Japan’s small- and mid-cap corporates are an underappreciated asset class. Investors tend to chase the popular names and smaller-cap opportunities tend to go unnoticed or ignored. Our understanding of behavioural biases and the use of a disciplined valuation anchor enables us to exploit the inefficiencies and draw out alpha in the small- and mid-cap market.

In our previous article Why you should not ignore Japan Inc, we pointed out that Japanese corporates have been surprisingly resilient despite the Covid-19 pandemic. Gradual but steady restructuring over the last decade has been supportive of higher operational efficiency and improved trend profitability and consequently put Japanese corporates on a stronger footing to weather the major exogenous shock.

While the pandemic certainly dealt a cyclical hit to margins, the impact was not permanent as trend improvement has remained intact. This is likely testament to the progress made from the consistent and ongoing corporate reforms. Additionally, improvements in corporate governance have also been gathering momentum and have become a key factor influencing the attractiveness of Japanese equities.

Large-cap corporations may get the most attention in the global media, but similar trends can also be seen in the small and mid-cap (SMID) space. Just as with larger caps, government policy (for example, the Japan Stewardship Code and Japan Corporate Governance code) plus an evolution in corporate culture and the emergence of activist investors have all been driving change in small and mid-caps.

The ongoing positive structural changes seen across the economy, such as deleveraging of balance sheets, rising dividend payouts, stock buybacks and numbers of contested takeovers are just as evident in small- and mid-caps. Many SMID stocks are also starting with very conservative balance sheets in terms of high levels of net cash; currently 61% have more cash than debt on their books, versus 49% historically. This is also in contrast to many of their developed market peers, where net debt-to-EBITDA ratios are almost near all-time highs1.

Significant universe

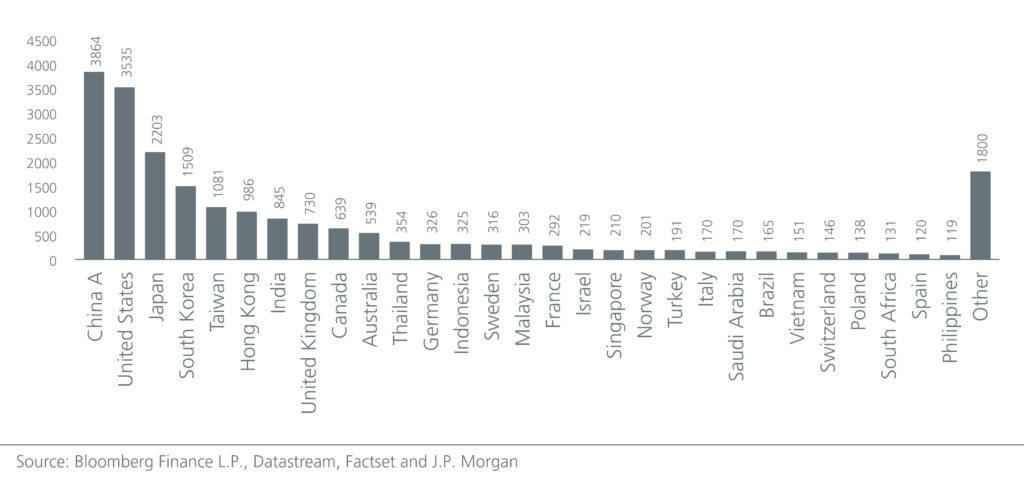

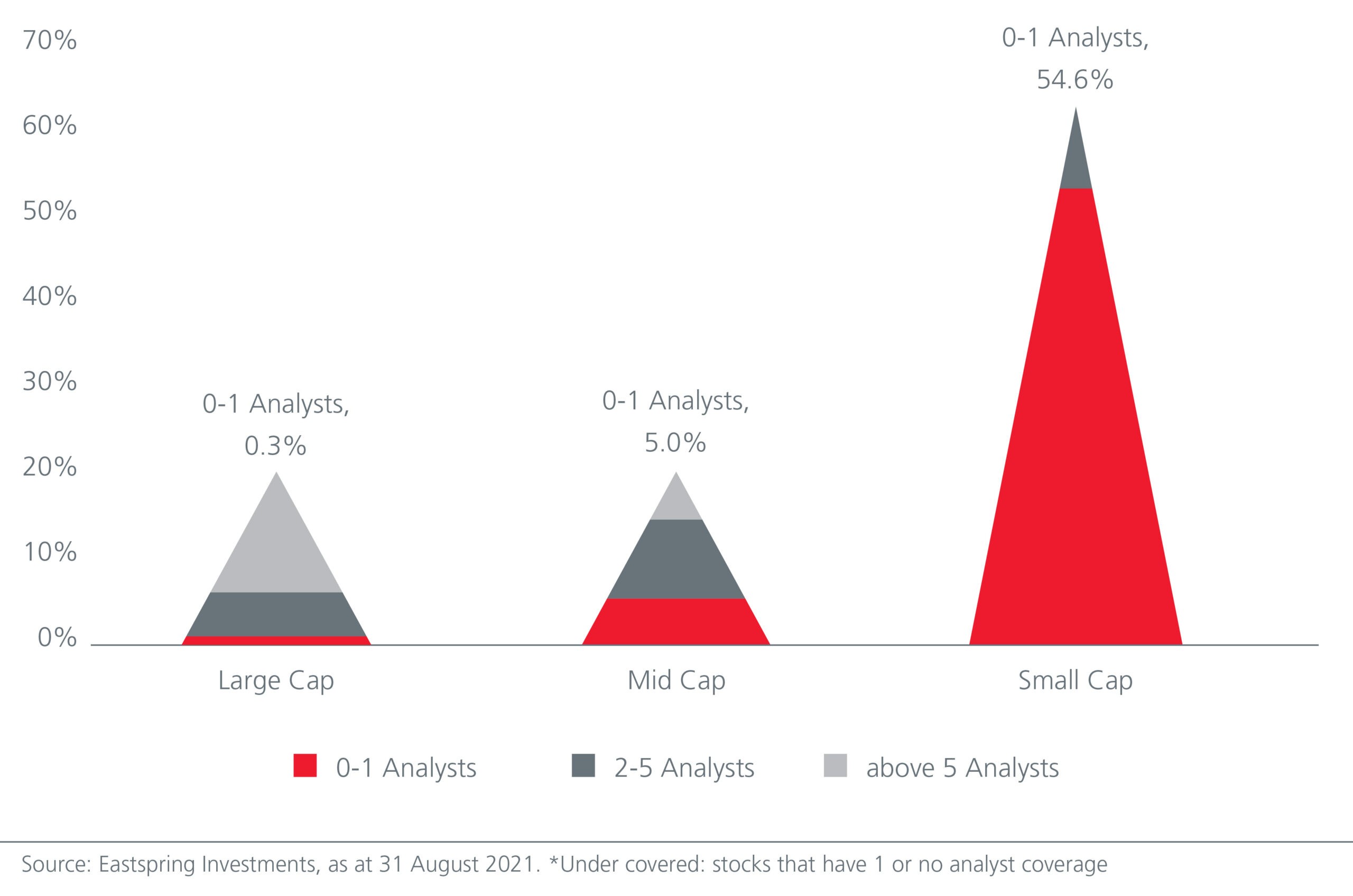

Japan’s small to mid-cap (SMID) universe is impressive in terms of the sheer number of listed stocks. See Fig. 1. Small-cap stocks, for example, represent approximately 67% of the Japan universe2. However, small cap Japanese stocks are often under researched. The amount of sell-side analyst coverage is a good proxy for the market’s focus. Analyst coverage increases for stocks that are in favour with the market. Within the TOPIX Index, under covered* small-cap stocks represent almost 55% of the index. See Fig 2.

Fig 1: The SMID universe by countries

Fig. 2: Long tail of under covered* small- and mid-cap stocks

We believe that factors including lower analyst coverage and cheaper valuations, both in aggregate and in the extremes of valuation dispersion, usually indicate more exaggerated behavioural biases within the smaller cap universe compared to the broader market. We repeatedly see cases where smaller companies not only fall out of favour, often for shorter-term thematic reasons, but are also dropped from analyst coverage altogether. This drives mispricing to the sort of extremes where good or improving companies are simply ignored. Given that our investment process relies on exploiting persistent behavioural biases, this is a very good thing for us.

Diverse representation

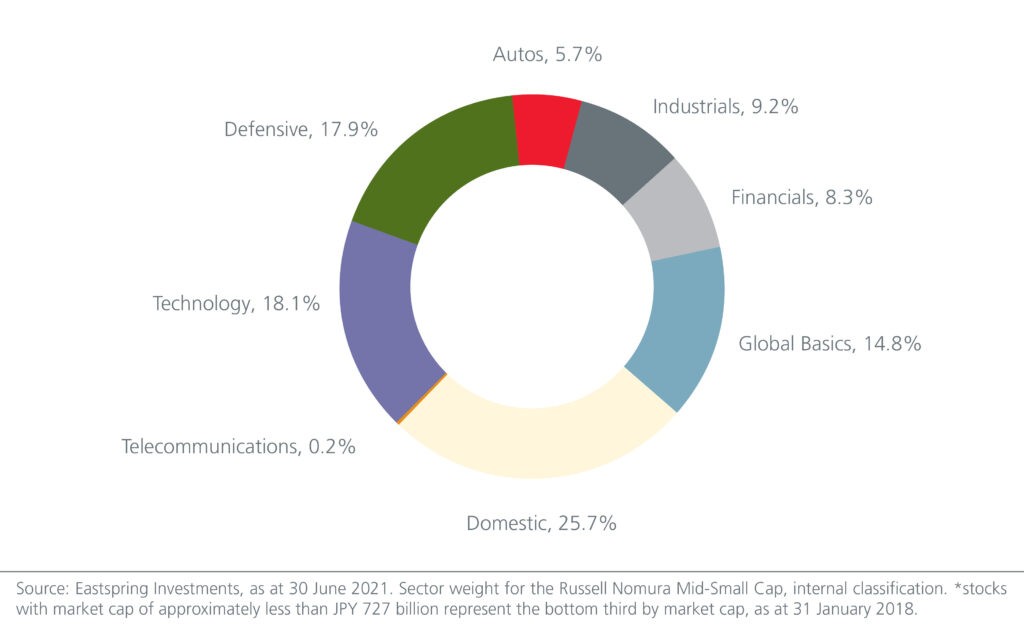

Another potential bias or oversimplification we have observed is that Japanese SMID companies are often seen as being domestic in nature. This has perhaps encouraged investors to treat the segment as largely a thematic play on Japan’s domestic market. But contrary to popular market perception, however, the SMID investment universe is in fact well represented by companies generating earnings overseas. Domestic and export related companies are distributed widely across a range of industries. See Fig 3.

Fig 3: Japan’s SMID cap universe is diverse

Meanwhile, with vaccinations currently on track and the easing of restrictions post the Olympics, Japan’s economic growth should pick up here on and the boost will come from domestic demand as the economy reopens. The upside for the domestic consumption and services sector which has been affected by the pandemic therefore seems large, and small cap stocks in these segments are poised to benefit.

Undemanding valuations

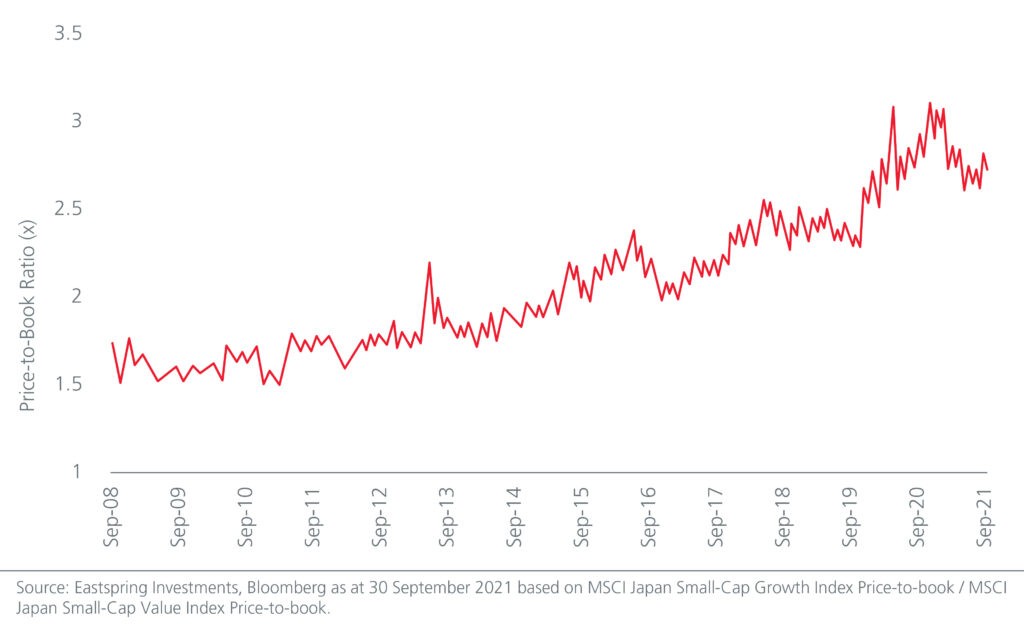

As we have also seen in the Japanese market more broadly, the overall valuation dispersion between expensive and cheap small-cap stocks remains near all-time highs. See Fig.4. Over a multi-year period, market risk preferences have gravitated towards companies with perceived high earnings growth and solid near-term earnings momentum. This has resulted in a market dynamic that has seen investors crowd into a narrow group of expensively valued stocks, including domestic, technology-related and defensive names. Ultimately, we believe these valuation extremes are not sustainable as they are not representative of the likely trend earnings power of the underlying companies.

Fig 4: Valuation dispersion in Japanese small caps has continued to widen

The flipside of the currently extremely bifurcated market is that, whilst there is a narrow market focus on expensively valued growth, there is also a wide range of other segments which are extremely out of favour – often unjustifiably so on a longer-term valuation basis. Our focus on significant mispricing based around valuation leads our approach to opportunities within this wide range of undervalued sectors in the small and mid-cap market.

Smaller companies, on average, lag in governance practices. This provides a lower starting point for much larger improvements on this front. This also provides a conducive environment for investors to constructively engage on capital structure, including stock buybacks or increased dividend payouts. Ultimately, there is great potential in this universe for long term valuation-based stock pickers to find and exploit mispriced stocks that may be out of favour with the market but where there are signs that governance may be starting to improve.

Drawing out the alpha

With undemanding valuations and a wide investable universe of about 2000 stocks, Japan’s small- and mid-cap space is prime territory for longer term valuation-driven stock pickers. We believe it is an environment which our value investment process is ideally positioned to exploit. Our investment process is based on the understanding that the greatest opportunities are likely to be found where the market’s shorter-term preferences and extrapolation have caused a large dislocation between the price and relative value of a company. This is the group of outliers we focus our fundamental analysis on.

Our differentiator lies in understanding the present value of a company’s future cash flows and what the market is currently pricing. Our concept of value is not reliant on accurately forecasting these cash flows, but rather on understanding them on a trend level by conducting rigorous due diligence on likely drivers of future returns of a business, what has been changing cyclically or structurally and how a company may adapt.

When the market materially misprices the likely income stream of a company in either direction, this presents us with both risk as well as opportunity. Our process is good at drawing out opportunities. It has allowed us to generate long-term returns.