Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested.

The Liontrust UK Micro Cap Fund returned -5.1%* in March. The FTSE Small Cap (excluding investment trusts) Index and the FTSE AIM All-Share Index comparator benchmarks returned -7.0% and -5.8% respectively. The average return of funds in the IA UK Smaller Companies sector, also a comparator benchmark, was -5.7%.

The month began with strong economic data which lifted expectations for the number of central bank hikes still to come. As news of Silicon Valley Bank’s (SVB) demise fed through, the market narrative quickly shifted to one of financial sector resilience, which in turn seemed to reduce the chances of substantial further monetary tightening.

With investors fretting over banks’ exposure to a combination of a negative yield curve (meaning more expensive short-term deposit finance and mark-to-market losses on long-term assets) and the risk of deposit flight, the sector took a broad-based hit. Credit Suisse was the highest profile casualty, forced into a government-brokered sale to UBS that wiped out bondholders and the majority of its share price.

Although based in the US, SVB had strong ties with the technology sector globally, including companies in the UK. The Fund is overweight in financials, but this is mainly via asset managers and financial services providers. As a group, they posted a return of around -7.9%.

At the small cap end of the market, companies’ liquidity became a focal point. Although SVB’s operations were relatively small in global banking terms, it had strong ties with the technology sector, including companies in the UK. As its balance sheet unravelled and regulators stepped in, many companies – particularly small caps – chose to issue stockmarket updates in order to reassure over their exposure to SVB and liquidity position. Several portfolio stocks were among this number. The common theme was that where SVB exposure existed via deposits or borrowing facilities, it was an insignificant proportion of overall liquidity.

The Fund’s largest detractors fell for reasons unrelated to the banking crisis. Shares in frontline healthcare services provider Totally (-43%) lost ground at the start of the year due to delays in the re-tender process for some contracts that were due to expire. It took another leg lower in March after issuing a profit warming, saying that earnings for the year to 31 March 2023 will be below market expectations, due not only to the contract delays but also higher costs incurred through a greater reliance on agency staff following clinical workforce shortages.

Calnex Solutions (-37%) provides test and measurement tools to the global telecommunications sector. In a trading update, it outlined that financial results in the year to 30 March 2023 will be in line with expectations but the following year’s trading is likely to be hit by a challenging macroeconomic outlook. It commented that many of its telecoms customers have reported a softening in short-term demand for their products and services and are taking a more cautious approach to investment decision. Calnex now expects to experience negative growth in the year to 30 March 2024.

The Fund’s top performer in March, Belvoir Group (+21%), had been under pressure for much of 2022, particularly in the final quarter after Truss and Kwarteng’s mini-budget derailed the UK mortgage market. It still recorded 14% revenue growth to £34m during the year, with 12% attributable to acquired businesses. Profit before tax slipped by 2% to £9.1m. The tone of Belvoir’s outlook comments were more positive, however; it said that mortgage activity has recovered by about 20% compared with Q4 2022. With house transactions taking up to five months to complete, this improved activity won’t feed through to Belvoir’s financials until the second half of 2023, but the news was enough to lift the shares.

EKF Diagnostics (+11%) staged a partial recovery from the falls suffered after last month’s profit warning. Its contract manufacturing and laboratory testing divisions have been affected by a drop in demand for Covid testing, while there have been supply chain delays in the life science division regarding fermentation capacity build out in the South Bend Indiana plant. During March, the company announced the disposal of ADL Health, its laboratory testing business, and full-year results revealed that it will discontinue its UK contract manufacturing operations. EKF Diagnostics will now focus on point-of-care, central laboratory and life sciences divisions.

Having said in a late-January trading statement that earnings would be slightly ahead of expectations, Microlise Group (+11%) followed up in March with a strong set of 2022 results. The telematics software provider for fleet operators grew like-for-like subscriptions by 9% to 599,000, with a very low churn rate of 0.4% by value. Against a backdrop of cost inflation and component shortages, it was still able to grow adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) by 6% to £8.2m, after revenue rose 5% to £63.2m. Microlise also confirmed that it expects to achieve market expectations for the new financial year.

Mobile payments company Bango (-17%) had outperformed the market so far this year, helped along by an upbeat trading update issued in January. It gave back most of this relative performance in March, despite issuing solid looking 2022 results. Revenue rose 38% to $28.5m, and adjusted EBITDA of $5.0m was ahead of market expectations albeit down 17% on last year due to the short-term impact of its DOCOMO Digital acquisition. End user spend rose from $4.1bn in 2021 to $5.6bn in 2022 and finished the year at an annual run-rate of $8.6bn. Bango also provided upbeat comments on trading so far in 2023 and the outlook for the rest of the year.

Positive contributors included:

Belvoir Group (+21%), Kitwave Group (+15%), Bigblu Broadband (+12%), EKF Diagnostics (+11%) and Microlise Group (+11%).

Negative contributors included:

Totally (-43%), Calnex Solutions (-37%), Solid State (-18%), Bango (-17%) and Record (-16%).

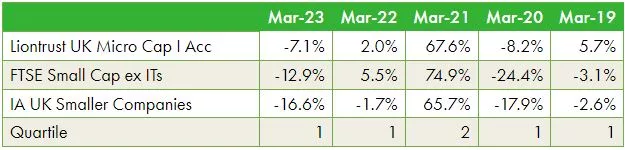

Discrete years’ performance** (%), to previous quarter-end:

Past performance does not predict future returns

**Source: Financial Express, as at 31.03.23, total return (net of fees and income reinvested), bid-to-bid, institutional class.

KEY RISKS

Past performance is not a guide to future performance. The value of an investment and the income generated from it can fall as well as rise and is not guaranteed. You may get back less than you originally invested.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

The portfolio is primarily invested in smaller companies and companies traded on the Alternative Investment Market. These stocks may be less liquid and the price swings greater than those in, for example, larger companies.

DISCLAIMER

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID), which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.co.uk or direct from Liontrust. Always research your own investments. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.

This should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets. It contains information and analysis that is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content of this document, no representation or warranty, express or implied, is made by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified. It should not be copied, forwarded, reproduced, divulged or otherwise distributed in any form whether by way of fax, email, oral or otherwise, in whole or in part without the express and prior written consent of Liontrust.