Updating our views on market signals and some key investment debates

Our focus this quarter was on the opportunities we see in in the global transition to lower carbon and the consequences of bank disintermediation. See the full overview below.

What is QIF?

The Quarterly Investment Forum (QIF) is an ongoing cross-investment team discussion and debate about the most relevant active risks in major markets and across asset classes and funds.

Each QIF is a mix of ‘top down’ and ‘bottom up’ perspectives, beginning with a ‘top down’ discussion of the major macroeconomic themes identified by the Asset Allocation Team. Each quarter, a rotating roster of portfolio managers present a ‘bottom up’ view of major active risks in their portfolios.

We have a unique depth and breadth of investment expertise across traditional and alternative asset classes in all regions globally. The QIF leverages that expertise through regular, structured communication between investment teams. The ultimate goal is to improve client outcomes.

4Q 2021 Quarterly Investment Forum highlights

Macro outlook

Evan Brown, Head of Multi-Asset Strategy Investment Solutions

Our view is that this cycle is different than the recovery from the Global Financial Crisis, and it’s better. Growth will likely be more robust in this expansion compared to the previous one, because of more supportive fiscal policy, stronger growth in labor income, and higher capital expenditures.

We believe that the market is not priced for this positive environment, so the risk-reward opportunity is better in assets, regions, and sectors that stand to benefit from these growth tailwinds. Bond yields are too low for this set of economic fundamentals, and cyclicals should reprice higher relative to defensives, in our view. While faster Federal Reserve tightening cycles can introduce short-term volatility in markets, we expect equities to move higher buoyed by good earnings growth.

The lingering threat of COVID outbreaks, as well as mutations that could significantly undermine the effectiveness of vaccines, remains the key risk to the outlook. The potential for a sharp slowdown in Chinese activity, though not our base case, would also jeopardize this optimistic growth backdrop.

Persistently elevated inflation that threatens to raise longer-term inflation expectations would also likely generate a more aggressive withdrawal of monetary stimulus that could pose a headwind for activity as well as risk asset performance.

Opportunities and risks on the road to Net Zero

Tom Kasa, Head of Sustainability, Environmental Focus Fund

We believe that there are generational market opportunities associated with the trillions of dollars in investments needed as we move towards the goal of a decarbonized energy system, both on the long and short sides. In our view, completing this transformation is a long-term imperative but will be subject to societal constraints (tolerance for higher prices / lower energy consumption), as well as governments who want to avoid any economic or political destabilization along the way. Failing to satisfy different stakeholders may result in a step backwards in this transition (for instance, boosting coal consumption due to insufficient alternatives and high energy demand).

There are several areas of improvement available to hasten this process. Better data on product-level emissions may make a tremendous difference in consumer behavior, and allow them to better incorporate sustainability considerations in their purchases. It would also enable investors to better identify long and short opportunities and policymakers to better target regulations at products that are hurting the environment. Enhancing existing carbon taxes which currently either cover an insufficient part of the economy, or are priced well below any reasonable estimates of the social cost of carbon, may also help. Integrating renewable energy into the existing electricity grid (currently not primarily a technology issue in the US, but rather facing roadblocks from a regulatory approval perspective) may also be beneficial.

Ellis Eckland, Senior Investment Analyst

Under the International Energy Agency’s scenario for moving to Net Zero, total energy production needs to fall 7% over the next 10 years and the net energy consumed per person would fall even more as populations increase. Since energy consumption per capital is unlikely to go down in India, Africa, or Southeast Asia, this implies that high energy usage areas like the US, European Union, and Japan need to see per capita consumption decline by 30-40% over the next 10 years. This would be unlike anything experienced in the last 200 years, and could lead to discontent and even unrest.

Modern food production relies heavily on energy inputs, and therefore food is likely to become more expensive. Energy-intensive components that are needed to build out capacity for renewables are likely to become more expensive as well, so estimates of the capital expenditures needed for the energy transition are also likely too low.

One positive is that the “E” in ESG should really pay off. More energy efficient firms are likely to outperform within their respective industries. Current fossil fuel companies will likely retain value during the transition phase, because the world needs fossil fuels to build out renewables, and beyond, because even past 2050 some of these energy sources will still be in use, even if only at 20 to 25% of their current size. But over time, they are likely to transition towards hydrogen. These companies have the expertise to work with it, are already using it in some cases, and have the pipelines and infrastructure required to transport it.

Francis Condon, Head of Thematic Engagement & Collaboration

In metals, we believe that the road to Net Zero is most beneficial for copper. Electrification is the name of the game when it comes to limiting the rise in temperatures to below 1.5 degrees Celsius. Copper is a huge contributor to moving electrons around, and the cornerstone of technologies associated with electricity generation, transmission, and end appliances. In Net Zero scenarios such as outlined by the International Energy Agency1, copper use doubles between now and 2050, and supply is not ready to meet the anticipated increase in demand over the course of this decade. Copper supply is also vulnerable to climate stress, as production competes with other users for water, and mines are subject to extreme heat and flooding.

For other metals, this transformation will likely be less positive. Steel will be needed for infrastructure, but has less scope for demand growth and requires a substantial amount of capital to reduce the emissions generated in its production process. Aluminum is likely to see higher utilization, but through a significant expansion in how we recycle.

In some smaller materials markets involved in battery production (lithium, graphite, nickel, cobalt) the potential demand growth is huge. However, many of these materials are highly sensitive to technological developments on how batteries are constructed, which can undermine demand.

Secular disintermediation of banks

Baxter Wasson, Co-Head of Private Credit, O’Connor

Typically, opportunities in bank disintermediation are tied to shifting regulatory frameworks that make it harder for banks to engage in certain types of lending activity. Regulation, not organic innovation, is the key driver. Unlike technological disruption, this disintermediation almost always involves former bankers, and at times entire divisions within banks, leading this disintermediation process.

One of the largest recent waves of bank disintermediation is the rise of private credit market, where funds make loans between USD 50 million and USD 1 billion to companies and engage in a wide range of consumer lending working hand-in-hand with fintech companies. This growth has been a function of post-crisis regulation that make it harder for banks to engage in this environment, and has been a huge boon for asset managers.

We believe that UBS Asset Management is well-positioned to benefit from private lending in part because of its strong affiliation with a bank with strong investment banking capabilities. A substantial share of transactions is referred to us from other parts of UBS.

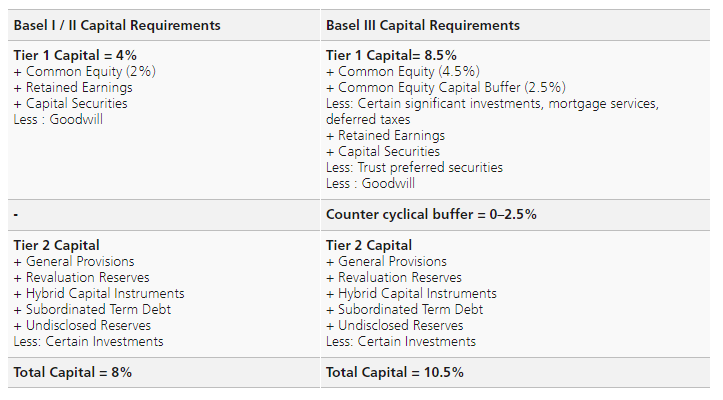

Exhibit 1: Regulatory and cost constraints create opportunity

Basel III has forced banks to improve their capital ratios reducing capacity for Working Capital Finance. More capital means increased pricing / scarcer availability.

Regulatory and cost constraints create opportunity

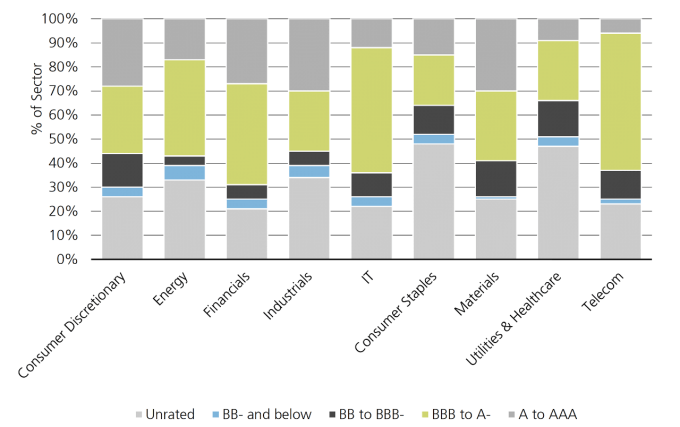

Exhibit 2: Global public company cost of goods sold approximately USD 25trn annually provides a large total available market

Chart shows the percentage of debt rated A to AAA, BBB to A-, BB to BBB-, BB- and below, and unrated among the nine of the largest business sectors.

Casey Talbot, Head of Fixed Income, O’Connor

Supply chain finance involves funding payables and receivables from large corporations, and underwriting accordingly to that risk. The opportunity is created by a rising cost of capital for banks coupled with a byzantine approval system that prevents them from responding quickly.

During the COVID crisis, the value of more diversified funding sources was apparent. All banks that offer credit lines typically behave in a roughly correlated fashion. As companies draw on credit, banks reduce funding in other areas – including supply chain finance. Asset managers don’t behave as similarly, allowing some of their funds to fill that void.

Patrick Huber, Head of Product Strategy & Shelf Evolution

Blockchain provides the means to streamline and reduce the litany of counterparties involved in financial transactions. Smart contracts, which not only represent an asset but can also perform tasks like rebalancing, also have the potential to disintermediate parts of the traditional financial system.

Cross-border currency payment in crypto are fast, convenient, and can be performed at a cost reasonably comparable to banks. Asset creation can allow for brokers, exchanges, and clearinghouses to be circumvented, and also with great built-in transparency if participants are properly identified in the first place.