The equity market rally continued over last week, as stronger US data releases saw markets move further into pricing a ‘soft landing’ scenario.

We also witnessed a new record for the Dow Jones index which experienced its longest winning streak since 1987, advancing for 13 consecutive sessions, as stocks globally approach new all-time highs.

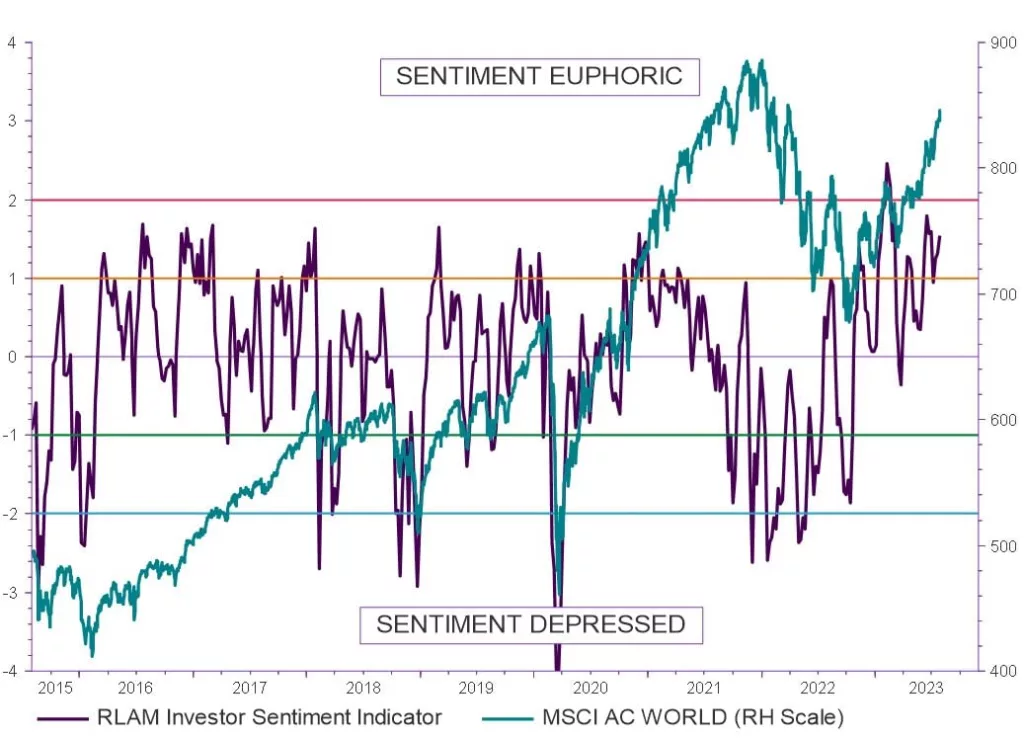

Against this backdrop of rising markets, our measure of investor sentiment has also returned to overly euphoric territory (chart 1), with volatility trending lower and retail investors displaying particularly bullish tendencies.

While the extent of this rally and the bullish levels of investor sentiment do send a note of caution, we believe markets can continue to move higher and we remain positive on equities for the time being. The macro backdrop is positive, with global growth remaining resilient and inflation moving decisively lower from peak levels.

We still expect more defensive positioning to be necessary at some point later this year as the effects of tighter policy transmit to the real economy and volatility spikes higher.

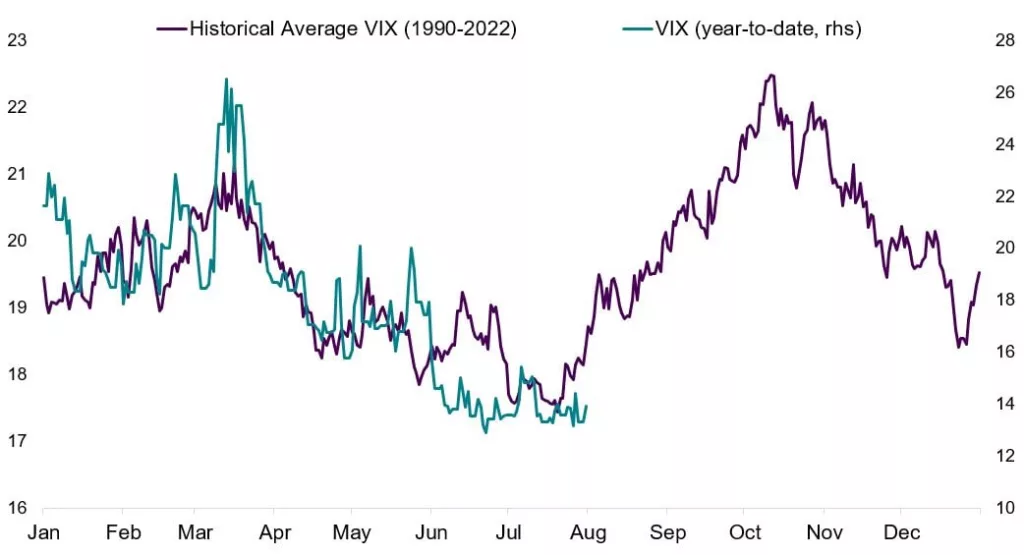

Volatility has trended lower over recent months, another factor which has contributed to our overbought investor sentiment score. However, this pattern of lower early summer volatility is nothing unusual, with VIX tending on average to trough in July (chart 2). It’s therefore common for volatility to move higher from here, a pattern we would not be surprised to see repeated this year should macro conditions deteriorate.

Chart 1: Investor sentiment is in overbought territory

Chart 2: Volatility has been drifting lower into summer

Market summary

Global stocks rose to their highest levels since April 2022, as improving growth conditions, rising earnings expectations, and cooling price pressures raised hopes for a soft landing in the US. Gains were further supported by a pledge by Chinese authorities to stimulate the economy, which saw emerging market and Asia Pacific stocks outperform other equity regions. Elsewhere, US yields rose sharply following a strong Q2 GDP print, while JGB yields rose as the Bank of Japan (BoJ) adjusted their yield curve control policy to allow greater flexibility, which also caused volatility in the Japanese yen.

Economics summary

Interest rate hikes of 0.25% from the US Federal Reserve (Fed) and European Central Bank (ECB) were accompanied by a heavy focus on data dependency (which may have implications for market volatility around future data releases). The door was at least opened to this marking peak rates. The BoJ tweaked YCC, setting a new 1% ceiling. The Bank of England are expected to follow the Fed and the ECB this week by hiking 0.25%.

This is a financial promotion and is not investment advice. Past performance is not a guide to future performance. The value of investments and any income from them may go down as well as up and is not guaranteed. Investors may not get back the amount invested. Portfolio characteristics and holdings are subject to change without notice. The views expressed are those of the author at the date of publication unless otherwise indicated, which are subject to change, and is not investment advice.