Against an uncertain global economic outlook, a stable income stream is an attractive proposition for investors. We encourage investors to seek income from multiple sources and believe that there are compelling opportunities within Asian REITs and Asian dividends.

Investors today face concerns over rising inflation and higher interest rates. This is in stark contrast to the past few decades of low interest rates and declining bond yields. Nevertheless, despite rising interest rates, we believe that there are still attractive opportunities in selected income strategies, particularly in Asian REITs and dividend-paying Asian equities where new growth drivers are emerging.

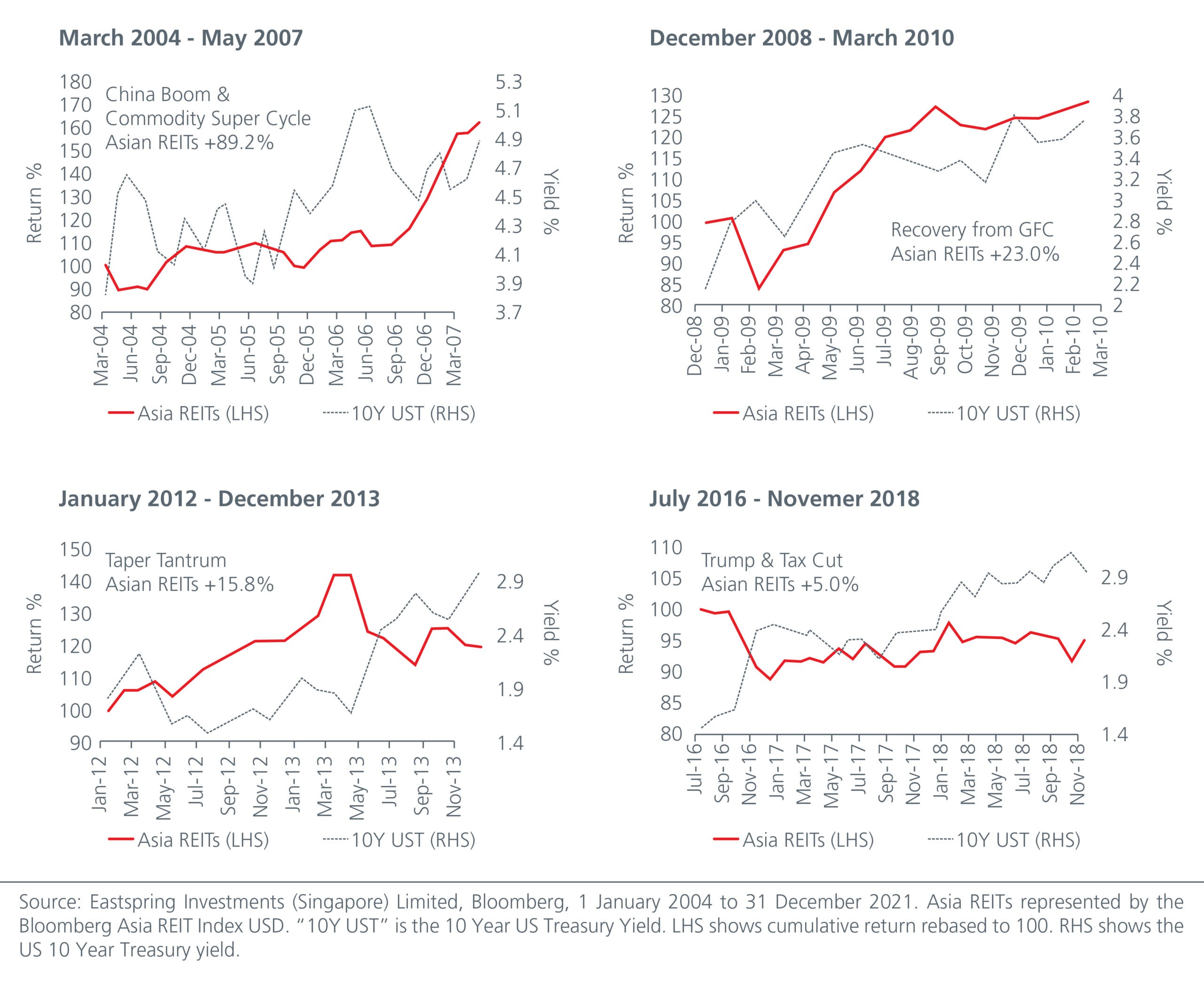

Asian REITs have delivered positive returns in times of rising yields

In the last four periods when the US 10-yr treasury yield rose by more than 100 bp, Asian REITs still delivered positive returns. See Fig. 1.

Fig 1. Performance of Asian REITs during rising rate cycles

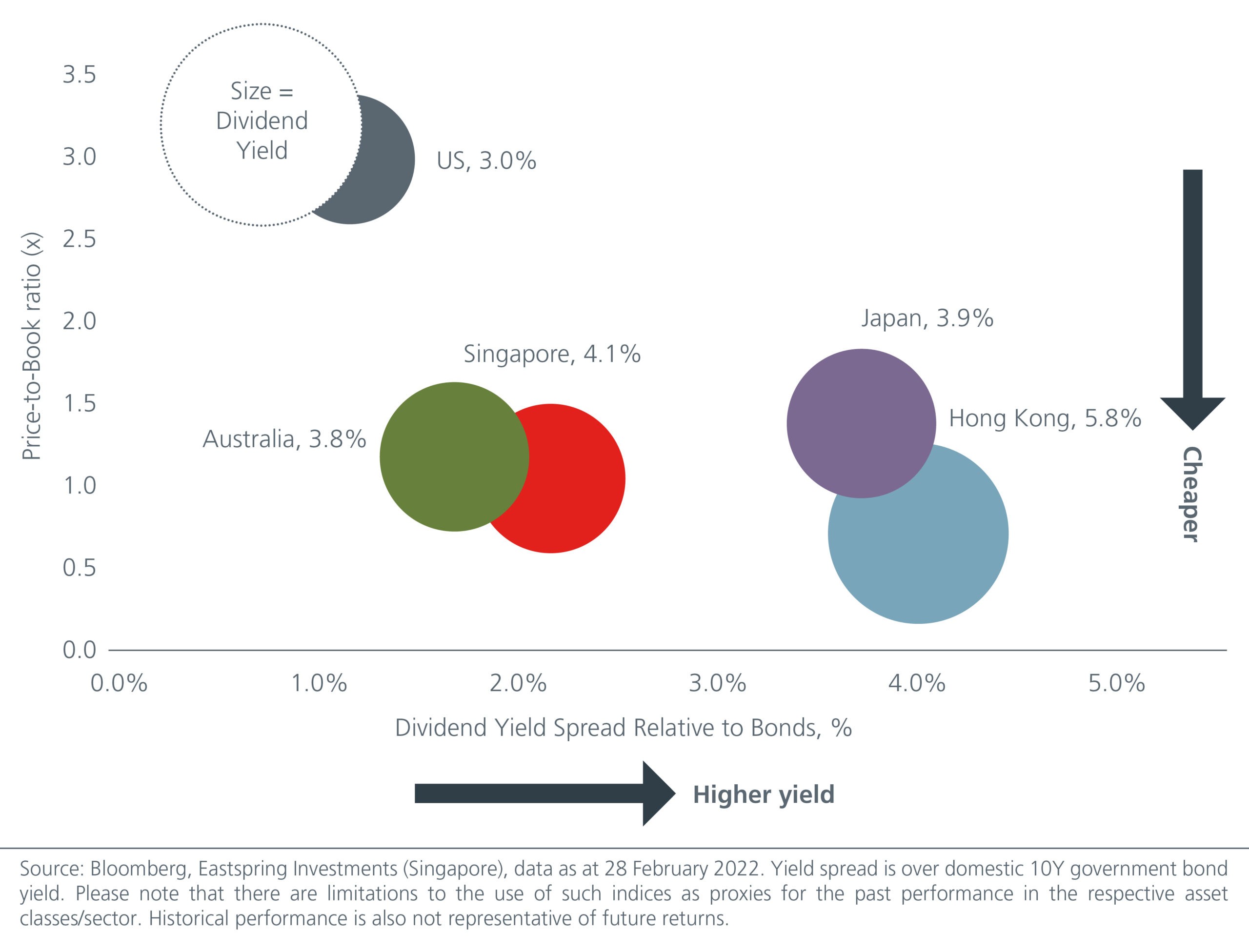

Meanwhile, even with the US 10-yr treasury yield trending above 2%, the yields from Asian REITs are still more attractive. See Fig. 2. Compared to US REITs, Asian REITs are more attractively valued and have lower gearing. Total debt to asset ratio for Singapore, Australia and Hong Kong REITs average 37.5%, 24.9% and 26.0% respectively versus 45.5% for the US1.

Fig. 2. Hong Kong and Singapore REITs offer attractive yields

Although the dynamics for Asian real estate have changed due to the pandemic, there are still exciting growth segments to invest in. Changes in the usage of retail and office space are giving these segments new leases of life. In addition, as countries re-open borders and ease their safe distancing measures, hotels and malls are likely to benefit.

As work norms evolve, the pros and cons of working from home may differ in Asia vs the developed economies, given the region’s smaller homes and shorter commuting distances. Nevertheless, some companies in Asia have moved to a permanent hybrid model as more tasks become digitally enabled. With employees having the flexibility to work away from the office, the demand for co-working spaces has risen.

At the same time, during the pandemic we saw rising demand for new/additional office space from new economy sectors. For example, in 2020, it was announced that Chinese internet company Tencent picked Singapore as its Asian hub and Tik Tok owner Bytedance planned to expand its office space in Singapore’s central business district in 2021. Meanwhile, within Asia, Singapore remained a key market for acquisitions with Alibaba’s purchase of a 50% stake of the AXA Tower in 2020 and Allianz Real Estate’s acquisition of a 50% stake of OUE Bayfront in 2021. Investment firm KKR has also identified Singapore as one of the core markets for its USD1.7 bn fund which targets real estate investments in the Asia Pacific.

Meanwhile, the rising adoption of cloud-based services is driving the construction of hyperscale data centers in Asia. The data center market in South East Asia is expected to grow at a compounded average growth rate of 6% from 2019 – 2025, with Singapore having the greatest potential followed by Indonesia, Malaysia, Thailand and Vietnam.2

Across Asia, demand for technology parks is also surging, in part driven by government policies seeking to leverage on innovation to drive economic growth. In India, new technology parks are being positioned to be production hubs aimed at both domestic and international markets. In China, demand for technology parks is rising amid the government’s push for greater technological self-reliance.

“Green buildings” that reduce the negative impact on the environment because of their design and construction will also increasingly come into focus amid rising demand from sustainability-focused tenants. The demand for sustainable buildings in Asia Pacific currently exceeds supply, allowing landlords to charge a premium of 10% above prevailing rents3.

The diversity within Asia’s REITs markets means that active managers can leverage on the unique characteristics of the different segments and their cyclical dynamics to increase portfolio yield.

Asian dividends have been a big driver of returns

Dividends can be another building block in an income portfolio. Historically, dividends are a relatively stable source of income due to their information content. Companies often prefer to keep dividends steady as a dividend cut could signal earnings or cashflow problems.

Evidence from both developed and emerging market equities shows that earnings have historically increased in the year of dividend initiation as well as in the following years. The initiation of a regular cash dividend has also been accompanied by capital gains4.

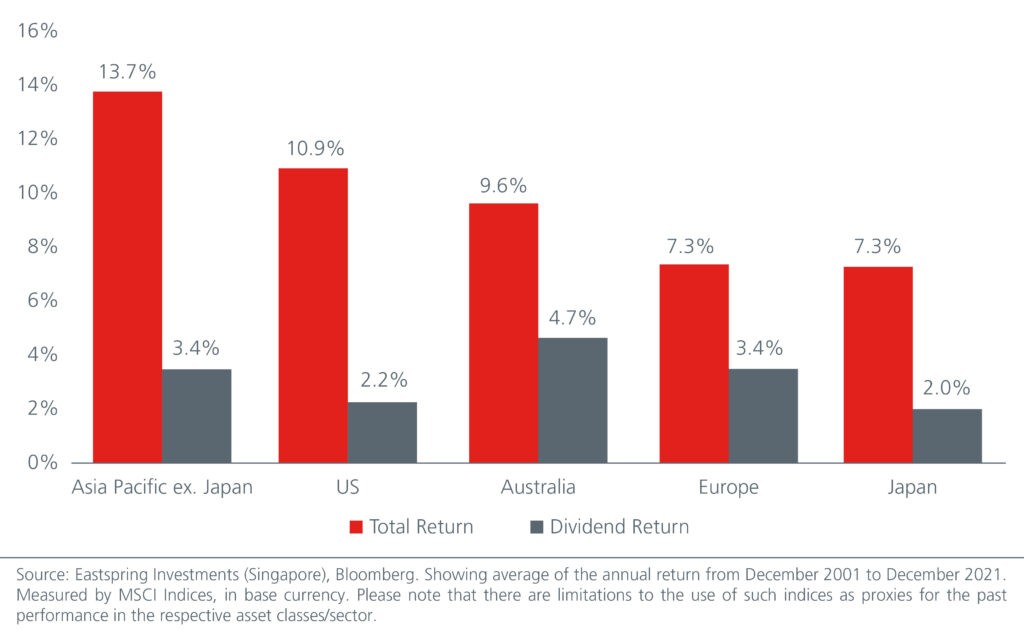

In the last twenty years (2001 to 2021), dividend returns in Asia have beaten those from the US and are comparable to those from Europe. Fig. 3.

Fig. 3. Average annual total and dividend return (%) – December 2001 to December 2021

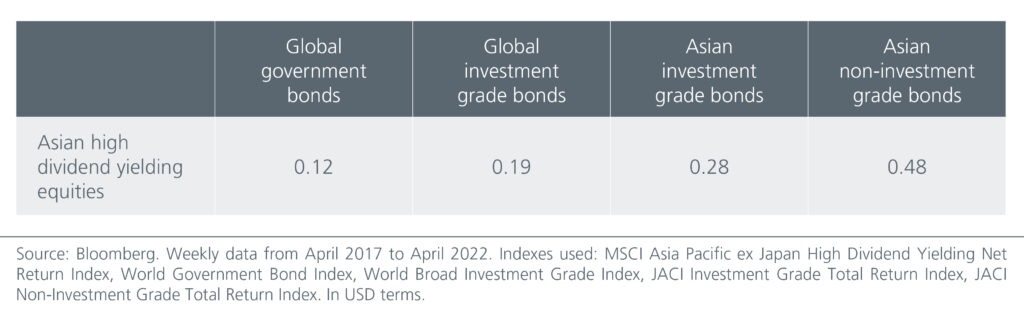

Asian dividends also have a low correlation to Asian and global bonds, a plus for investors seeking to build a diversified portfolio of income producing assets. Fig. 4.

Fig 4. Low correlations with Global and Asian bonds

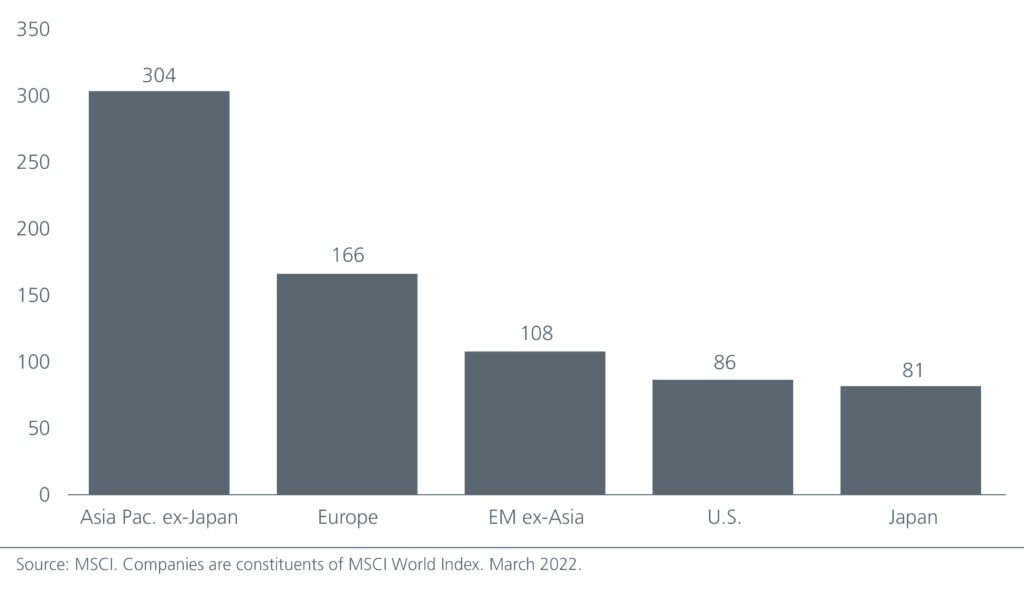

While the MSCI Asia Pacific ex Japan index has a dividend yield of 2.55%5, investors can achieve a higher than benchmark yield through careful active selection. Asia appears well suited for a high dividend strategy. The number of stocks in Asia Pacific ex Japan that have dividend yields above 3% is almost twice that of Europe and more than 3x that of the US. Fig. 5

Fig 5. Number of companies with dividend yields above 3% by region

In selecting dividend-paying equities, investors should assess that companies have sensible capital management policies that are appropriate to the stage of their business cycle and development. This increases the sustainability of their dividend payouts. While we like steady yielders – companies that make high and steady payouts from recurrent income, we are also on the lookout for companies that have the potential to grow their dividends. In addition, a company’s dividend yield may at times be elevated as its share price is unjustifiably low. In such a scenario, investors not only enjoy an attractive yield but also the potential for capital gains when valuation normalises. That said, investors need to be wary of value traps. More experienced investors can also take advantage of opportunistic dividend payouts that occur when a company monetises selected assets.

Dividends fell significantly in early 2020 due to the unprecedented nature of the COVID-19 outbreak but have recovered since. Dividend per share (DPS) growth was positive in 2021, led by Asia Pacific ex Japan and developed Europe. In 2022, dividends in Asia Pacific ex Japan are expected to grow by 4.6%. At the point of writing6, we favour the energy and real estate sectors as they are natural hedges against inflation. We also like the more defensive but still high dividend paying utilities and telecoms sectors.

Seek income from multiple sources

Against an uncertain global economic outlook, having a stable income stream is an attractive proposition for investors. We believe that investors should seek income from multiple sources and there are compelling opportunities within Asian REITs and Asian dividends. Asian REITs can benefit from the exciting growth opportunities found in data centers, technology parks, green buildings as well as the re-opening boost enjoyed by malls and hotels. Meanwhile, Asia appears well-placed in an income portfolio given its large universe of high dividend paying equities versus other regions.

This is the fifth of a series of eight articles which examines the different investment strategies investors can adopt to tap on the opportunities that are emerging in Asia

Sources:

1 Credit Suisse Research. For US: MSCI US REITs Index, April 2022.

2 Data Center Market in Southeast Asia 2021 Key Drivers and Challenges. Opportunities and Forecast Insights by 2025.

3 https://www.scmp.com/business/article/3146055/asia-pacific-developers-focus-green-buildings-they-take-steps-meet-climate

4 Analysis of Dividends and Share Repurchases. Gregory Noronha, PhD, CFA, and George H. Troughton, PhD, CFA

5 MSCI. As of February 2022.

6 13 April 2022.

Disclaimer

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore and Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws.

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (531241-U).

This document is produced by Eastspring Investments (Singapore) Limited and issued in Thailand by TMB Asset Management Co., Ltd. Investment contains certain risks; investors are advised to carefully study the related information before investing. The past performance of any the fund is not indicative of future performance.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

United Kingdom (for professional clients only) by Eastspring Investments (Luxembourg) S.A. – UK Branch, 10 Lower Thames Street, London EC3R 6AF.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author on this page, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this posting is at the sole discretion of the reader. Please consult your own professional adviser before investing.

Investment involves risk. Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments (excluding JV companies) companies are ultimately wholly-owned/indirect subsidiaries/associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company, a subsidiary of M&G plc (a company incorporated in the United Kingdom).