The US treasury yield curve inverted for the first time in almost three years, a traditional harbinger of a recessiona

- The yield curve has inverted more times than there have been recessions in recent decades

- Central bank responses and how long the reversion lasts may provide a clearer picture in terms of recessionary risk

Fears of a looming recession escalated this week as the US treasury yield curve inverted for the first time in almost three years, suggesting investors are worried that the Federal Reserve’s efforts to control inflation will bring about a sharp slowdown in US economic growth.

Yields on two-year US treasury notes rose above those of the 10-year note for the first time since August 2019 on 29 March1. Inversions typically signal underlying weakness in the economy’s long-term growth prospects and have preceded every US recession since the 1970s.

“The threat of recession hangs over markets, particularly in Europe. This week’s brief inversion in the US bond market, combined with elevated volatility on treasury options, is a warning that the risk of US recession should not be ignored. US bond markets are showing signs of stress,” says Lewis Grant, Senior Portfolio Manager – Global Equities, Federated Hermes2.

However, in light of market drivers, such as strong inflationary pressures and high uncertainty surrounding the conflict in Ukraine, the reversion should be viewed as an interesting indicator, not a necessarily clear triggering point for a recession, says Fraser Lundie, Head of Fixed Income – Public Markets, Federated Hermes.

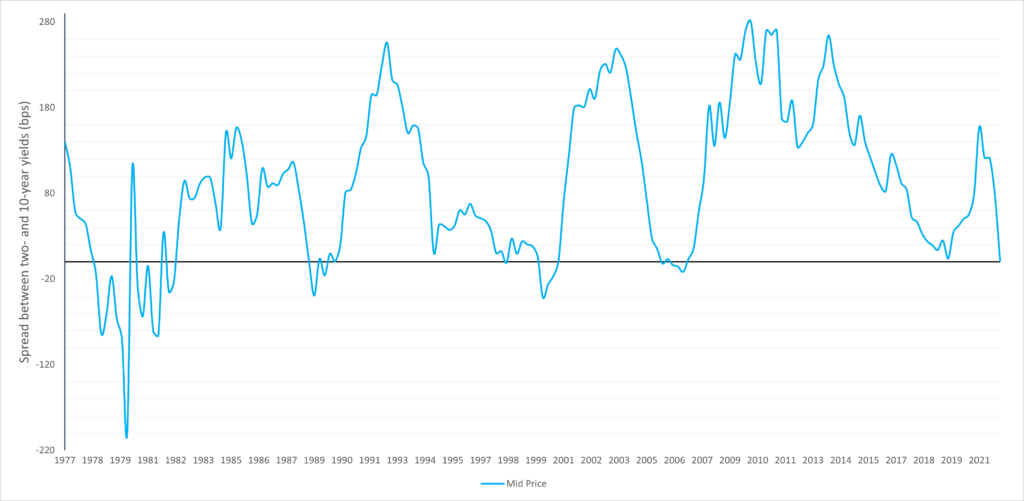

“While the reversion of the two year/10 year part of the US yield curve has raised recession worries, we must remember that historically the yield curve has inverted more times than there have actually been recessions,” Lundie says (See Figure 1).

“How central banks react and how long the reversion lasts will provide us with a clearer picture with regards to medium to longer term recessionary risk.”

Figure 1: The yield curve has inverted more times over last four decades than there have been recessions

Oil price drop

In other news, oil prices dropped on Thursday as the White House announced the largest-ever release of crude oil reserves from country’s emergency stockpile in a bid to ease shortage fears3. The commodity was trading down almost 5% at 16:30 GMT on Thursday at $108 a barrel4.

“The Biden administration is looking to combat some of the effects of inflation through

a massive release of oil from the strategic reserves,” says Grant. “But it remains unclear how much and for how long this will help consumers. The bigger and harder question of how to phase out Russian energy supplies remains, particularly gas supplies to Europe.”

European Equities fell on Thursday, with Germany’s DAX Index closing down 1.31% and France’s CAC 40 Index down 1.21% as Russia warned “unfriendly” foreign countries they must start paying for gas in roubles or it will cut supplies5.

Bonds, however, rallied on the hope the fall in oil prices may help ease inflation. The yield on the 10-year US treasury note had fallen to 2.31% at 16.00 GMT, while Germany’s 10-year Bund yield had fallen to 0.52%6.

To learn more about responsible investing in an inflationary environment read our report: ESG and inflation: An inconvenient truth?

Risk profile

- The views and opinions contained herein are those of the author and may not necessarily represent views expressed or reflected in other communications. This does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

- 1Bloomberg as at 31 March 2022

- 2All references to Federated Hermes relate to the international business of Federated Hermes

- 3US to make biggest ever release from Strategic Petroleum Reserve | Financial Times (ft.com)

- 4Bloomberg as at 31 March 2022

- 5Ibid.

- 6Ibid.