India’s monetary and fiscal policies are coming together to support India’s economic recovery, while digitalisation is driving transformational growth across multiple sectors. We see opportunities in both new and old economy sectors and note that investors have historically been well rewarded for investing in India’s less obvious, off-benchmark stocks.

In 2021, the Indian Sensex outperformed the MSCI Asia ex Japan Index by rising 20.8% in USD terms. Although large inflows from domestic retail investors and a number of high-profile listings of new economy companies played a part in propelling the market higher last year, we believe that there are both near and longer-term factors that make the Indian market attractive for investors as the Indian economy regains its growth mojo.

Fastest growing economy within EM

India is expected to be the fastest growing economy within the Emerging Markets in 2022 and 2023. It is forecasted to grow 9% in FY2022, repeating last year’s feat1. Many of the high frequency indicators which we track, such as power demand, rail freight and tax collection were already within their top 10th percentile readings in the last few months of 2021. The step up in India’s vaccination rate has also boosted mobility and consumption. 57.1% of India’s population is fully vaccinated with 70% having received at least one dose of the vaccine2. The higher vaccination rate and a better prepared healthcare system can potentially provide some buffer against newer strains of the COVID-19 virus.

The World Economic Forum recently raised India’s growth prospects for FY2023 to 7.1%, expecting the financial sector’s stronger performance to lift credit growth, investment and consumption3. Indeed, in the recent earnings results conference calls, bank management highlighted pent up credit demand across all segments and appeared to be more confident over the outlook for their asset quality.

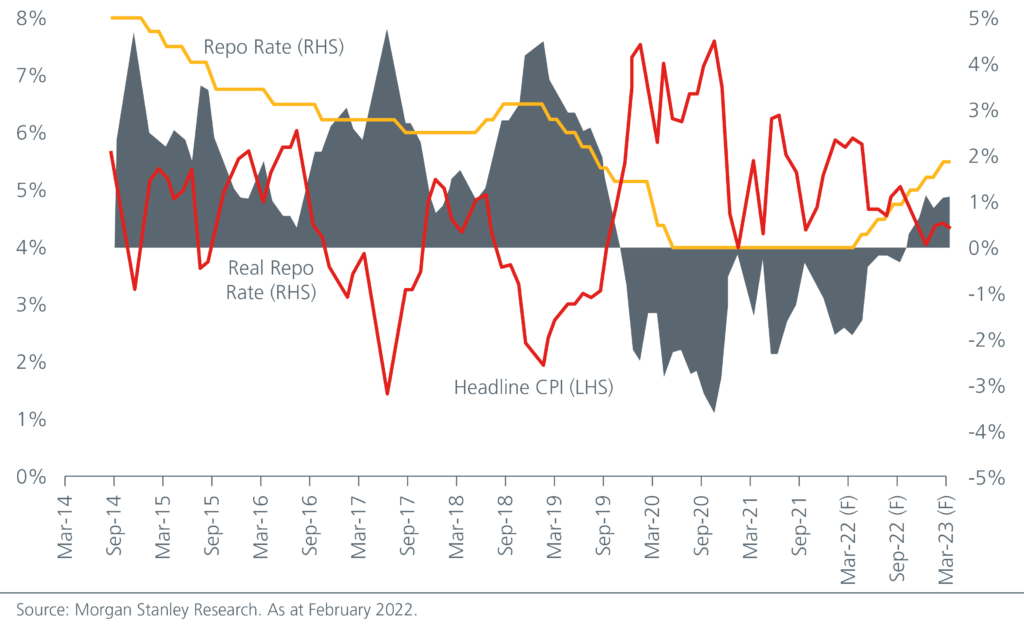

Consumer price inflation rose to 6.1% in February 2022, slightly exceeding the central bank’s target band of 4 to 6%. Nevertheless, any rate hikes are likely to be calibrated and in line with India’s economic recovery. With the gradual increase in nominal rates, real rates should remain negative until the third quarter of 2022, which should be positive for risk assets. See Fig. 1. That said, persistently high oil prices emerging from the developments in Russia/Ukraine could pose a risk to India’s inflation outlook. For now, India’s record foreign exchange reserves at 22% of GDP offer the central bank some flexibility in managing currency volatility. If Indian government bonds get added to global bond indexes this year, the ensuing inflows should also help support the rupee.

Fig 1. Real rates in India are expected to remain negative until 3Q22

On the fiscal front, India’s 2022 budget reaffirmed a capex-led growth push. Capex is expected to rise 35% from the previous year and account for 26% of the budget in FY22, up from 23%. Spending on infrastructure, domestic manufacturing, Environmental, Social and Governance (ESG) initiatives as well as digitalisation would be key.

Digitalisation to transform India’s growth

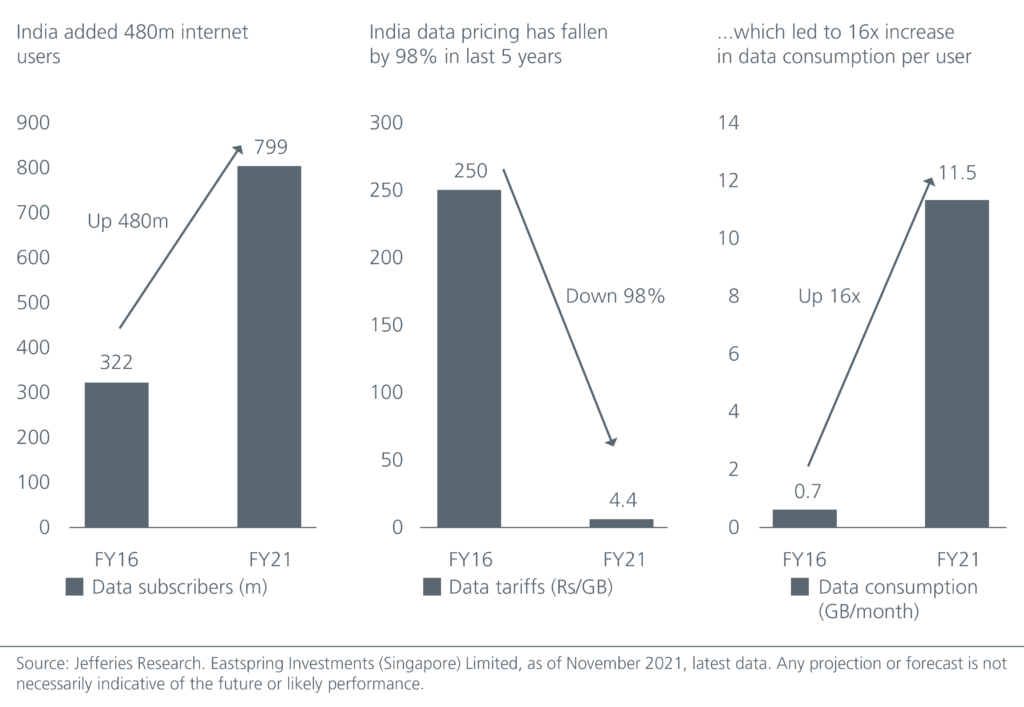

Digitalisation will be an important growth and earnings driver going forward. In the last five years, India added 480 m internet users. Over the same period, data pricing fell by 98%, resulting in a 16-fold increase in data consumption per user. See Fig. 2. The pandemic has also accelerated the adoption of digital channels in many sectors. Digitalisation will bring about productivity gains, supporting economic growth. It will allow companies for example to expand their distribution networks in tier 3 cities quickly and with lower costs. This can in turn lead to higher revenues and better margins. Ongoing digitalisation also enables new sectors such as ed-tech, fintech, e-commerce, creating more jobs. At the same time, with digitalisation, the government should see a more efficient execution of social schemes, and hence less leakages.

Fig 2. Digitalisation to drive new business models

With coal accounting for 70% of the country’s electricity source, the Indian government has been ramping up its investment in renewable energy. The recent budget introduced measures to encourage electric vehicle adoption and to reduce fuel pollution. Favourable policy, the private sector’s increasing focus on ESG and growing price competitiveness are expected to drive India’s solar module manufacturing capacity by 400%, from 8GW as of March 2021 to as high as 43GW by the end of FY2025. We see investment opportunities in renewables as well as in companies seeking to improve their sustainability practices.

Meanwhile, to encourage local manufacturing, the government is also phasing out concessional import duties in the capital goods sector. This should add impetus to the “Made in India” theme – we have already seen India’s exports and capacity utilisation rise across many sectors over the course of the pandemic as global companies seek to diversify their supply chains. India’s share of global exports has risen to an all-time high, although at 1.9%4, there is still significant room for market share gains especially in electronics and speciality chemicals. A pickup in exports would create much needed jobs and boost economic growth. That said, India’s current low share of global exports and its more domestically driven economy potentially offer the Indian economy some added resilience at a time when the outlook for global growth appears uncertain.

Meanwhile, the government’s ambitious programme to monetise USD81 bn of state assets appear to be gaining traction. The realised proceeds will help ease fiscal constraints and free up funds for more infrastructure investment.

Significant room for stock pickers to add alpha

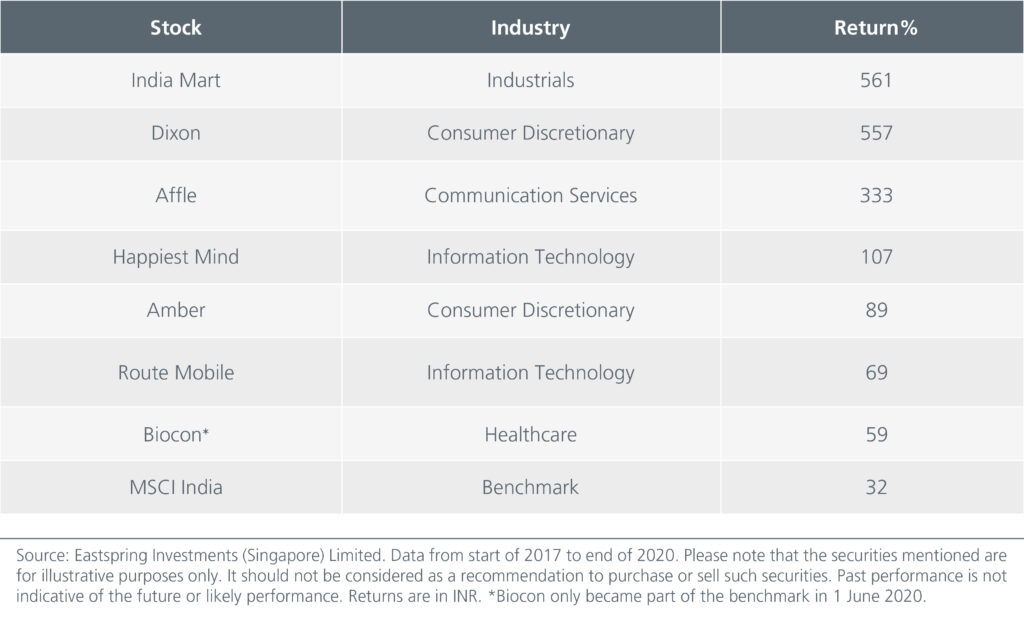

We had highlighted previously that India is one of the most diversified equity markets in Asia, with sizeable sectors that derive revenues from both within and outside of India. This provides significant opportunities for stock pickers to add alpha and is also one of the compelling reasons for investors to have an exposure to Indian equities in their portfolios. For investors who can go off the beaten track, non-benchmark stocks can offer significant outperformance. Fig. 3

Fig. 3. Performance of selected off-benchmark stocks in India (2017 – 2020)

Admittedly, India’s valuations are not cheap, but a strong earnings recovery could potentially provide some offset. We expect earnings to rebound from a low base, after being weighed down by multiple one-off events in the last seven years. These include the demonetisation program in 2016, the passing of the GST bill in 2017 and the collapse of a large non-bank financial company in 2018 which subsequently led to heightened risk aversion across the sector.

Going forward, we see opportunities in multiple sectors as digitalisation drives new business models. The information technology sector is also a big beneficiary as it is an enabler of this transformation, not just in India but globally. At the same time, there are opportunities in the old economy sectors such as real estate. With the housing affordability ratio at its lowest in 14 years, home purchases have never been so accessible. A recovery in the real estate sector can have a multiplier effect – on banks’ asset quality and their ability to lend, on consumption from the positive wealth effect, as well as on related industries including construction and cement.

This is the first of a series of eight articles which examines the different investment strategies investors can adopt to tap on the opportunities that are emerging in Asia.