In the early 1990s Japan suffered a well-documented deflationary slump. With China now seeing high-profile defaults, slowing economic growth and falling consumer prices, is North Asian history repeating itself?

It seems that barely a week goes by without further negative Chinese economic data being announced. Most recently, property giant Country Garden dragged sentiment lower after missing coupon payments, adding to the sector’s wider malaise.

As a result, there are mounting anxieties in China among developers, the wider economy, and the financial system. New economic activity data points have highlighted spill-over effects from real estate to the broader economy, with growth in investment, industrial production and retail sales all receding as sentiment sours.

On top of this, and despite much of the rest of the world experiencing the opposite challenge of high inflation, July saw Chinese consumer prices actually fall, prompting the Chinese central bank to cut interest rates and investors to make comparisons with Japan’s deflationary spiral in the early 1990s.

Property pressures

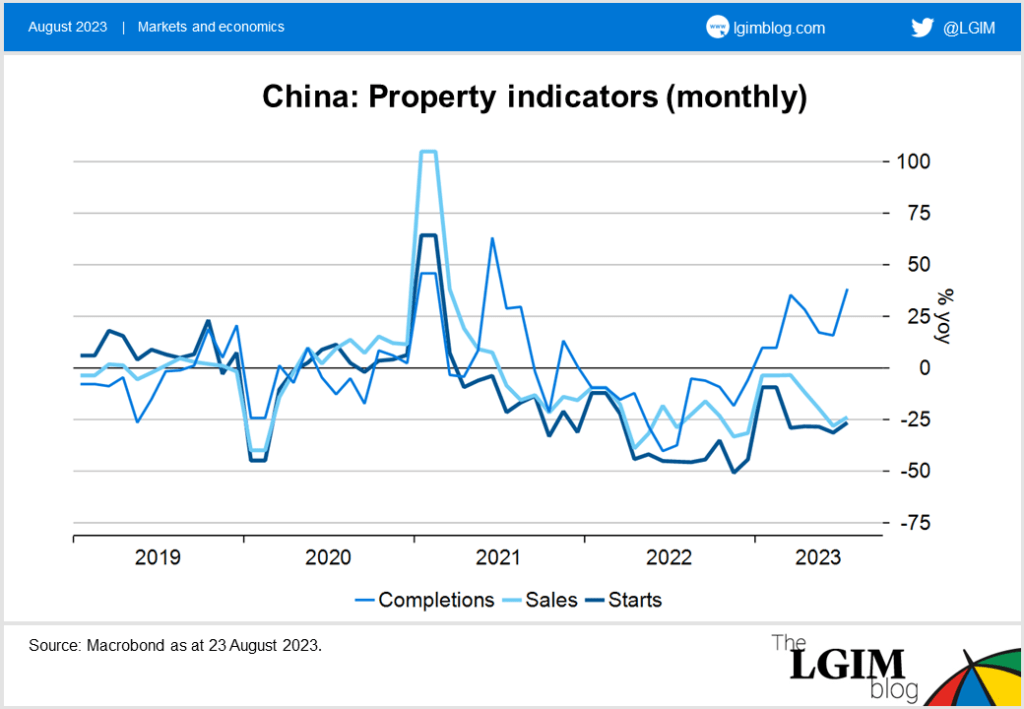

Amid all the gloom, it’s worth noting that property completions are actually going well, and it sounds like developers, banks and local authorities are putting all their focus on finishing already-sold properties.

That’s good for society as there are still a few million unfinished properties that people have already paid for. However, property sales and housing starts are desperately weak:

Despite the positive number of completions, the backdrop of depressed sales and new housing starts helps to explain why developers are defaulting and bond investors are worried about their recovery value. Furthermore, exposed lenders are under pressure, with financial trust Zhongrong recently skipping payments on its investment products.

Short-term solutions

Taken together, the weakness in the property sector, missed trust fund payments, sliding real activity, and financial stress have led some to declare that this is a ‘Lehman moment’ and a potential presage of a financial crisis. We are less sure. There is of course always room for policy mistakes, but scale-wise the problem looks manageable to us.

So while pain in trusts like Zhongrong requires attention, and financial sector troubles can escalate very quickly, we don’t see China’s current woes as a prelude to a 2008-style crisis. Domestic banks are well-capitalised and authorities can easily direct capital through the state-led banking system.

Importantly, the Chinese shadow banking sector has been small enough to be moved back onto banks’ balance sheets for some time. This is even more true today after a rigorous campaign to shrink it. Banks’ loan-to-deposit ratio is 80% and would stay below 100% if the shadow banking sector were brought back onto banks’ balance sheets.

In addition, banks’ reserve requirement ratio in China is still significantly higher than in other countries (approximately 10% compared to 5%), providing banks with sufficient reserves to shoulder shadow banks.

The waiting game continues

In terms of asset prices, investors are still very much waiting for stimulus to help revive the country’s China financial markets. On the monetary side, the People’s Bank of China has cut various interest rates by 10-15bps recently, but in terms of robust fiscal support, outside of a total emergency, investors may potentially have to wait for the following key events:

- The National Financial Work Conference (September or perhaps Q4)

- The Third Plenary Session (likely in October)

- The next Politburo meeting (also October)

However, there continues to be a strong pushback against income disparity, and we think this also applies to excess asset price appreciation, which is one of the key drivers behind the pressure on property speculation and perhaps why stimulus thus far has been muted.

Long-term challenges and opportunities

What all of the above means for China longer-term is a different story. Taking a step back, we believe the current stress marks an end to a period of high growth as the economy reckons with historical imbalances, which is similar to the experiences of Japan and also South Korea in the 1990s.

But that’s not to say the picture in China is entirely negative. The bursting of an asset bubbles does not always lead to a financial crisis, with Japan in the early 1990s being a prominent example. And if 1990 Japan could avoid it, China is even more likely to do so in our view given its state-owned banking sector. In addition, emerging companies in this new growth model, in particular vehicle and electronics manufacturers, are continuing to grow despite pain in the property sector.

So is China the next Japan?

China is certainly undergoing a dramatic rebalancing. After significant overinvestment, particularly in the property sector, we believe growth looks likely to be about half of what it was pre-COVID over the next 15 years. In this China does indeed resemble Japan, where growth fell from 5% to 2.5% after the 1990 bubble burst.

However, while China’s transition to a period of lower growth is likely to be painful, and the authorities will remain watchful for any potential crisis, it is a transition we expect the country can manage. Comparisons with the US in 2008, where a deflationary bust triggered a financial crisis, look wide of the mark in our view.