The recent Iran-related escalation in the Middle East has moved beyond a short-term oil shock. With strained negotiations and only a tenuous ceasefire, the risk of prolonged disruption—particularly around the Strait of Hormuz—has increased. As we have said before, duration of the conflict—not just its magnitude—matters.

The conflict has now persisted long enough to have long-term, global economic implications. Its potential impact extends well beyond the daily movement in oil prices. While effects on the energy sector are clear, broader spillovers—both direct and indirect—are likely to touch numerous areas of the market, from big tech to consumer spending and near-term monetary policy.

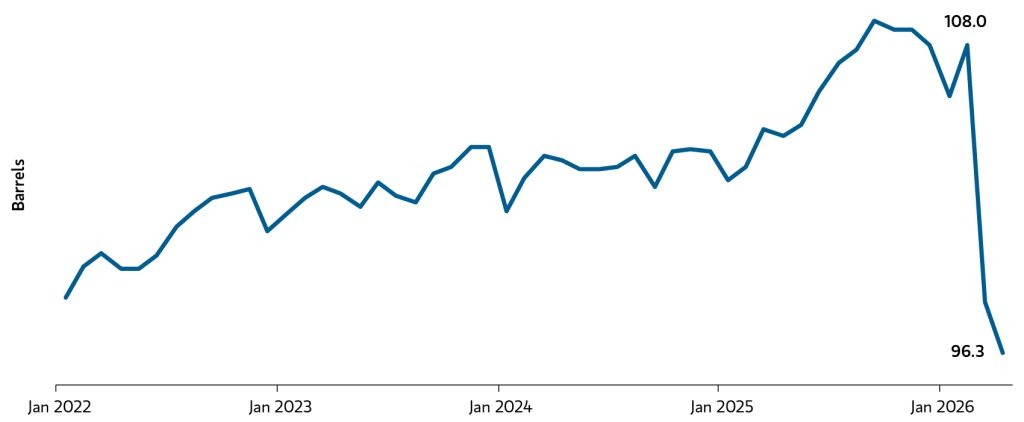

First, we rewind to cover the current supply of oil hitting the market…

Global Oil Production: 12 Million Barrels Short

Source: U.S. Energy Information Administration (EIA); April 7, 2026.

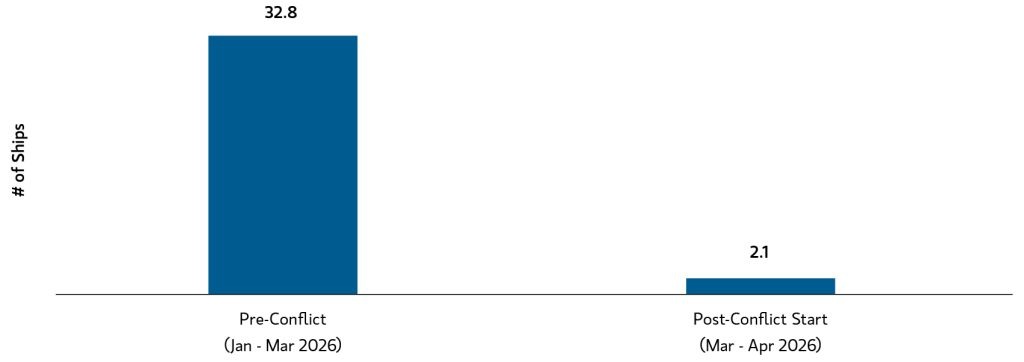

Maritime Disruption: Daily Number of Ships Traversing the Strait of Hormuz

Source: UBS, April 15, 2026.

While a 12 million barrel-per-day difference may not appear large in a global context, it represents the largest supply shock since the 1970s OPEC oil embargo. Further, its persistence amplifies the risk of broader economic impacts. Moreover, the timing of this disruption further compounds the issue, with the gasoline-heavy summer driving season (May through August) quickly approaching. Again, duration matters.

Second and Third Order Effects…In the Not-So-Distant Future

While the clear focus has been on oil, we are closely monitoring the potentially broader, indirect economic consequences, particularly risks to key value sectors where growth strategies are reliant on global supply chains. Across sectors, we see several potential impacts:

- Consumer: Headwinds are likely to increase for U.S. housing and other interest-rate-sensitive industries. In contrast, tailwinds may emerge for off-price retail and other value- conscious segments.

- Tech: Watch Helium! Nearly one-third of global supply comes from Qatar, and helium is a key input in semiconductor manufacturing. Delays in helium transport could disrupt longer-term, hyper-scaler data center builds and the electric utilities powering them.

- Manufacturing: Watch Diesel! Nearly 80% of Middle East exports go to Asia. Factories in Vietnam, Thailand and Japan rely on diesel for both transport and manufacturing. A prolonged conflict will disrupt supply chains globally.

- Energy: Approximately 20% of global liquid natural gas (LNG) flows through the Strait of Hormuz. A prolonged conflict could increase demand for coal. Also, cheap natural gas in the U.S. is great for American manufacturing; low-cost inputs give aluminum and steel companies a competitive advantage.

Bottom line: Looking ahead, the Iran-Middle East conflict risks becoming the second global supply-chain disruption in five years. We believe this may push company management teams to focus on local supply chains to reduce risk. This could have long-term implications for capital-goods producers, steel producers and fabricators, industrial gas producers, and U.S.-based semiconductor companies. In these volatile times, with meaningful short- and long-term implications, we believe having a dedicated, experienced investment team actively analyzing companies is essential to building a portfolio that can navigate today’s markets and remain forward looking.