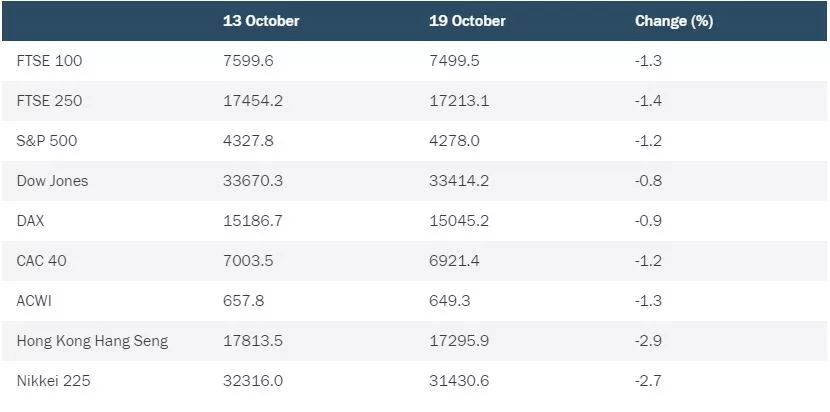

Global stock markets endured another week of volatility and decline as fears about the potential impact of the intensifying conflict in the Middle East grew

Geopolitical concerns have led investors to seek safety in more defensive assets and helped commodity prices remain elevated – a development that has the potential to increase inflationary pressures around the world. There remains considerable uncertainty around central banks’ next moves, with the latest signs of economic resilience in the US and sticky inflation in the UK making future monetary policy changes even more difficult to predict. The emerging consensus among investors appears to be that while policymakers are unlikely to increase interest rates to a significant degree in the months ahead, the prospect of any imminent cuts is receding rapidly.

United States

On Wall Street, the Dow Jones Industrial Average ended trading on Thursday 0.8% down for the week so far, with the S&P 500 dropping 1.2%. Interest rate expectations rose again this week after latest data showed strong performance in retail sales as well as continued resilience in the labour market, with a fresh fall in unemployment claims. In a speech on Thursday, Federal Reserve chair, Jerome Powell, did little to reassure investors that the Fed’s programme of monetary tightening was near its end. There was mixed news in terms of third-quarter company earnings, and downbeat statements from the banking sector offset more positive reports from major technology firms.

UK

In the UK, the FTSE 100 closed on Thursday 1.3% down for the week so far despite the boost provided by high oil prices to London-listed energy businesses. Investors in Britain are also worried about the possibility of further rate hikes after the Bank of England’s chief economist warned at the start of the week that greater effort will be needed to bring inflation under control. To illustrate his point, official figures published on Wednesday showed that the UK Consumer Prices Index in September had remained unchanged at 6.7%, currently the highest rate among the G7 countries. An easing of wage inflation and a fall in job vacancies were welcomed but reports of redundancies at a number of major employers highlighted the ongoing impact of rising costs and high interest rates on the British economy.

Europe

In Frankfurt, the DAX index ended Thursday’s session down 0.9% for the week, while France’s CAC 40 lost 1.2% as America’s interest rate jitters spread to Europe. There was some positive news with the eurozone countries posting a trade surplus given a year-on-year drop in energy prices and reports of improving investor sentiment in Germany. However, earnings statements from major consumer goods companies indicated that shoppers are increasingly struggling to tolerate rising prices.

Asia

In Asia, the Hang Seng index in Hong Kong dipped 2.9% as geopolitical concerns dominated. Shares in China were also hit by the latest salvo in the technology trade war with the US, with the American government imposing new restrictions on the sale and purchase of microchips used in artificial intelligence applications. Positive economic data showing better-than-expected growth in the third quarter of the year was overshadowed by concerns about the property sector and the prospect of a debt default by another major developer. Japan’s Nikkei 225 index of leading shares, meanwhile, lost 2.7%, largely as a result of nervousness around US monetary policy. It was reported that the country’s prime minister was planning to ease tax policies to help households cope with the rising cost of living.