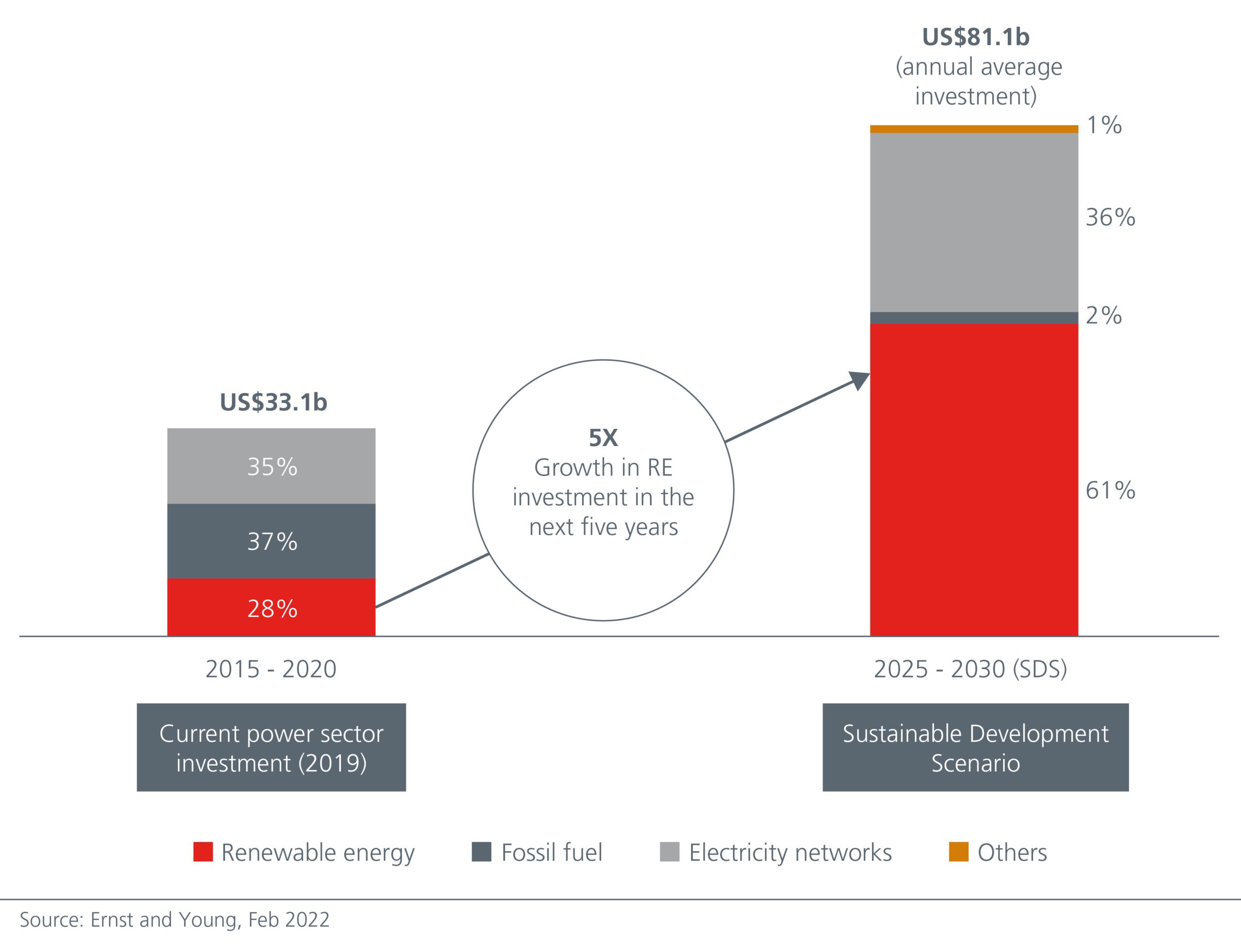

Investment implications: This focus on sustainability is set to create significant opportunities in certain sectors, in particular energy transition and renewable energies for manufacturing, construction and installation and transport and buildings. See Fig. 3. Moreover, this green push will also create new green jobs with the International Labour Organisation estimating 14 million net jobs to be created in ASEAN by 2030.

Fig 3. ASEAN’s renewable investments set to increase

Key challenges to navigate

In our previous article, we discussed how ASEAN’s post pandemic future will be shaped by greater regional trade and integration, shifts in global manufacturing supply chains and acceleration in digitalisation. Nonetheless there are challenges that need to be addressed.

A prolonged Ukraine-Russia crisis will see inflation rise across the board. The impact on individual countries will not be even; Philippines and Thailand are more sensitive to higher oil prices, while energy and commodity exporters such as Indonesia and Malaysia will have some buffer. Nonetheless the rise in inflation rate may not necessarily lead Asian central banks on a more hawkish monetary policy path (unlike the US Federal Reserve) than previously anticipated, especially as there remain significant output gaps in several Asian countries. In any case, bank stocks tend to do well in a rising rate environment and bank weightings in ASEAN’s indices remain much higher than in other parts of Asia Pacific.

Another area of concern is the economic scarring from COVID and the resultant loss of output. While the region is on the recovery path, the quality of growth is different given that the varied nature of the economies. Hence recovery will not be even across the region. Still, it should not be too long for investors to notice the region’s structural strengths i.e., demographic dividend, low digital and credit penetration, and attractive valuations. As geopolitical tensions rise, ASEAN becomes a more appealing story. Investors seeking differentiated ideas should pay attention to the increasingly overlooked diversity of ASEAN markets.

This is the third of a series of eight articles which examines the different investment strategies investors can adopt to tap on the opportunities that are emerging in Asia.