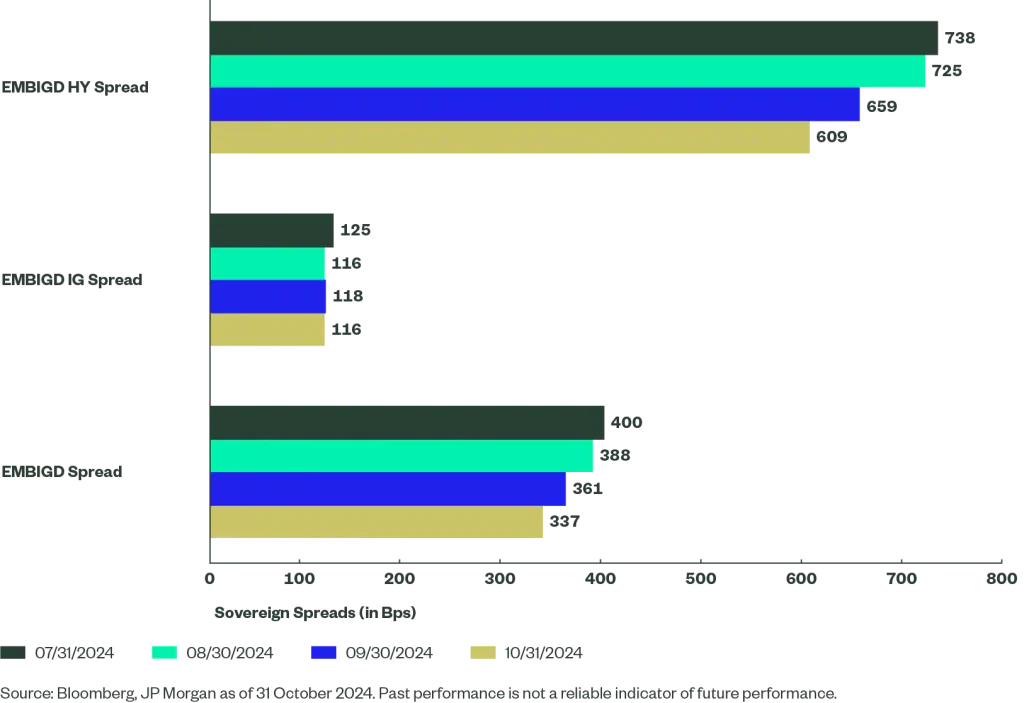

Emerging market hard currency sovereign spreads continued to narrow in October amid risk-off market sentiment. The consequent compression in High Yield-Investment Grade spreads gained momentum on firming expectations for a US soft landing and speculation around the impact from US election outcome possibilities.

Emerging market (EM) debt in October was impacted by a broad reduction in investor risk appetite, fueled by geopolitical risks stemming from the widening conflict in the Middle East and market uncertainty around the US elections. The potential spillover impact of the US election on long-term economic prospects raised some intermittent market concerns for EM macro prospects. Tailwinds from the US Federal Reserve’s (Fed) September rate cut weakened somewhat after the strong US payroll report and a higher-than-expected US CPI print released in October. Overall, total returns were negative for both EM local currency and hard currency bonds in the month. Market repricing of US core rates and expectations of near-term caution around the monetary easing cycle from EM central banks pushed EM local market yields higher, while US dollar strength in October also weighed on returns. EM hard currency debt posted negative returns in October as the treasury component returns were negative across the board.

In terms of monetary easing, markets factored in the likelihood of major EM central bank decisions being driven by domestic inflation and growth factors, rather than US elections and the Fed’s rate cut dynamics. In Latin America (LatAm), the Central Bank of Colombia lowered its benchmark interest rate by 50 basis points (bps) to 10.75% in October. The Central Bank of Chile trimmed its interest rate by 25bps to 5.25%. In EM Asia (ex-China), the Bank of Thailand and the Central Bank of Philippines each cut interest rates by 25bps to 2.25 and 6.0%, respectively. In China, the property sector continued to weigh on performance and the People’s Bank of China (PBoC) maintained its accommodative approach by lowering its policy rates to record lows in October. The one-year loan prime rate and the five-year mortgage reference rate were reduced by 25bps to 3.1% and 3.6%, respectively. China’s long-term benchmark yields remained near multi-decade lows amid expectations of additional rate cuts. According to the data released for Q3, gross domestic product (GDP) rose by 4.6% (on an annual basis), which was below the government’s target of 5%.

Net flows in October for hard currency and local currency bonds amounted to -$1.8bn and $0bn, respectively. (Source: JP Morgan).