Asian bond markets and currencies have been relatively resilient amid the ongoing Russia-Ukraine conflict, held up by the fall in global interest rates and the region’s generally strong economic and corporate fundamentals. But as the situation remains fluid, we will be monitoring Asian issuers’ sensitivity to supply-side risks in the event of a prolonged military conflict scenario.

Russia announced military operations in Ukraine on 24 February 2022. At the time of writing, fighting continues in Ukraine and potential negotiations between the two sides are expected to be drawn out at this point. Western allies who have spearheaded sanctions on Russia have mostly targeted the finance sector i.e. major state-owned banks, including the Central Bank of Russia (CBR), individuals close to the leadership as well as new public debt issued after 1 March 2022. Some Russian banks are banned from the SWIFT international payments system. The list is still being finalised by the EU partners.

These sanctions have impeded the overall function of Russian capital markets, forcing Russia to introduce capital controls and suspend trading on the local stock market. More recently, the CBR has also announced a temporary suspension on outward remittances including coupons and dividend payments to foreigners. As the overall situation remains fluid, sentiment has deteriorated with bonds correcting to distressed levels ranging from 10-50 cents and liquidity is thin.

Asian bonds and currencies show resilience for now

On a macroeconomic level, the conflict’s direct impact on Asia appears to be contained in the near term as the region’s trade linkages with Russia and Ukraine are generally low. Not all Asian countries have also imposed sanctions on Russia. China, for example, has announced that it would lift all wheat-import restrictions on Russia, paving the way for increased wheat imports from Russia.

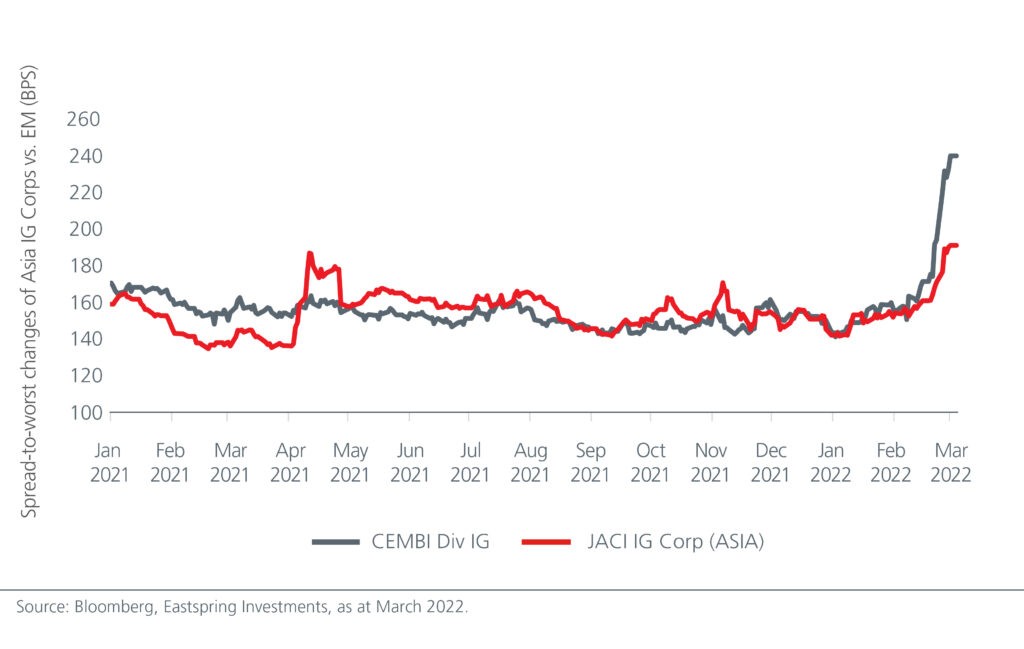

Hence, we expect the key impact on Asian bond markets in the near term is likely to be from the fluctuations in risk appetites, as well as rises in energy and commodity prices. Since the start of the conflict, risk assets in Asia, including Asian USD credits and Asian currencies, have experienced some weakness amid the deterioration in risk sentiment. However, the declines have been moderate with the Asian USD credit market falling by around 1%1.

Fig 1: Spread widening is more moderate for Asian investment grades’ corporates

Asian currencies fell modestly by an average of 0.7% against the US dollar2. This compares with the 4-5% decline seen in Emerging Market bond and currency markets. Asian local currency government bonds have mostly held up well as the fall in global interest rates on the back of rising global growth uncertainties lifted performance.

The relatively resilient performance of Asian bonds and currencies underlines the market’s view that the region is relatively shielded from the direct repercussion of the conflict, while the region’s generally strong economic fundamentals could also provide a buffer to exogenous shocks. Asian credit markets have also shown the ability to weather through past periods of commodity price spikes (i.e. 2011 and 2014) without a significant rise in default rates during those years.

Be mindful of the differing impact on Asian countries

We are however mindful that the rise in oil and commodity prices, including food and base metal prices, will still exert upward pressure on inflation rates in Asia. This complicates the central banks’ reaction function, while bringing more growth and currency uncertainties into the region.

The impact on individual countries will not be even; current accounts in countries like Philippines, India and Thailand are likely to be more sensitive to rises in oil prices, while energy and commodity producing countries like Indonesia and Malaysia may see their terms of trade improve. It is also worthwhile to note that while inflation is expected to rise across Asia, the rise in inflation rate may not necessarily lead Asian central banks on a more hawkish monetary policy path than previously anticipated, especially as there remain significant output gaps in several Asian countries.

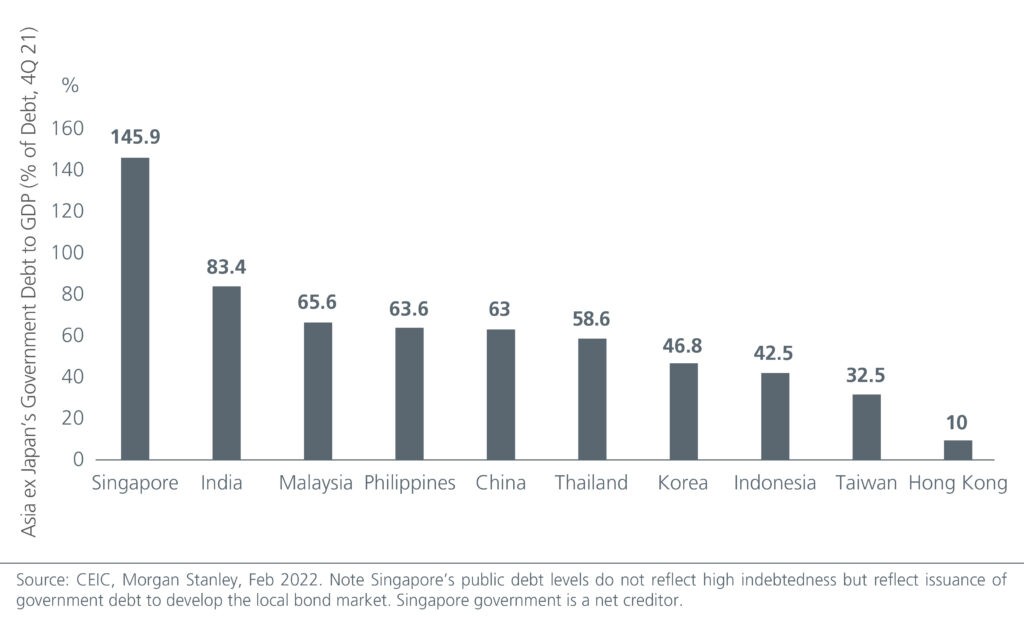

Asian central banks have typically looked through past episodes of commodity prices increases. They tend to support growth, while leaving governments to utilise administrative or fiscal measures, such as increase of oil subsides to help cushion the rise in commodity prices. Further, the ability for Asian governments to provide such support remains intact. Government debt ratios in most Asian countries are below 70%, suggesting room for Asian governments to increase spending to help absorb the impact of energy and commodity prices.

Fig 2: Asian governments’ debt ratios are favourable

Most Asian corporates can withstand near-term fallout from the conflict

On a corporate level, similarly, the direct exposures of Asian companies to Russia and Ukraine businesses or operations are largely manageable, while the rise in input prices could impact individual companies by varying degrees. Asian producers in the energy, base metal, coal, and palm oil industries could benefit from higher energy and commodity prices, while power generation and selected manufacturing companies which rely more heavily on commodity /energy inputs could be adversely hit. However, even in these sectors, the magnitude of impact is not likely to be straightforward and would vary from company to company. Factors such as the company’s ability to pass on price increases to consumers, likelihood of government support (for government-owned utility companies), as well as the ability to source for substitute inputs would play a part in determining the outcome.

All in all, assuming that the rise in energy and commodity prices would be temporary and mitigated by government response, we expect most Asian companies to be able to withstand the near-term impact of the Russia-Ukraine conflict. However, we will be monitoring the issuers’ sensitivity to supply-side risks and will make the necessary portfolio adjustments to reflect our views on the winners and losers, backed by valuations. We are also mindful that a sustained military conflict and further sanctions could lead to deeper dislocations of supply chains which will result in a broader global economic fallout that could challenge our base-case scenario.