Broadly constructive on the region’s bonds

Summary

- US Treasury (UST) yields rose in December, with the benchmark 2-year and 10-year UST yields climibing to 4.43% and 3.87%, respectively, about 12 basis points (bps) and 27 bps higher compared to end-November.

- Inflationary pressures within the region mostly moderated in November. Central banks in India, Indonesia and the Philippines hiked their policy rates in December.

- In December, China further relaxed its COVID-19 restrictions, and travellers to the country will no longer be subject to quarantines and PCR test requirements. China’s top leadership vowed to “forcefully revive market confidence” and put growth on top of the priority list. It also called for new measures to assist the ailing property market.

- We prefer Singapore and South Korea government bonds as well as Indonesia bonds. We favour the Singapore dollar and the Thai baht. Asian credits gained 1.66% in December, as spreads tightened about 37.4 bps and UST yields dropped. Asian high-yield (HY) rose 6.31%, outperforming Asian high-grade (HG) credits, which gained 0.84%.

- We believe there is room for Asian credit spreads to tighten in the early part of 2023 given global investors’ light positioning, as well as the potential for fresh capital and risk allocation to the asset class at the start of the year.

Asian rates and FX

Market review

UST yields rise in December

The US Federal Reserve (Fed) hiked their policy rate by 50 bps during the Federal Open Monetary Committee (FOMC) meeting in December 2022. The Fed’s median forecasts for the peak Fed fund rate rose to 5%–5.25% from 4.5%–4.75%. Fed Chair Jerome Powell remained hawkish, noting during the post-FOMC press conference that “substantially more evidence” is needed to convince him that inflation is moving towards the Fed’s 2% target. Meanwhile, on 20 December, the Bank of Japan (BOJ) unexpectedly expanded its target range for the 10-year Japanese government bond (JGB) yield to +/-50 bps on either side of 0% from +/- 25 bps. Both JGB and UST yields moved higher following the BOJ meeting. News that China would re-open its borders further drove UST yields higher. UST 2-year and 10-year yields ended December at 4.43% and 3.87 %, respectively, about 12 bps and 27 bps higher compared to end-November.

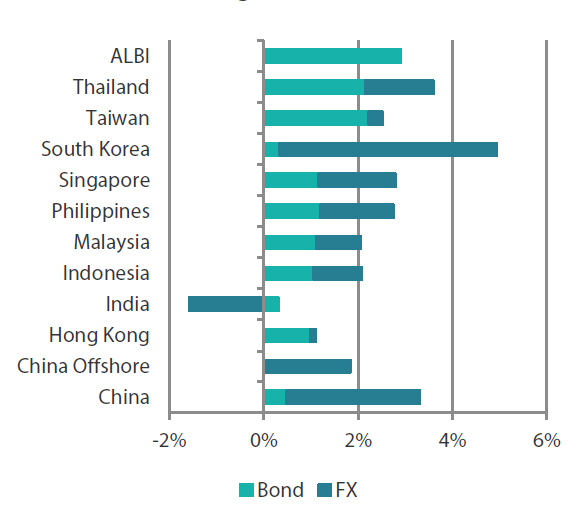

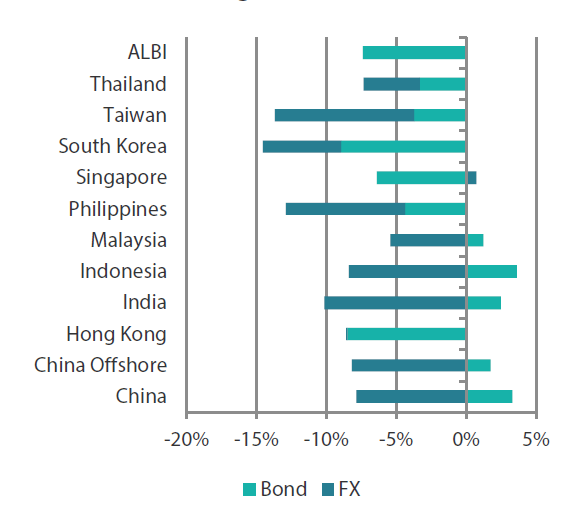

Chart 1: Markit iBoxx Asian Local Bond Index (ALBI)

For the month ending 31 December 2022

For one year ending 31 December 2022

Note: Bond returns refer to ALBI indices quoted in local currencies while FX refers to local currency movement against USD. ALBI regional index is in USD unhedged terms. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

Asia’s headline consumer price index (CPI) prints mostly moderate in November

November headline CPI prints in the region eased for the most part as food prices moderated. On the other hand, core inflation in the region remained sticky. While Singapore’s core CPI remained flat at 5.1%, Malaysia’s core CPI was marginally higher at 4.2% (versus 4.1% the previous month). Indonesia’s headline CPI eased slightly to 5.42% in November from 5.71% in October. Thailand’s headline CPI for November moderated to 5.55% from 5.98% in October as food prices eased. However, core inflation in Thailand rose marginally to 3.22%. In contrast, the headline CPI for the Philippines rose to 8.0%, beating expectations for the third consecutive month as food price pressure continued to mount. Stripping out the prices of volatile commodities, core inflation in the Philippines also surged, to 6.5% in November from an upwardly revised 5.9% in the prior month.

Monetary authorities hike policy rates with smaller steps

Central banks in India, Indonesia and the Philippines hiked their policy rates in December. The Reserve Bank of India delivered a smaller rate hike of 35 bps compared to previous meeting, raising the policy rate to 6.25%. Importantly, the Monetary Policy Committee cut its growth forecast for FY2023 to 6.8%, while keeping the inflation forecast unchanged at 6.7%. Bank Indonesia (BI) lifted its key rate in December by 25 bps to 5.5%. BI commented that the smaller rate hike was a follow-up step to ensure lower expected inflation and that it was a front-loaded, pre-emptive measure to cap core inflation. The Bangko Sentral ng Pilipinas (BSP) raised its policy rate to 5.5% from 5.0% as broadly expected, stating that this hike would support the Philippine peso amid tightening global financial conditions. The BSP kept its 2022 inflation forecast unchanged at 5.8% but raised its 2023 inflation forecast to 4.5% from 4.3% while lowering its inflation forecast for 2024 to 2.8% from 3.1%.

China eases COVID-19 restrictions

On 7 December, China’s authorities announced a further easing of COVID measures, and highlighted coordination between pandemic control measures and economic development. Ten more measures were announced by the NHC (National Health Commission) on the same day. On 26 December, the NHC greatly eased COVID curbs again by downgrading the management of the virus from “Class A” to “Class B” and updated the Chinese term for COVID from “coronavirus pneumonia” to “coronavirus infection”, removing quarantine and PCR test requirements for inbound travellers. The Central Economic Work Conference took place during 15–16 December, during which the top leadership vowed to “forcefully revive market confidence”. The conference also put growth on the top of its priority list while a restrained stance was shown regarding stimulus out of concerns towards factors such as local government finance, inflation risks and financial stability. On the property sector, the conference called for new measures to turn around home sales and developer financing, help leading developers resolve risks and ensure a smooth transition towards a “new real estate development model”. “Housing is for living not for speculation” remains the overarching principle.

Market outlook

Remain constructive on overall duration; Prefer Singapore, Korea and Indonesia bonds

For 2023 we expect global inflation to ease and global growth to weaken; we also think that the Fed is likely to pause hiking rates by the first quarter of 2023. Against this backdrop, we are broadly constructive on regional bonds as most Asian central banks could be nearing the end of their rate hike cycles. Within Asia, we favour both Singapore and South Korean government bonds, given their relatively higher sensitivities to stabilising UST yields. In addition, we believe that South Korea’s central bank may end their rate hike cycle soon. Meanwhile, demand for Indonesia bonds could increase when upward pressure on global bond yields eases and market focus turns to their attractive real yields relative to those of their regional peers.

Singapore dollar and Thai baht preferred

On currencies, we take a neutral to underweight view on the US dollar as we see demand for the currency waning if the Fed pivots. Also, the earlier-than-expected re-opening of China’s borders and easing of COVID measures are expected to support regional growth and in turn lift foreign exchange sentiments. We expect a majority of Asian currencies to outperform the dollar and see the Thai baht and the Singapore dollar further outperform their regional peers. In Singapore, sticky core inflation may prompt the Monetary Authority of Singapore (MAS) to keep the Singapore dollar nominal effective exchange rate (NEER) on an appreciating stance. Meanwhile, demand for the Thai baht could increase meaningfully along with a return by Chinese tourists to Thailand.

Asian credits

Market review

Asian credit spreads end tighter with optimism over China’s re-opening

Asian credits gained 1.66% in December, as spreads tightened about 37.4 bps and UST yields rose. The marked improvement in risk sentiment led Asian HY to outperform Asian HG credits. Asian HG credit gained 0.84%, with spreads tightening about 21.8 bps, and Asian HY credit returned 6.31%, with spreads narrowing 159.3 bps.

Following the sharp rally in risk assets in November, investors remained excited in December towards China’s re-opening and positive headlines regarding the country’s property sector. Following the initial measures announced in November, China followed up with a significant further relaxation of its COVID containment policies, which included a removal of broad testing requirements and an introduction of home quarantine. In late December, China announced that it would re-open its borders in early January 2023 with inbound travellers no longer subject to mandatory quarantine requirements upon arrival. These policy tweaks and statements highlight the tentative path China is taking towards loosening of its COVID restrictions, seen as an important factor driving economic growth. Both Hong Kong and Macau also announced meaningful COVID control relaxations. The faster-than-expected relaxation of COVID-related policies by China boosted market sentiment, leading to tightening of credit spreads, particularly in China, Macau and Hong Kong. That said, such moves were milder compared to November as liquidity declined further into the year-end. In the China property sector, an announcement by the China Securities Regulatory Commission that onshore equity financing channels for developers would be resumed triggered another rally. While the theme in December was largely focused on the re-opening of Greater China, other parts of Asia also joined the rally with inflows to emerging market bond funds supporting further spread tightening for Indian credits as well as Philippine and Indonesian sovereigns and quasi-sovereigns. Taiwanese and Thai credits also outperformed on strong technicals and are some of the biggest potential beneficiaries of China’s re-opening.

UST yields mostly fell during the first half of December. Yields initially treaded lower as markets focused on weak inflation and activity data over hawkish central bank developments. Both the November US headline and core CPI prints eased more than expected. Nevertheless, the Fed hiked rates by 50 bps as expected in December, but the accompanying statement was more hawkish than anticipated, with the Fed noting that “ongoing increases” in the funds rate are likely appropriate. In the second half of the month, UST yields rebounded somewhat following hawkish policy decisions by the European Central Bank and the BOJ.

Primary market activity remains quiet in December

New issuances for Asian credits slowed down in December ahead of the year-end. Four new issues raised a total of USD 900 million in the market. The HG space saw three new issues amounting to about USD 853 million, including a USD 250 million issue from Industrial and Commercial Bank of China and a USD 350 million Deyang Development Holdings Group Co issue. Meanwhile, the HY space remained quiet with one issuer raising a small size of USD 47 million in December.

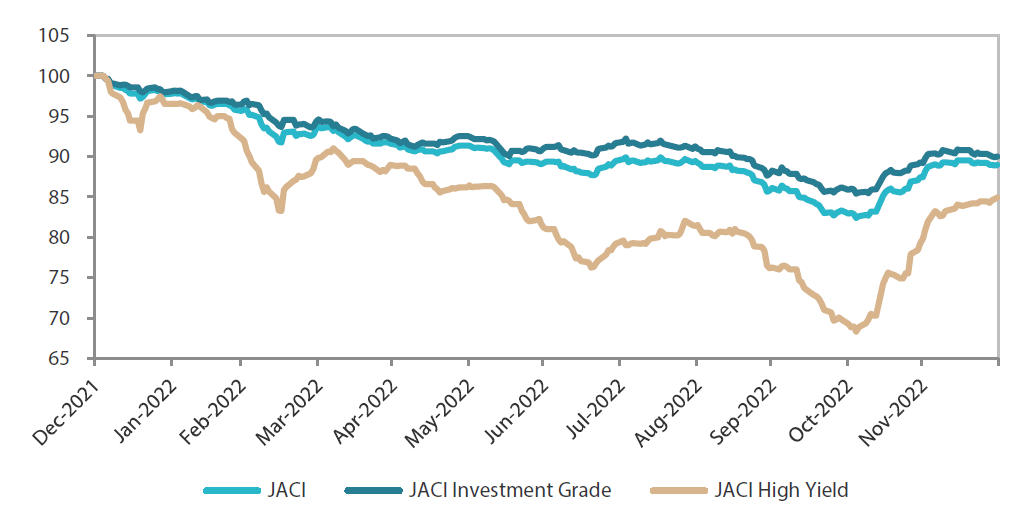

Chart 2: JP Morgan Asia Credit Index (JACI)

Index rebased to 100 at 31 December 2021

Source: Bloomberg, 31 December 2022

Market outlook

Technicals and resilient fundamentals to support Asia credit spreads at start of 2023

We believe there is room for Asian credit spreads to tighten in the early part of 2023 given global investors’ light positioning, as well as the potential for fresh capital and risk allocation to the asset class at the start of the year. This comes against the backdrop of some positive catalysts, including a potential slowdown in Fed rate hikes and China’s policy shifts in certain key areas including COVID management, the property sector and internet platforms. Once the initial wave of inflows and deployment are over, the evolution of Asian credit spreads could become more tentative and there might be more volatility from second quarter of 2023 onwards depending on the developments of growth and inflation, and consequently monetary policy, in the developed markets.

In our base case, disinflation is likely to become a stronger narrative in the US as we move through 2023. The US economy may experience a mild recession sometime in 2023, although the timing is uncertain. The balance of risk between a soft (very weak growth but no recession) and hard landing (more severe recession) scenarios seems even at this point. In our base case, UST yields should gradually move lower through 2023.

China’s policy shifts are expected to support growth recovery in 2023, although risks around implementation and policy predictability remain. To be sure, China’s exit path from its zero-COVID policy is likely to be stop-start in nature given the population’s low natural immunity and the country’s less than well-equipped healthcare system. China’s determination to follow through on the relaxation of COVID measures and its expansion of support to the property sector beyond just financing to demand-oriented measures to revive new home sales growth will be critical for sustaining positive investor sentiment towards China credits, both HG and HY. At the same, while geopolitical tensions seem to have stabilised, latent risks remain, particularly around technology and the Taiwan issue.

Macro and corporate credit fundamentals across Asia ex-China are expected to stay robust, albeit weaker given the softness in exports, tighter global financial conditions and higher domestic interest rates. Indian and ASEAN economies, supported by a rebound in tourism and domestic re-openings, are expected to fare better than exportdependent North Asia. Given the backdrop of declining UST yields and still resilient fundamentals, we expect Asian credit spreads to stay within a range after the initial tightening at the start of the year.

There are nevertheless downside risks to the base case scenario. In our view a key downside risk is inflation across major economies being more persistent than expected. This could lead to a more protracted hiking cycle, higher terminal policy rates, a more severe economic downturn in the developed economies, a backtracking by China on its COVID and property sector policies and local funding and credit market stress—such as the one experienced by South Korea early in 4Q2022. The materialisation of one or more of these downside risks could lead to the widening of Asian credit spreads from current levels.

Important disclaimer information

Please note that much of the content which appears on this page is intended for the use of professional investors only.