As investors grapple with the ongoing fallout from the Ukraine crisis and Covid-19, the risks posed by stagflation are growing.

- Surging commodity prices and supply chain risks remain pressing concerns, while the French election result fails to spark relief rally.

- Earning season in line with expectations but companies err on the side of caution in their forecasts.

Volatility remains the dominant theme in markets as the war in Ukraine, China’s zero-Covid policy and central bank monetary tightening all continue to affect investor sentiment across the board.

Geir Lode, Federated Hermes1 head of global equities, notes that while earnings season has so far been in line with expectations, the average earnings beat was lower than the average revenue beat. This indicates a margin squeeze from higher material and labour costs, he says.

Coupled with residual pandemic effects, such as the continuing lockdowns in China, supply chain backlogs and further volatility in energy costs as a result of the war in Ukraine, the overall picture is a gloomy one, he adds.

“With the S&P 500 down over 10% and the 10-year interest rate up over 1% since the start of the year, the market is already discounting a high probability of a recession,” he says. “The Fed is getting ready to fight inflation by increasing interest rates faster than anticipated. In this context, investors could do well to focus on stocks less exposed to labour costs and with higher control over their supply chain.”

In France, the election victory of President Emmanuel Macron over right-wing challenger Marine Le Pen failed to spark the relief rally some had expected, says Chi Chan, portfolio manager, European Equities. Against a backdrop of rising uncertainty, public companies are now introducing caution to their outlooks, he says, or even withdrawing them altogether. “With this in mind, we continue to favour well-managed, long-term structural winners with pricing power,” he adds.

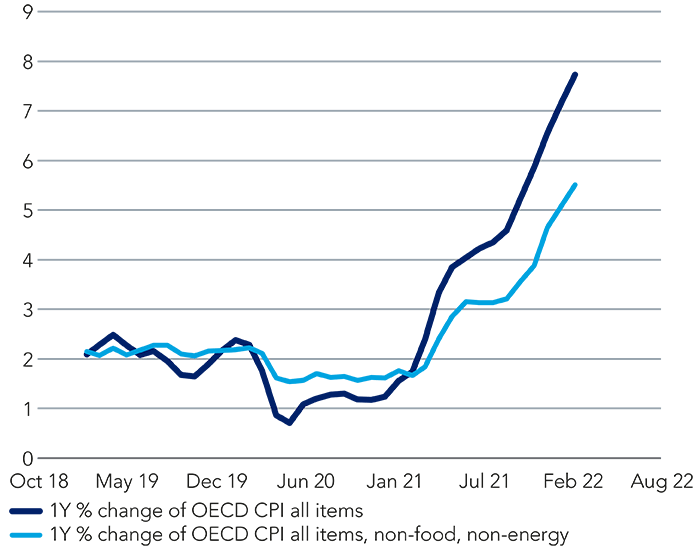

Shapes of things: Three years of OECD inflation data (%)

Source: Bloomberg, 11 April.

Slowing growth and inflation

For Silvia Dall’Angelo, senior economist at Federated Hermes, a toxic mix of slowing growth and short-term inflationary trends is contributing to a rising risk of stagflation.

The US economy unexpectedly contracted in the first quarter, shrinking 1.4% on an annualised basis, down significantly from the 6.9% rise recorded in the fourth quarter of 20212. At the same time, inflation exceeded 8% in March3.

“The Russian invasion of Ukraine and its impact on commodity prices has imparted a stagflationary shock in the midst of an unusual recovery from an unusual recession,” says Dall’Angelo. “The global economy hadn’t fully recovered from the Covid hit before inflation began to surge above the central banks’ targets in most economies. Given the lack of clarity on underlying trends even ahead of the shock from the war in Ukraine, it’s hard to fathom from here whether stagflation will follow.”

As an illustration of global stagflation risk, the MSCI All Country World Index, which comprises stocks of almost 3,000 companies from 23 developed countries and 25 emerging markets, was down 13.3% year to date at 16:30 GMT on 28 April, while the price of West Texas crude was up 38% year to date4. The price of gold, a traditional investor safe haven during periods of distress, was trading at $1,888 a troy ounce (up 3% year to date) after breaching $2,000 in early March.

Looking forward, Dall’Angelo expects inflation to remain sticky at elevated levels while demand will likely slow down significantly over the second half.

“Our base case is that stabilisation in energy prices, base effects, some easing of global supply constraints and, crucially, the likely slowdown in demand will all contribute to drive inflation down over 2023, although it will remain above target given the elevated starting point,” she says.

With this in mind, the central bank policy response will be crucial, and central banks can be expected to have a hard time calibrating the right amount of tightening to achieve a soft landing. “This means there’s a risk of moving from a stagflation scenario to a recession scenario. That challenge is particularly pronounced for a Federal Reserve that is behind-the-curve by its own admission,” she concludes.

For further insight on the inflationary backdrop and its interplay with long-term megatrends, read the latest report from our Impact Opportunities team.

Risk profile

- The views and opinions contained herein are those of the author and may not necessarily represent views expressed or reflected in other communications. This does not constitute a solicitation or offer to any person to buy or sell any related securities or financial instruments.

2 US economy contracts for first time since mid-2020 | Financial Times (ft.com)

3 US inflation hits 8.5% after surge in energy and food prices | Financial Times

4 Bloomberg, as at 28 April