The International Monetary Fund (IMF) recently released its latest World Economic Outlook (WEO).* Its projections for global GDP growth are broadly unchanged relative to the April WEO and July WEO update but the risks to the outlook have become more balanced. In this Macro Flash Note, Economist Sam Jochim summarises.

IMF growth forecasts

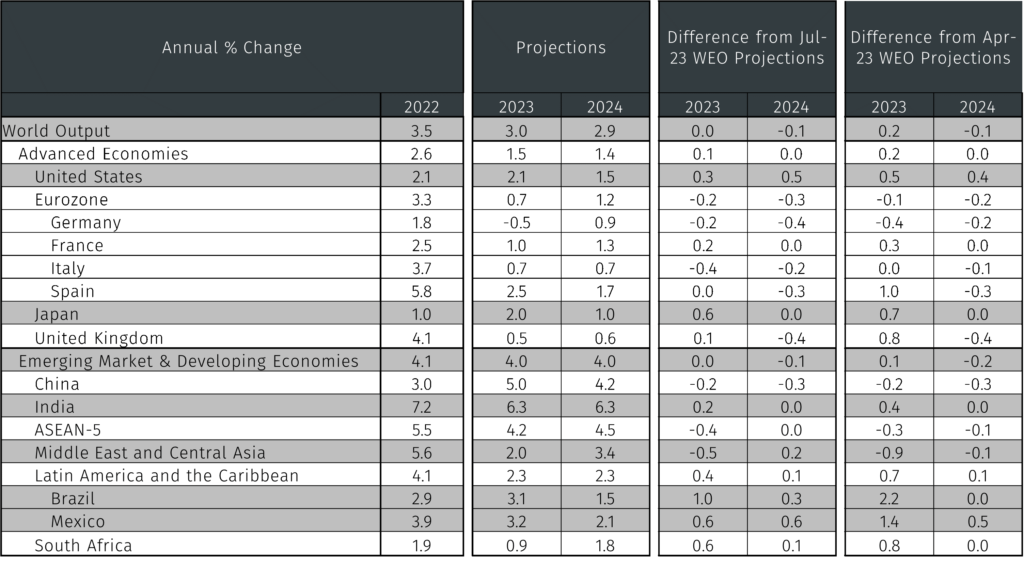

The IMF forecasts global GDP growth of 3.0% and 2.9% respectively in 2023 and 2024 (see Table 1). This is broadly in line with its previous forecasts made in July and April.1 The headline numbers for advanced and emerging market (EM) economies have moved little from their previous forecasts, yet these hide diverging growth paths across economies within the two groupings.

Table 1. IMF’s World Economic Outlook GDP growth projections (% year-on-year change)

Source: IMF. Data as at 10 October 2023.

Within advanced economies, US GDP growth has been revised up and in 2023 it is now expected to be 2.1%, the same as in 2022, before slowing to 1.5% in 2024. This reflects resilient private consumption and a tight labour market. Notably, the IMF sees the US unemployment rate peaking at 4.0% in Q4 2024, just 0.2 percentage points above its current level and 1.2 percentage points below the April WEO projection. Contrasting this is the IMF’s forecasts for the eurozone, which is now predicted to see a more significant slowdown in 2023 and a smaller rebound in 2024 – largely reflecting weaker growth in Germany due to weakness in interest rate sensitive sectors and slower foreign demand.

In EM economies, the IMF projects a slower growth rate in China than was previously expected. The world’s second largest economy is now scarcely expected to achieve its 2023 growth target of around 5%, with lower investment due to the struggling property sector expected to continue to drag growth lower in 2024. India, on the other hand, has seen an upgrade to its GDP growth forecast for 2023 to 6.3% – due to stronger than expected consumption in Q2 – and this pace of growth is expected to be maintained in 2024.

Risks to the outlook

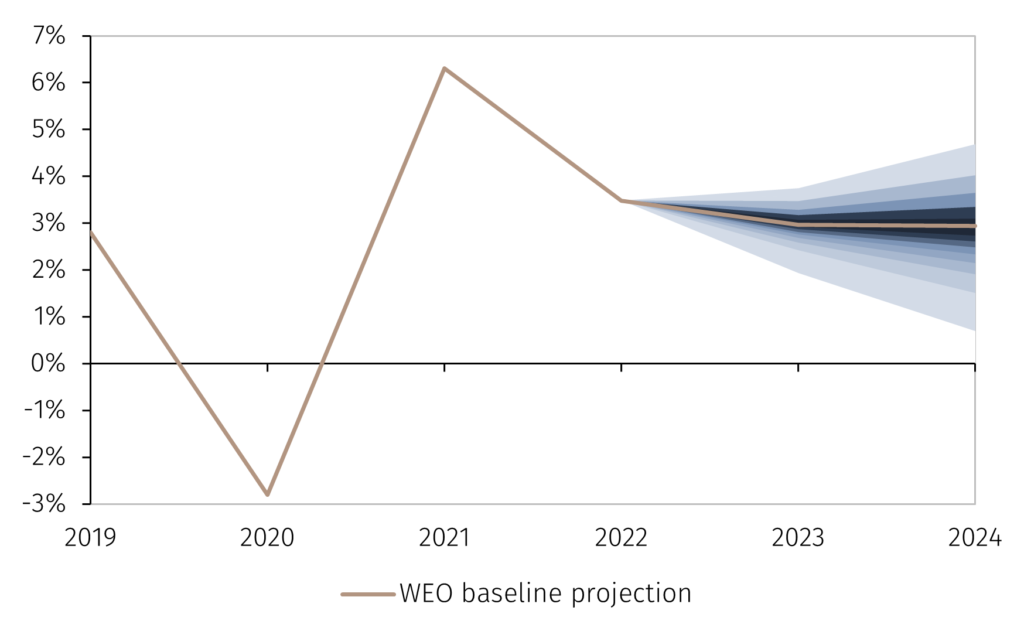

Although the distribution of risks to the IMF’s baseline forecast is more balanced compared to the previous WEO reports in 2023, the overall balance of risks remains skewed slightly to the downside (see Chart 1).

Chart 1. Distribution of forecast uncertainty around global GDP growth (%)

Source: IMF. Data as at 10 October 2023. This chart shows the distribution of forecast uncertainty around the baseline projection. Each shade represents a 5 percentage point probability.

One factor the IMF believes could support global growth is a faster than expected decline in underlying inflation. This could reflect developments such as a stronger than expected pass through to inflation from lower energy prices, or declining job vacancies leading to looser labour markets and thus reducing the need for further tightening of monetary policy.

The IMF also noted the possibility that domestic demand recovers faster than expected as an upside growth risk. This could come about as the stock of excess savings in economies such as the eurozone and UK has not yet been depleted and consumption remains below pre-pandemic trends. Furthermore, policy support in China could be stronger than is currently envisioned, boosting domestic demand.

On the downside, risks that China’s recovery slows further cannot be ruled out. This could occur if Beijing’s support to the real estate sector is not sufficient to preserve financial stability. According to the IMF, financial stability concerns in China could spill over to other EM economies through exchange rate volatility and destabilised capital flows.

The possibility that commodity prices become more volatile amid climate and geopolitical shocks was also highlighted as a downside risk. Heatwaves, droughts, and the war in Ukraine have the potential to intensify fluctuations in commodity prices, which could feed through to inflation and act as a drag on growth.

Persistence of underlying inflation due to tight labour markets, near-term inflation expectations remaining elevated, and excess savings remaining in some economies is another downside risk to global growth cited by the IMF. This could lead to central banks raising interest rates by more than is currently expected by markets, which could in turn lead to a repricing of financial market assets. As a result, further tightening of financial conditions through this mechanism could stress banks’ and nonbank financial institutions’ balance sheets.

Lending standards have tightened, and loan demand has declined in the US, eurozone, and some EM economies. Borrowing costs have risen and almost one quarter of EM economies have sovereign credit spreads above 1,000 basis points raising the risk of debt distress and, in turn, lower global growth prospects.

To conclude, global, advanced economy and EM economy GDP growth forecasts for 2023 and 2024 are little changed in the latest IMF WEO. However, this masks divergences across economies, with prospects having improved for the US and India, and having deteriorated for the eurozone and China, among others. Risks to the outlook remain tilted to the downside but a more balanced outlook has emerged compared to previous WEO reports in 2023.

* See “World Economic Outlook, October 2023: Navigating Global Divergences” https://go.pardot.com/e/931253/-economic-outlook-october-2023/3ng8b/278523720/h/QUcDGASW_rSDqvYRh0_8k0JdXraf9FfK-QAITwqJEDg

1 See “World Economic Outlook Update, July 2023: Near-Term Resilience, Persistent Challenges” https://go.pardot.com/e/931253/nomic-outlook-update-july-2023/3ng8f/278523720/h/QUcDGASW_rSDqvYRh0_8k0JdXraf9FfK-QAITwqJEDg and “World Economic Outlook, April 2023: A Rocky Recovery” https://go.pardot.com/e/931253/ld-economic-outlook-april-2023/3ng8j/278523720/h/QUcDGASW_rSDqvYRh0_8k0JdXraf9FfK-QAITwqJEDg