The International Monetary Fund (IMF) recently released its October World Economic Outlook (WEO)*. Its projections for global real Gross Domestic Product (GDP) growth in 2024 and 2025 are little changed relative to its July WEO update, although risks to the outlook are now tilted to the downside. In this Macro Flash Note, Economist Sam Jochim summarises.

IMF growth forecasts

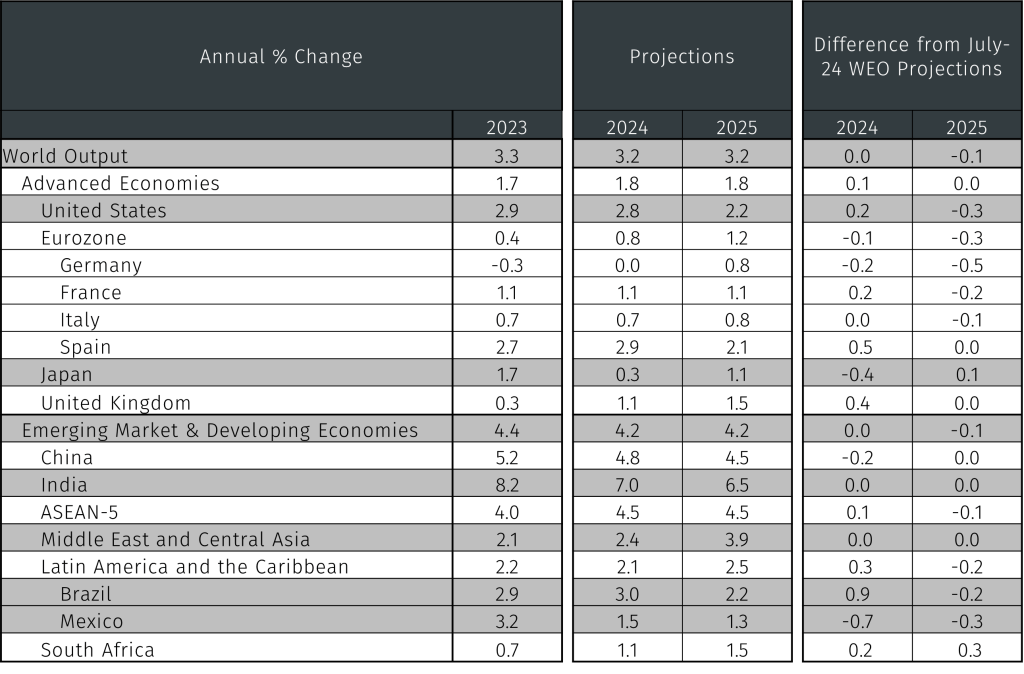

The IMF forecasts global real GDP growth of 3.2% in both 2024 and 2025, marginally below the 3.3% registered in 2023 (see Table 1). The projection for 2024 is unchanged relative to the WEO July update while that of 2025 is 0.1 percentage points lower.1

Table 1. IMF’s World Economic Outlook real GDP growth projections (% change, year-on-year)

Source: IMF. Data as at 22 October 2024.

In advanced economies, growth is projected to rise from 1.7% in 2023 to 1.8% in 2024. This represents a 0.1 percentage point upward revision to the projection made in July and is attributed to stronger growth projections for the US and UK. The upgrade for the US reflects expectations for consumption to remain resilient, while for the UK the IMF anticipates falling inflation and interest rates stimulating domestic demand.

Conversely, the IMF lowered its growth forecasts for the eurozone, though a recovery is still expected relative to the trough growth rate experienced in 2023. Much of the downward revision for the eurozone reflects persistent manufacturing sector weakness in Germany and Italy.

In emerging market economies, the IMF expects real GDP growth to decline from 4.4% in 2023 to 4.2% in both 2024 and 2025. The outlook is little changed from the July WEO update, though the projection for growth in China has declined slightly amid persistent real estate sector weakness and low consumer confidence. Mexico has also seen a downward revision to its projected GDP growth due to tighter monetary and fiscal policy, while Brazil has seen a large upward revision due to stronger private consumption and investment.

Risks to the outlook

Having been viewed as balanced throughout 2024, the IMF now believes that risks to the global outlook are tilted to the downside.

October’s WEO highlights the lagged impact of monetary policy tightening as one of the greatest downside risks to the outlook. Although most central banks across the world are now reducing interest rates, an unanticipated strengthening of the transmission of rate increases in 2023 could lead to a deceleration in growth.

Also related to monetary policy is the risk that financial markets reprice assets due to changes in interest rate expectations. If underlying inflation proves more persistent than central banks expect, consumers’ and businesses’ inflation expectations could de-anchor, forcing central banks to adjust the path of policy normalisation. The IMF notes this could lead to financial markets repricing assets and driving tighter financial conditions, acting as a constraint on GDP growth.

The outlook for the recovery in China is highly uncertain and a deeper-than-expected contraction of the world’s second largest economy’s property sector poses a downside risk to global GDP growth. Further drops in housing prices amid a contraction in sales and investment could lead to additional declines in Chinese consumer confidence and consumption, weakening domestic demand.

The IMF also stressed that protectionist policies which exacerbate trade tensions could disrupt global supply chains and increase production inefficiencies, representing a downside risk to global GDP growth. Additionally, while domestic demand in China has been weak in 2024, exports have been a bright spot.2 Elevated trade tensions could act as a drag on one of China’s main GDP growth drivers in 2024.

As was the case in April’s WEO, October’s WEO highlights commodity price spikes amid regional conflicts as a downside risk to the outlook.3 Were the conflict in the Middle East or the war in Ukraine to escalate, additional supply shocks could raise headline inflation. This would be particularly damaging for emerging market economies where food prices make up a larger proportion of household expenditure.

The IMF also highlighted upside risks to global GDP growth, stemming from the possibility of stronger momentum of structural reforms, as well as a stronger recovery in investment in advanced economies. Structural reform momentum could accelerate in an effort to address productivity and labour force participation declines. The potential for stronger investment in advanced economies reflects the demands of the green transition, infrastructure upgrades and investment in science and technology. Both factors could raise GDP growth.

Conclusion

In conclusion, the global growth outlook is little changed relative to the IMF’s previous WEO publication, and growth is expected to remain steady over the next two years. Discrepancies remain apparent across economies, with growth prospects higher in the US than in most other advanced economies, while the same is true of India within emerging market economies. The outlook is consistent with a soft landing of the global economy, although risks are now skewed to the downside, having been balanced in the previous WEO.

* https://www.imf.org/en/Publications/WEO/Issues/2024/10/22/world-economic-outlook-october-2024

1 https://www.imf.org/en/Publications/WEO/Issues/2024/07/16/world-economic-outlook-update-july-2024

2 https://www.efginternational.com/uk/insights/2024/chinas_shifting_policy_stance.html

3 https://www.imf.org/en/Publications/WEO/Issues/2024/04/16/world-economic-outlook-april-2024